Potrebbero piacerti anche

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- BACEN wps7Documento48 pagineBACEN wps7marceloscarvalhoNessuna valutazione finora

- Revista 71 PDFDocumento183 pagineRevista 71 PDFAnonymous 80AZibuhBHNessuna valutazione finora

- CONTI & PRATES (2018) - The International Monetary System HierarchyDocumento47 pagineCONTI & PRATES (2018) - The International Monetary System HierarchymarceloscarvalhoNessuna valutazione finora

- Cepal: ReviewDocumento10 pagineCepal: ReviewmarceloscarvalhoNessuna valutazione finora

- Bellamy Foster - Theories-of-Capitalist-Transformation-Critical-Notes-on-the-Comparison-of-Marx-and-SchumpeterDocumento5 pagineBellamy Foster - Theories-of-Capitalist-Transformation-Critical-Notes-on-the-Comparison-of-Marx-and-SchumpetermarceloscarvalhoNessuna valutazione finora

- Evolving International Financial MarketsDocumento44 pagineEvolving International Financial MarketsmarceloscarvalhoNessuna valutazione finora

- BACEN wps3Documento22 pagineBACEN wps3marceloscarvalhoNessuna valutazione finora

- PRATES (2017) - Monetary Sovereignty, Currency Hierarchy and Policy Space - A Post-Keynesian ApproachDocumento47 paginePRATES (2017) - Monetary Sovereignty, Currency Hierarchy and Policy Space - A Post-Keynesian ApproachmarceloscarvalhoNessuna valutazione finora

- Financial Crisis and Policy ResponsesDocumento37 pagineFinancial Crisis and Policy ResponsesmarceloscarvalhoNessuna valutazione finora

- The Euro and The DollarDocumento81 pagineThe Euro and The DollarmarceloscarvalhoNessuna valutazione finora

- Evolving International Financial MarketsDocumento44 pagineEvolving International Financial MarketsmarceloscarvalhoNessuna valutazione finora

- Banking and CommerceDocumento34 pagineBanking and CommercemarceloscarvalhoNessuna valutazione finora

- BIS Work91 PDFDocumento46 pagineBIS Work91 PDFmarceloscarvalhoNessuna valutazione finora

- Monetary Policy in Low InflationDocumento58 pagineMonetary Policy in Low InflationmarceloscarvalhoNessuna valutazione finora

- Bank Lending To Emerging MarketsDocumento47 pagineBank Lending To Emerging MarketsmarceloscarvalhoNessuna valutazione finora

- Predicting RecessionsDocumento30 paginePredicting RecessionsmarceloscarvalhoNessuna valutazione finora

- The DollarDocumento27 pagineThe DollarmarceloscarvalhoNessuna valutazione finora

- Bader (2013) - The End of Democratic CapitalismDocumento7 pagineBader (2013) - The End of Democratic CapitalismmarceloscarvalhoNessuna valutazione finora

- Tugan-Baranovsky (1910) - Modern Socialism in Its Historical DevelopmentDocumento248 pagineTugan-Baranovsky (1910) - Modern Socialism in Its Historical DevelopmentmarceloscarvalhoNessuna valutazione finora

- Bhaduri & Marglin (1990)Documento20 pagineBhaduri & Marglin (1990)marceloscarvalhoNessuna valutazione finora

- Epstein & Schor (1988) PDFDocumento77 pagineEpstein & Schor (1988) PDFmarceloscarvalhoNessuna valutazione finora

- Karl PolanyiDocumento18 pagineKarl PolanyimarceloscarvalhoNessuna valutazione finora

- SHIXUE (2003) - Third World Approach To Globalization - Comparing Latin America and ChinaDocumento9 pagineSHIXUE (2003) - Third World Approach To Globalization - Comparing Latin America and ChinamarceloscarvalhoNessuna valutazione finora

- Minsky (2013) - The Relevance of Kalecki - The Useable Contribution PDFDocumento12 pagineMinsky (2013) - The Relevance of Kalecki - The Useable Contribution PDFmarceloscarvalhoNessuna valutazione finora

- Godley (1992) - Maastricht and All ThatDocumento5 pagineGodley (1992) - Maastricht and All ThatmarceloscarvalhoNessuna valutazione finora

- Minsky (2013) - The Relevance of Kalecki - The Useable Contribution PDFDocumento12 pagineMinsky (2013) - The Relevance of Kalecki - The Useable Contribution PDFmarceloscarvalhoNessuna valutazione finora

- 2014 UN Social Panorama ALyCDocumento285 pagine2014 UN Social Panorama ALyCEdgar EslavaNessuna valutazione finora

- FAJNZYLBER (1981) - Some Reflections On South-East Asian Export IndustrializationDocumento24 pagineFAJNZYLBER (1981) - Some Reflections On South-East Asian Export IndustrializationmarceloscarvalhoNessuna valutazione finora

