Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- POS301.R - Topic7Worksheet-8-29-16 CompleteDocumento3 paginePOS301.R - Topic7Worksheet-8-29-16 Completetama00018Nessuna valutazione finora

- 1701 Bir Form 2006 2013-2019Documento11 pagine1701 Bir Form 2006 2013-2019Jessie Boy Balino BalderamaNessuna valutazione finora

- Invoice - Apple Airpods ProDocumento1 paginaInvoice - Apple Airpods ProKrish JaiswalNessuna valutazione finora

- Tax Remedies Flowchart (Revised)Documento6 pagineTax Remedies Flowchart (Revised)GersonGamas0% (1)

- Procedure in Computing Vanishing DeductionDocumento5 pagineProcedure in Computing Vanishing DeductionDon Tiansay100% (5)

- Buddha Institute of Technology: Walk-in-Interview For Faculty PositionDocumento1 paginaBuddha Institute of Technology: Walk-in-Interview For Faculty Positionkd vlogsNessuna valutazione finora

- Wa0013Documento3 pagineWa0013kd vlogsNessuna valutazione finora

- Personal Details: Examination Form View Form PDF Hall TicketDocumento2 paginePersonal Details: Examination Form View Form PDF Hall Ticketkd vlogsNessuna valutazione finora

- Chhattisgarh Swami Vivekanand Technical University, Bhilai: Student DetailsDocumento3 pagineChhattisgarh Swami Vivekanand Technical University, Bhilai: Student Detailskd vlogsNessuna valutazione finora

- Optimization Methods TheoryDocumento28 pagineOptimization Methods Theorykd vlogsNessuna valutazione finora

- 1.swami Vivekanand Yuva Kaushal Setu An Initiative of CSVTUDocumento6 pagine1.swami Vivekanand Yuva Kaushal Setu An Initiative of CSVTUkd vlogsNessuna valutazione finora

- NSDC Annual Update 2014-15Documento56 pagineNSDC Annual Update 2014-15kd vlogsNessuna valutazione finora

- STRIVE PhaseDocumento10 pagineSTRIVE Phasekd vlogsNessuna valutazione finora

- List of ITIsDocumento13 pagineList of ITIskd vlogsNessuna valutazione finora

- Research Lab Ass. Sem2Documento27 pagineResearch Lab Ass. Sem2kd vlogsNessuna valutazione finora

- Front Page"a Study On Consumers' Buying Decision Towards Hyundai I20Documento2 pagineFront Page"a Study On Consumers' Buying Decision Towards Hyundai I20kd vlogsNessuna valutazione finora

- Chapter - 1: Project & Viva-Voceroll No.:74500240102017-18Documento18 pagineChapter - 1: Project & Viva-Voceroll No.:74500240102017-18kd vlogsNessuna valutazione finora

- INVOICE: INV44692504 Customer #52693642Documento1 paginaINVOICE: INV44692504 Customer #52693642Sandy TessierNessuna valutazione finora

- CN No. CN Date Inv - No. Pkgs Truck No. Reporting Date Delivery Date Wt. Rate Total FreightDocumento1 paginaCN No. CN Date Inv - No. Pkgs Truck No. Reporting Date Delivery Date Wt. Rate Total FreightRohit Parmar (Computer Operator, Bangalore)Nessuna valutazione finora

- Income Taxes: Sri Lanka Accounting Standard - LKAS 12Documento46 pagineIncome Taxes: Sri Lanka Accounting Standard - LKAS 12Sineth NeththasingheNessuna valutazione finora

- Liabilities RS. Assets RS.: A. Balance Sheet of The Sarvodaya Sahakari Bank Ltd. For The Year Ended On 31 MARCH, 2006Documento3 pagineLiabilities RS. Assets RS.: A. Balance Sheet of The Sarvodaya Sahakari Bank Ltd. For The Year Ended On 31 MARCH, 2006bhaveshpipaliyaNessuna valutazione finora

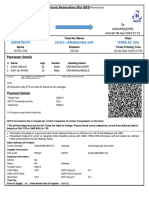

- Tez Ticket PrintDocumento1 paginaTez Ticket Printosama amjad.hy8ggNessuna valutazione finora

- CS Executive Tax Laws Amendments by Vipul ShahDocumento41 pagineCS Executive Tax Laws Amendments by Vipul ShahCloxan India Pvt LtdNessuna valutazione finora

- Payroll Process Flow Job AidDocumento1 paginaPayroll Process Flow Job AidtolgaevilNessuna valutazione finora

- 2015-2018 Tax Bar QuestionsDocumento42 pagine2015-2018 Tax Bar QuestionsDenver Dela Cruz PadrigoNessuna valutazione finora

- AE23 Capital BudgetingDocumento4 pagineAE23 Capital BudgetingCheska AgrabioNessuna valutazione finora

- Income Taxation Quiz 1Documento2 pagineIncome Taxation Quiz 1Yi Zara100% (1)

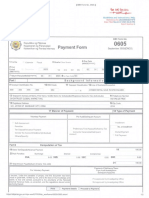

- Payment FormDocumento4 paginePayment FormRodel Rivera VelascoNessuna valutazione finora

- 5.4 SECTION 80C To 80UDocumento5 pagine5.4 SECTION 80C To 80UYash DedhiaNessuna valutazione finora

- InvoiceDocumento1 paginaInvoiceSalman KhanNessuna valutazione finora

- GSTR-9 AND GSTR-9C - OutwardDocumento39 pagineGSTR-9 AND GSTR-9C - OutwardRahul KLNessuna valutazione finora

- Employee Details Payment & Leave Details: Arrears Current AmountDocumento1 paginaEmployee Details Payment & Leave Details: Arrears Current AmountBalajiNessuna valutazione finora

- ISE 2040 Excel HWDocumento20 pagineISE 2040 Excel HWPatch HavanasNessuna valutazione finora

- CA Final Test Paper-1Documento4 pagineCA Final Test Paper-1anjana2734Nessuna valutazione finora

- WWW - Humanservices.gov - Au SPW Customer Forms Resources Modjy-1211enDocumento17 pagineWWW - Humanservices.gov - Au SPW Customer Forms Resources Modjy-1211enLeslie BrownNessuna valutazione finora

- G.R. NO. 190102 ACCENTURE, INC., Petitioner,: PrincipleDocumento3 pagineG.R. NO. 190102 ACCENTURE, INC., Petitioner,: PrincipleEmmanuel BurcerNessuna valutazione finora

- TAX Quiz 2Documento8 pagineTAX Quiz 2Pearl Jade YecyecNessuna valutazione finora

- Durga Malleswara RaoDocumento1 paginaDurga Malleswara RaoRajesh pvkNessuna valutazione finora

- Earnings Deductions: Eicher Motors LimitedDocumento1 paginaEarnings Deductions: Eicher Motors LimitedBarath BiberNessuna valutazione finora

- REG Exam Format - CPADocumento1 paginaREG Exam Format - CPAgavkaNessuna valutazione finora

- 2016 Itr1 PR7 PDFDocumento5 pagine2016 Itr1 PR7 PDFVyankatesh KurriNessuna valutazione finora

- Goods and Service Tax Act, 2017Documento4 pagineGoods and Service Tax Act, 2017shivani yadavNessuna valutazione finora