Potrebbero piacerti anche

- East Coast Yacht's Expansion Plans-06!02!2008 v2Documento3 pagineEast Coast Yacht's Expansion Plans-06!02!2008 v2percyNessuna valutazione finora

- Audi, BMW and Skoda's Research and Development CaseDocumento3 pagineAudi, BMW and Skoda's Research and Development CaseJeklin LewaneyNessuna valutazione finora

- Mini Case STOCK VALUATIONDocumento5 pagineMini Case STOCK VALUATIONRizky Khairunnisa0% (1)

- Erro Jaya Rosady - 042024353001Documento6 pagineErro Jaya Rosady - 042024353001Erro Jaya RosadyNessuna valutazione finora

- Cash Flow Statements and Warf Computers Mini CaseDocumento6 pagineCash Flow Statements and Warf Computers Mini CaseAshekin MahadiNessuna valutazione finora

- Conch Republic Electronics Capital Budgeting CaseDocumento5 pagineConch Republic Electronics Capital Budgeting Casegilli1trNessuna valutazione finora

- Warf Computers Case - CHAPTER 27 AnswersDocumento3 pagineWarf Computers Case - CHAPTER 27 AnswersTrent100% (2)

- HALVIS - 1921011017 - Mini Case THE COST OF CAPITAL FOR GOFF.Documento8 pagineHALVIS - 1921011017 - Mini Case THE COST OF CAPITAL FOR GOFF.Sekar WulandariNessuna valutazione finora

- Assig BetaDocumento9 pagineAssig BetaGan Huey Ling100% (1)

- Case Solutions For Case Studies in Finance 7th Edition by BrunerDocumento1 paginaCase Solutions For Case Studies in Finance 7th Edition by BrunerbhaskkarNessuna valutazione finora

- 1 Week-6Documento3 pagine1 Week-6restameria ubNessuna valutazione finora

- Bunyan LumberDocumento8 pagineBunyan LumberDinh JamieNessuna valutazione finora

- Week 3 BUS 650 Assignment Finance Goff ComputerDocumento12 pagineWeek 3 BUS 650 Assignment Finance Goff Computermenafraid100% (4)

- The Cost of Capital For Goff Computer, Inc 1Documento7 pagineThe Cost of Capital For Goff Computer, Inc 1Zahra ZfraNessuna valutazione finora

- Corporate Finance Asia Edition (Solution Manual)Documento3 pagineCorporate Finance Asia Edition (Solution Manual)Kinglam Tse20% (15)

- Solutions Manual: Fundamentals of Corporate Finance (Asia Global Edition)Documento8 pagineSolutions Manual: Fundamentals of Corporate Finance (Asia Global Edition)Silver Bullet100% (1)

- RequiredDocumento3 pagineRequiredKplm StevenNessuna valutazione finora

- Macrs Depreciation: New Smart Phone Calculation AnalysisDocumento4 pagineMacrs Depreciation: New Smart Phone Calculation AnalysisErro Jaya RosadyNessuna valutazione finora

- Ross, Westerfield, Jaffe - Corporate Finance. Vol. II PDFDocumento64 pagineRoss, Westerfield, Jaffe - Corporate Finance. Vol. II PDFRamakrishnan RanganathanNessuna valutazione finora

- Chapter 19 - Dividend & Other PayoutDocumento23 pagineChapter 19 - Dividend & Other PayoutHameed WesabiNessuna valutazione finora

- Case 4 Stock Valuation 1Documento1 paginaCase 4 Stock Valuation 1Camesh Janu0% (1)

- Tan, Ma. Cecilia ADocumento20 pagineTan, Ma. Cecilia ACecilia TanNessuna valutazione finora

- Case #2 - The Mba Decision - QuestionsDocumento1 paginaCase #2 - The Mba Decision - QuestionsGarrett Singer0% (1)

- Bullock Mining CaseDocumento2 pagineBullock Mining Casekennyfrease50% (4)

- Final Exam Financial Management Antonius Cliff Setiawan 29119033Documento20 pagineFinal Exam Financial Management Antonius Cliff Setiawan 29119033Antonius CliffSetiawan100% (4)

