Potrebbero piacerti anche

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Understanding Life Insurance Products From PivotDocumento4 pagineUnderstanding Life Insurance Products From PivotYekini KazeemNessuna valutazione finora

- 1 FAQs FinacleDocumento17 pagine1 FAQs FinacleVikramNessuna valutazione finora

- Department of Labor: 96 19484Documento5 pagineDepartment of Labor: 96 19484USA_DepartmentOfLaborNessuna valutazione finora

- Lamya Yusuf Jhumur BUS498.37 Internship Report Summer2021..Documento29 pagineLamya Yusuf Jhumur BUS498.37 Internship Report Summer2021..Nazia ElhamNessuna valutazione finora

- Ajay YadavDocumento146 pagineAjay Yadav9415697349Nessuna valutazione finora

- P3 Pertemuan 3Documento8 pagineP3 Pertemuan 3Ahsan FirdausNessuna valutazione finora

- Answers To TestsDocumento19 pagineAnswers To TestsАнтон ВасильевNessuna valutazione finora

- Rizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)Documento2 pagineRizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)faheemNessuna valutazione finora

- Assignment / Tugasan - Financial AccountingDocumento10 pagineAssignment / Tugasan - Financial Accountinghemavathy0% (1)

- The Abcs of Abs: Portfolio Strategy ResearchDocumento20 pagineThe Abcs of Abs: Portfolio Strategy ResearchYusuf Utomo100% (2)

- Shorter Life Expectancy Gives UK Pensions An Unexpected Windfall - Financial TimesDocumento4 pagineShorter Life Expectancy Gives UK Pensions An Unexpected Windfall - Financial TimesAleksandar SpasojevicNessuna valutazione finora

- Mancon Test QuestionsDocumento2 pagineMancon Test QuestionsIsaiah CruzNessuna valutazione finora

- Cost Chapter FourDocumento28 pagineCost Chapter FourDEREJENessuna valutazione finora

- Compound Interest Installment PDFDocumento36 pagineCompound Interest Installment PDFnileshmpharmNessuna valutazione finora

- Cheque Petition IN MVOP 281 of 2009 (P-4)Documento3 pagineCheque Petition IN MVOP 281 of 2009 (P-4)rkjayakumar7639Nessuna valutazione finora

- Acct Statement - XX3940 - 09082023 (1) - LDocumento22 pagineAcct Statement - XX3940 - 09082023 (1) - LTHE CAMBRIDGENessuna valutazione finora

- Chapter 10 Share Capital Transactions Subsequent To Original Issuance Exercises 15 ItemsDocumento7 pagineChapter 10 Share Capital Transactions Subsequent To Original Issuance Exercises 15 ItemsdmangiginNessuna valutazione finora

- Exam 4 Fin 2020 - 2Documento2 pagineExam 4 Fin 2020 - 2samaresh chhotrayNessuna valutazione finora

- M/s Rishabh Creations Sikka Knitting FabDocumento1 paginaM/s Rishabh Creations Sikka Knitting FabVarun AgarwalNessuna valutazione finora

- Reference: Financial Accounting - 2 by Conrado T. Valix and Christian ValixDocumento2 pagineReference: Financial Accounting - 2 by Conrado T. Valix and Christian ValixMie CuarteroNessuna valutazione finora

- LIBF Level 4 Certificate For Documentary Credit Specialists (CDCS)Documento30 pagineLIBF Level 4 Certificate For Documentary Credit Specialists (CDCS)Abhay PandereNessuna valutazione finora

- Axis Bank AptitudeDocumento94 pagineAxis Bank AptitudeladmohanNessuna valutazione finora

- Ashford Bus401 Week 1 4 Quiz and Practice QuestionsDocumento15 pagineAshford Bus401 Week 1 4 Quiz and Practice QuestionsDoreenNessuna valutazione finora

- Sa1 Ae 121 - TheoriesDocumento6 pagineSa1 Ae 121 - TheoriesMariette Alex AgbanlogNessuna valutazione finora

- Loan CalculatorDocumento6 pagineLoan CalculatorAbegail habalNessuna valutazione finora

- ComplaintDocumento25 pagineComplaintThe GuardianNessuna valutazione finora

- Tugas Sesi 4Documento3 pagineTugas Sesi 4mutmainnahNessuna valutazione finora

- PGPM 2023 Time Value Problem Set v1.2Documento20 paginePGPM 2023 Time Value Problem Set v1.2Jayanth DeshmukhNessuna valutazione finora

- Chapter 2 - Advanced AccDocumento15 pagineChapter 2 - Advanced AccAsad KhadarNessuna valutazione finora

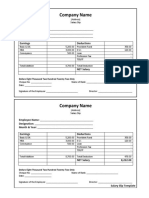

- Company Paystub Salary Slip Template Free Word FormatDocumento1 paginaCompany Paystub Salary Slip Template Free Word FormatdilipomiNessuna valutazione finora