Potrebbero piacerti anche

- Export-Import Bank of India: Catalysing India'S Trade and InvestmentDocumento11 pagineExport-Import Bank of India: Catalysing India'S Trade and Investmentershad123Nessuna valutazione finora

- The Thirsty Crow Story in Hindi PDFDocumento2 pagineThe Thirsty Crow Story in Hindi PDFershad123100% (3)

- MC 101Documento720 pagineMC 101Anamika Rai PandeyNessuna valutazione finora

- Lessons From Three Countries: Working Paper No. 8Documento44 pagineLessons From Three Countries: Working Paper No. 8ershad123Nessuna valutazione finora

- Report - 9th CII-EXIM Bank India-Africa Conclave 2013Documento60 pagineReport - 9th CII-EXIM Bank India-Africa Conclave 2013ershad123Nessuna valutazione finora

- Red FM 93.5Documento3 pagineRed FM 93.5ershad123Nessuna valutazione finora

- CRISILDocumento2 pagineCRISILershad123Nessuna valutazione finora

- Annual Report 2011-12Documento156 pagineAnnual Report 2011-12ershad123Nessuna valutazione finora

- Bin CardDocumento2 pagineBin Cardershad123100% (1)

- Report - 9th CII-EXIM Bank India-Africa Conclave 2013Documento60 pagineReport - 9th CII-EXIM Bank India-Africa Conclave 2013ershad123Nessuna valutazione finora

- Methods of TrainingDocumento3 pagineMethods of Trainingershad123Nessuna valutazione finora

- Functional StructureDocumento2 pagineFunctional Structureershad123Nessuna valutazione finora

- MCS Notes (MBA)Documento88 pagineMCS Notes (MBA)prashantsmartie100% (20)

- Methods of TrainingDocumento3 pagineMethods of Trainingershad123Nessuna valutazione finora

- Points Forward Contract Futures Contract: MeaningDocumento6 paginePoints Forward Contract Futures Contract: Meaningershad123Nessuna valutazione finora

- Evolution of Banking - IndiaDocumento29 pagineEvolution of Banking - Indiaershad123Nessuna valutazione finora

- Methods of TrainingDocumento3 pagineMethods of Trainingershad123Nessuna valutazione finora

- Portfolio ManagementDocumento75 paginePortfolio Managementsheemankhan82% (17)

- Evolution of Banking - IndiaDocumento29 pagineEvolution of Banking - Indiaershad123Nessuna valutazione finora

- SR2Documento58 pagineSR2ershad123Nessuna valutazione finora

- MotivationDocumento29 pagineMotivationershad123Nessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (120)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Income Tax Banggawan2019 Ch9Documento13 pagineIncome Tax Banggawan2019 Ch9Noreen Ledda83% (6)

- Customer Loyalty AttributesDocumento25 pagineCustomer Loyalty Attributesmr_gelda6183Nessuna valutazione finora

- BSC Charting Proposal For Banglar JoyjatraDocumento12 pagineBSC Charting Proposal For Banglar Joyjatrarabi4457Nessuna valutazione finora

- Project On Rewards Recognition Schemes Staff Officers HLLDocumento56 pagineProject On Rewards Recognition Schemes Staff Officers HLLRoyal Projects100% (4)

- Notes On b2b BusinessDocumento7 pagineNotes On b2b Businesssneha pathakNessuna valutazione finora

- 1.introduction To Operations Management PDFDocumento7 pagine1.introduction To Operations Management PDFEmmanuel Okena67% (3)

- SAP ISR Course ContentDocumento1 paginaSAP ISR Course ContentSandeep SharmaaNessuna valutazione finora

- A Study On Labour Absenteeism in Ammarun Foundries Coimbatore-QuestionnaireDocumento4 pagineA Study On Labour Absenteeism in Ammarun Foundries Coimbatore-QuestionnaireSUKUMAR75% (8)

- Lessons 1 and 2 Review IBM Coursera TestDocumento6 pagineLessons 1 and 2 Review IBM Coursera TestNueNessuna valutazione finora

- Idx Monthly StatsticsDocumento113 pagineIdx Monthly StatsticsemmaryanaNessuna valutazione finora

- ISA 701 MindMapDocumento1 paginaISA 701 MindMapAli HaiderNessuna valutazione finora

- Business Development Sales Manager in Colorado Springs CO Resume Rick KlopenstineDocumento2 pagineBusiness Development Sales Manager in Colorado Springs CO Resume Rick KlopenstineRick KlopenstineNessuna valutazione finora

- AideD&D n5 Basse-Tour (Suite Pour Un Diamant)Documento7 pagineAideD&D n5 Basse-Tour (Suite Pour Un Diamant)Etan KrelNessuna valutazione finora

- Management Accounting Perspective: © Mcgraw-Hill EducationDocumento12 pagineManagement Accounting Perspective: © Mcgraw-Hill Educationabeer alfalehNessuna valutazione finora

- Business CombinationDocumento20 pagineBusiness CombinationabhaybittuNessuna valutazione finora

- Resort Management System For ProjectDocumento15 pagineResort Management System For ProjectSachin Kulkarni100% (5)

- Forex Investor AgreementDocumento8 pagineForex Investor AgreementForex Mentor100% (3)

- Final QARSHI REPORTDocumento31 pagineFinal QARSHI REPORTUzma Khan100% (2)

- Abstract Mini Projects 2016Documento91 pagineAbstract Mini Projects 2016Sikkandhar JabbarNessuna valutazione finora

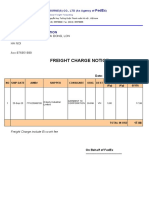

- Freight Charge Notice: To: Garment 10 CorporationDocumento4 pagineFreight Charge Notice: To: Garment 10 CorporationThuy HoangNessuna valutazione finora

- Exemption Certificate - SalesDocumento2 pagineExemption Certificate - SalesExecutive F&ADADUNessuna valutazione finora

- Modern OfficeDocumento10 pagineModern OfficesonuNessuna valutazione finora

- Report On Financial Market Review by The Hong Kong SAR Government in April 1998Documento223 pagineReport On Financial Market Review by The Hong Kong SAR Government in April 1998Tsang Shu-kiNessuna valutazione finora

- 01 Activity 1 - ARG: Facility Management Concepcion, Stephanie Kyle S. BM303Documento2 pagine01 Activity 1 - ARG: Facility Management Concepcion, Stephanie Kyle S. BM303Stephanie Kyle Concepcion100% (3)

- Chapter 2 Management Accounting Hansen Mowen PDFDocumento28 pagineChapter 2 Management Accounting Hansen Mowen PDFidka100% (1)

- Gujarat Technological University: Comprehensive Project ReportDocumento32 pagineGujarat Technological University: Comprehensive Project ReportDharmesh PatelNessuna valutazione finora

- Finacle - CommandsDocumento5 pagineFinacle - CommandsvpsrnthNessuna valutazione finora

- The Implications of Globalisation For Consumer AttitudesDocumento2 pagineThe Implications of Globalisation For Consumer AttitudesIvan Luis100% (1)

- Niraj-LSB CatalogueDocumento8 pagineNiraj-LSB CataloguenirajNessuna valutazione finora

- MKT 460 CH 1 Seh Defining Marketing For The 21st CenturyDocumento56 pagineMKT 460 CH 1 Seh Defining Marketing For The 21st CenturyRifat ChowdhuryNessuna valutazione finora