- SHY Week 1 Assignment SolutionDocumento2 pagineSHY Week 1 Assignment Solutionhy_saingheng_7602609Nessuna valutazione finora

- Cost of Capital: Answers To Concepts Review and Critical Thinking Questions 1Documento7 pagineCost of Capital: Answers To Concepts Review and Critical Thinking Questions 1Trung NguyenNessuna valutazione finora

- Wacc 4Documento10 pagineWacc 4Rita NyairoNessuna valutazione finora

- Mini Case: Bethesda Mining Company: Disusun OlehDocumento5 pagineMini Case: Bethesda Mining Company: Disusun Olehrica100% (2)

- Mini CaseDocumento9 pagineMini CaseJOBIN VARGHESENessuna valutazione finora

- Tugas Manajemen KeuanganDocumento3 pagineTugas Manajemen KeuanganmunawarchalilNessuna valutazione finora

- Conch CaseDocumento3 pagineConch Casesantosh kumar25% (4)

- NPV & Other Investment Rules - RossDocumento30 pagineNPV & Other Investment Rules - RossPrometheus Smith100% (1)

- 5762 10964 IM FinancialManagementandPolicy12e HorneDhamija 9788131754467Documento152 pagine5762 10964 IM FinancialManagementandPolicy12e HorneDhamija 9788131754467sukriti2812Nessuna valutazione finora

- APT-What Is It? Estimating and Testing APT Apt and Capm ConclusionDocumento19 pagineAPT-What Is It? Estimating and Testing APT Apt and Capm ConclusionMariya FilimonovaNessuna valutazione finora

- Jawaban Kasus John Deere Component Works (A)Documento2 pagineJawaban Kasus John Deere Component Works (A)Hafizah MardiahNessuna valutazione finora

- Solución Mini Caso Cap. 8Documento5 pagineSolución Mini Caso Cap. 8Anonymous 5qHvuEIVz0Nessuna valutazione finora

- Ross FCF 9ce Chapter 10Documento35 pagineRoss FCF 9ce Chapter 10Kevin WroblewskiNessuna valutazione finora

- Mm0057 Financial Management Midterm Exam: No. 1 - Track Software, IncDocumento15 pagineMm0057 Financial Management Midterm Exam: No. 1 - Track Software, Incnavier funtabulousNessuna valutazione finora

- AFIN1Documento6 pagineAFIN1Abs PangaderNessuna valutazione finora

- Case Ragan - Stock ValuationDocumento5 pagineCase Ragan - Stock ValuationadiNessuna valutazione finora

- Pak Taufikur CH 11 Financial Management BrighamDocumento69 paginePak Taufikur CH 11 Financial Management BrighamRidhoVerianNessuna valutazione finora

- Tugas Ekonomi Manajerial Chapter 5 The Production Process and Costs - Nely Noer Sofwati (2020318320009)Documento4 pagineTugas Ekonomi Manajerial Chapter 5 The Production Process and Costs - Nely Noer Sofwati (2020318320009)Nely Noer SofwatiNessuna valutazione finora

- Solutions Chapter 11Documento29 pagineSolutions Chapter 11Мирион НэлNessuna valutazione finora

- Resume of Chapter 6 Making Capital Investment DecisionsDocumento4 pagineResume of Chapter 6 Making Capital Investment DecisionsAimé RandrianantenainaNessuna valutazione finora

- Chapter 9-STOCK VALUATION-FIXDocumento33 pagineChapter 9-STOCK VALUATION-FIXRacing FirmanNessuna valutazione finora

- Ikea Group Yearly Summary Fy14Documento43 pagineIkea Group Yearly Summary Fy14ArraNessuna valutazione finora

- CFA Exercise With Solution - Chap 07Documento3 pagineCFA Exercise With Solution - Chap 07Fagbola Oluwatobi OmolajaNessuna valutazione finora

- Bullock Gold Mining: Corporate Finance Case StudyDocumento28 pagineBullock Gold Mining: Corporate Finance Case StudyVivek TripathyNessuna valutazione finora

