Potrebbero piacerti anche

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- 08 Chapter 2Documento66 pagine08 Chapter 2Ravi GuptaNessuna valutazione finora

- ST Book 9th Edition TAXGURUDocumento805 pagineST Book 9th Edition TAXGURUaddy31Nessuna valutazione finora

- Dashboard Februari 2021Documento992 pagineDashboard Februari 2021KanasfiNessuna valutazione finora

- Eop (4Documento8 pagineEop (4Andres ChavarrioNessuna valutazione finora

- Income tax deductions under 40 charsDocumento4 pagineIncome tax deductions under 40 charsAgie MarquezNessuna valutazione finora

- User account creation and payment authorization flowDocumento1 paginaUser account creation and payment authorization flowRafael KrappNessuna valutazione finora

- Chapter 7 - Business Taxes Flashcards - QuizletDocumento9 pagineChapter 7 - Business Taxes Flashcards - QuizletBisag AsaNessuna valutazione finora

- Transactions 650 344366000 20200827 200640 PDFDocumento15 pagineTransactions 650 344366000 20200827 200640 PDFKiran AdhikariNessuna valutazione finora

- EntityDocumento1 paginaEntitysveerkarNessuna valutazione finora

- Tax invoice for furniture purchaseDocumento1 paginaTax invoice for furniture purchaseRajnish JainNessuna valutazione finora

- Invoice: (Original)Documento1 paginaInvoice: (Original)azmatNessuna valutazione finora

- View - Download Savings Bank StatementDocumento1 paginaView - Download Savings Bank Statementpravallika aNessuna valutazione finora

- BAB 2 Analisis TransaksiDocumento84 pagineBAB 2 Analisis TransaksiScouter SejatiNessuna valutazione finora

- Dip 27Documento5 pagineDip 27Aimms AimmsNessuna valutazione finora

- File 3Documento3 pagineFile 3Ivan GrahamNessuna valutazione finora

- Credit Card Fact SheetDocumento2 pagineCredit Card Fact SheetEthelyn SalternNessuna valutazione finora

- Nego Notes 1Documento19 pagineNego Notes 1Ariane AquinoNessuna valutazione finora

- Chartering TermsDocumento4 pagineChartering TermsCarlos Alberto Zamorano PizarroNessuna valutazione finora

- Pil Mumbai Private Limited: Schedule of Local ChargesDocumento1 paginaPil Mumbai Private Limited: Schedule of Local ChargesANMOL SUKHDEVENessuna valutazione finora

- GST Seminar Key HighlightsDocumento40 pagineGST Seminar Key HighlightsNavneetNessuna valutazione finora

- PDFDocumento2 paginePDFjagjit singhNessuna valutazione finora

- RR 10-2015Documento6 pagineRR 10-2015dan2aurusNessuna valutazione finora

- printPaymentReceipt HTML PDFDocumento1 paginaprintPaymentReceipt HTML PDFvrkotsNessuna valutazione finora

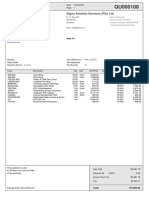

- Signa Aviation Services (Pty) LTD: Bill To: Ship ToDocumento1 paginaSigna Aviation Services (Pty) LTD: Bill To: Ship ToForexx 101Nessuna valutazione finora

- Bunna International Bank S.C Debit Card Personalization RequestDocumento3 pagineBunna International Bank S.C Debit Card Personalization RequestSolomon TekalignNessuna valutazione finora

- Bank StatementDocumento4 pagineBank Statementsulaimon2023Nessuna valutazione finora

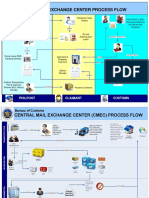

- Central Mail Exchange Center Process FlowDocumento4 pagineCentral Mail Exchange Center Process FlowMa Angela MamarilNessuna valutazione finora

- Fundamentals of AccountingDocumento2 pagineFundamentals of AccountingLhyn Cantal Calica100% (2)

- Statement of AccountDocumento52 pagineStatement of AccountKhalil AfghanNessuna valutazione finora

- Group Health Insurance Plans in India - SANADocumento5 pagineGroup Health Insurance Plans in India - SANArohan kumarNessuna valutazione finora