- SdarticleDocumento32 pagineSdarticlemarceloscarvalhoNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- International Economics II - Chapter 1Documento56 pagineInternational Economics II - Chapter 1seid sufiyanNessuna valutazione finora

- Macroeconomy - FMCG Update Q4 17 (JHHP) PDFDocumento46 pagineMacroeconomy - FMCG Update Q4 17 (JHHP) PDFBerry PakpahanNessuna valutazione finora

- National Income - TMKDocumento3 pagineNational Income - TMKKuthubudeen T MNessuna valutazione finora

- Central Banking & Monetary Policy SyllabusDocumento3 pagineCentral Banking & Monetary Policy SyllabusCielo ObriqueNessuna valutazione finora

- AP Macroeconomics Assignment: Apply Knowledge of UnemploymentDocumento2 pagineAP Macroeconomics Assignment: Apply Knowledge of UnemploymentSixPennyUnicorn0% (1)

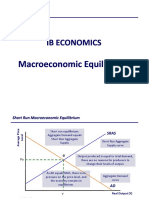

- IB MACRO EQUILIBRIUMDocumento13 pagineIB MACRO EQUILIBRIUMPablo Torrecilla100% (1)

- Pros Cons: CapitalismDocumento5 paginePros Cons: CapitalismAlejandro Sanchez ArequipaNessuna valutazione finora

- Foundations of Business: Chapter - 1Documento50 pagineFoundations of Business: Chapter - 1Petfeo SuNessuna valutazione finora

- Fisher' Equation of ExchangeDocumento5 pagineFisher' Equation of ExchangeDHWANI DEDHIANessuna valutazione finora

- Chapter 8 Myfinancelab Solutions Pearsoncmgcom PDFDocumento89 pagineChapter 8 Myfinancelab Solutions Pearsoncmgcom PDFChristopher Carpenter100% (7)

- Dovish Vs HawkishDocumento9 pagineDovish Vs Hawkisharti guptaNessuna valutazione finora

- 4676Documento2 pagine4676Sana KanNessuna valutazione finora

- Factors of Regional CompetitivenessDocumento184 pagineFactors of Regional CompetitivenessLance MorilloNessuna valutazione finora

- Mini Exam 2Documento16 pagineMini Exam 2course101Nessuna valutazione finora

- Tutorial 4 Solution PDFDocumento5 pagineTutorial 4 Solution PDFRoite BeteroNessuna valutazione finora

- Principles of Macroeconomics GDPDocumento31 paginePrinciples of Macroeconomics GDPAlice LorenNessuna valutazione finora

- International Monetary SystemDocumento16 pagineInternational Monetary Systemriyaskalpetta100% (2)

- AP Exam Past Exam PaperDocumento3 pagineAP Exam Past Exam PaperAnnaLuxeNessuna valutazione finora

- Balance of PaymentDocumento15 pagineBalance of PaymentShanaya GiriNessuna valutazione finora

- Simple Interest Loan Calculator: BorrowerDocumento8 pagineSimple Interest Loan Calculator: BorrowerPresident DhakaGrandNessuna valutazione finora

- Resource Allocation in Market and Mixed SystemsDocumento15 pagineResource Allocation in Market and Mixed SystemsxebomeNessuna valutazione finora

- © Oxford Fajar Sdn. Bhd. (008974-T), 2013 13 - 1: Principles of EconomicsDocumento20 pagine© Oxford Fajar Sdn. Bhd. (008974-T), 2013 13 - 1: Principles of EconomicsNür FátíhàhNessuna valutazione finora

- The Business Cycle: Definition and PhasesDocumento4 pagineThe Business Cycle: Definition and PhasesIshida KeikoNessuna valutazione finora

- Outlook: Asian DevelopmentDocumento301 pagineOutlook: Asian DevelopmentmaharpiciNessuna valutazione finora

- Some Basic Concepts of MacroeconomicsDocumento16 pagineSome Basic Concepts of MacroeconomicsAnvi RaiNessuna valutazione finora

- The Economic Thought of Al-Maqrizi - The Role of The Dinar and Dirham As Money - Finance in IslamDocumento7 pagineThe Economic Thought of Al-Maqrizi - The Role of The Dinar and Dirham As Money - Finance in IslamMuhammad Izzam Mohd KhazarNessuna valutazione finora

- John Maynard KeynesDocumento1 paginaJohn Maynard KeynesVidelSatanNessuna valutazione finora

- Open-Economy Macroeconomics: The Balance of Payments and Exchange RatesDocumento26 pagineOpen-Economy Macroeconomics: The Balance of Payments and Exchange RatesCharles Reginald K. HwangNessuna valutazione finora

- Reviewer in Economics: Part I: Definition of TermsDocumento4 pagineReviewer in Economics: Part I: Definition of TermsjenNessuna valutazione finora

- Consumption and Investment Functions ExplainedDocumento14 pagineConsumption and Investment Functions Explainedtamilrockers downloadNessuna valutazione finora