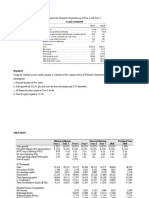

- BEIFANGDocumento10 pagineBEIFANGUmar AzizNessuna valutazione finora

- Ditta Shierlly Novierra - Minicase Conch Republic Electronics, Part 2Documento36 pagineDitta Shierlly Novierra - Minicase Conch Republic Electronics, Part 2Ummaya MalikNessuna valutazione finora

- Tugas FMCM Minggu 10 Richard Andrew - 8312419003 FixDocumento6 pagineTugas FMCM Minggu 10 Richard Andrew - 8312419003 FixsNessuna valutazione finora

- Mini Case: Stock Valuation at Ragan Engines: Disusun OlehDocumento6 pagineMini Case: Stock Valuation at Ragan Engines: Disusun OlehricaNessuna valutazione finora

- Whiz Calculator CompanyDocumento18 pagineWhiz Calculator CompanyAsibur Rahman100% (1)

- Stock Valuation: Answers To Concept Questions 1Documento15 pagineStock Valuation: Answers To Concept Questions 1Sindhu JattNessuna valutazione finora

- HOMEWORKDocumento7 pagineHOMEWORKReinaldo RoseroNessuna valutazione finora

- Chapter 2 Corporate FinanceDocumento37 pagineChapter 2 Corporate FinancediaNessuna valutazione finora

- Assignment 3 Week 3 Thecostofcapitalforgoffcomputerinc GM Drrahuldparikh 120620071214 Phpapp01Documento13 pagineAssignment 3 Week 3 Thecostofcapitalforgoffcomputerinc GM Drrahuldparikh 120620071214 Phpapp01Chris Galvez100% (1)

- Group Names:: The Cost of Capital For Goff Computer, IncDocumento6 pagineGroup Names:: The Cost of Capital For Goff Computer, IncAHMED MOHAMED YUSUFNessuna valutazione finora

- Equity Analysis and Evaluation - II Assignment December 23Documento14 pagineEquity Analysis and Evaluation - II Assignment December 23sachin.saroa.1Nessuna valutazione finora

- Group 2 - Derivatives Market in VietnamDocumento5 pagineGroup 2 - Derivatives Market in VietnamNhật HạNessuna valutazione finora

- Incoterms: Group 2 - Banking 59Documento27 pagineIncoterms: Group 2 - Banking 59Nhật HạNessuna valutazione finora

- International Sales ContractDocumento39 pagineInternational Sales ContractNhật HạNessuna valutazione finora

- International Sales ContractDocumento20 pagineInternational Sales ContractNhật HạNessuna valutazione finora

- Monetary and Finance TheoriesDocumento29 pagineMonetary and Finance TheoriesNhật HạNessuna valutazione finora

- Lesson 4Documento45 pagineLesson 4Nhật HạNessuna valutazione finora

- Micro EconomicDocumento9 pagineMicro EconomicNhật HạNessuna valutazione finora

- Determination of Physicochemical Pollutants in Wastewater and Some Food Crops Grown Along Kakuri Brewery Wastewater Channels, Kaduna State, NigeriaDocumento5 pagineDetermination of Physicochemical Pollutants in Wastewater and Some Food Crops Grown Along Kakuri Brewery Wastewater Channels, Kaduna State, NigeriamiguelNessuna valutazione finora

- PH Water On Stability PesticidesDocumento6 paginePH Water On Stability PesticidesMontoya AlidNessuna valutazione finora

- Didhard Muduni Mparo and 8 Others Vs The GRN of Namibia and 6 OthersDocumento20 pagineDidhard Muduni Mparo and 8 Others Vs The GRN of Namibia and 6 OthersAndré Le RouxNessuna valutazione finora

- Chapter 14ADocumento52 pagineChapter 14Arajan35Nessuna valutazione finora

- The Problem Between Teacher and Students: Name: Dinda Chintya Sinaga (2152121008) Astry Iswara Kelana Citra (2152121005)Documento3 pagineThe Problem Between Teacher and Students: Name: Dinda Chintya Sinaga (2152121008) Astry Iswara Kelana Citra (2152121005)Astry Iswara Kelana CitraNessuna valutazione finora

- Thick Teak PVT LTD Aoa and MoaDocumento17 pagineThick Teak PVT LTD Aoa and MoaVj EnthiranNessuna valutazione finora

- FACT SHEET KidZaniaDocumento4 pagineFACT SHEET KidZaniaKiara MpNessuna valutazione finora

- 6977 - Read and Answer The WorksheetDocumento1 pagina6977 - Read and Answer The Worksheetmohamad aliNessuna valutazione finora

- The Trial of Jesus ChristDocumento10 pagineThe Trial of Jesus ChristTomaso Vialardi di Sandigliano100% (2)

- DODGER: Book Club GuideDocumento2 pagineDODGER: Book Club GuideEpicReadsNessuna valutazione finora

- Vocabulary Inglés.Documento14 pagineVocabulary Inglés.Psicoguía LatacungaNessuna valutazione finora

- What A Wonderful WorldDocumento2 pagineWhat A Wonderful WorldDraganaNessuna valutazione finora

- 5.4 Marketing Arithmetic For Business AnalysisDocumento12 pagine5.4 Marketing Arithmetic For Business AnalysisashNessuna valutazione finora

- Problem Based LearningDocumento23 pagineProblem Based Learningapi-645777752Nessuna valutazione finora

- Komatsu Hydraulic Excavator Pc290lc 290nlc 6k Shop ManualDocumento20 pagineKomatsu Hydraulic Excavator Pc290lc 290nlc 6k Shop Manualmallory100% (47)

- RPS Manajemen Keuangan IIDocumento2 pagineRPS Manajemen Keuangan IIaulia endiniNessuna valutazione finora

- James Ellroy PerfidiaDocumento4 pagineJames Ellroy PerfidiaMichelly Cristina SilvaNessuna valutazione finora

- Judicial Review of Legislative ActionDocumento14 pagineJudicial Review of Legislative ActionAnushka SinghNessuna valutazione finora

- Knowledge, Attitude and Practice of Non-Allied Health Sciences Students of Southwestern University Phinma During The Covid-19 PandemicDocumento81 pagineKnowledge, Attitude and Practice of Non-Allied Health Sciences Students of Southwestern University Phinma During The Covid-19 Pandemicgeorgemayhew1030Nessuna valutazione finora

- Trainee'S Record Book: Technical Education and Skills Development Authority (Your Institution)Documento17 pagineTrainee'S Record Book: Technical Education and Skills Development Authority (Your Institution)Ronald Dequilla PacolNessuna valutazione finora

- Law - Midterm ExamDocumento2 pagineLaw - Midterm ExamJulian Mernando vlogsNessuna valutazione finora

- Forensic BallisticsDocumento23 pagineForensic BallisticsCristiana Jsu DandanNessuna valutazione finora

- Tim Horton's Case StudyDocumento8 pagineTim Horton's Case Studyhiba harizNessuna valutazione finora

- Contoh Rancangan Pengajaran Harian (RPH)Documento7 pagineContoh Rancangan Pengajaran Harian (RPH)Farees Ashraf Bin ZahriNessuna valutazione finora

- God's Word in Holy Citadel New Jerusalem" Monastery, Glodeni - Romania, Redactor Note. Translated by I.ADocumento6 pagineGod's Word in Holy Citadel New Jerusalem" Monastery, Glodeni - Romania, Redactor Note. Translated by I.Abillydean_enNessuna valutazione finora

- Lyndhurst OPRA Request FormDocumento4 pagineLyndhurst OPRA Request FormThe Citizens CampaignNessuna valutazione finora

- Rotation and Revolution of EarthDocumento4 pagineRotation and Revolution of EarthRamu ArunachalamNessuna valutazione finora

- EFL Listeners' Strategy Development and Listening Problems: A Process-Based StudyDocumento22 pagineEFL Listeners' Strategy Development and Listening Problems: A Process-Based StudyCom DigfulNessuna valutazione finora

- Project CharterDocumento10 pagineProject CharterAdnan AhmedNessuna valutazione finora

- Quizo Yupanqui StoryDocumento8 pagineQuizo Yupanqui StoryrickfrombrooklynNessuna valutazione finora