Potrebbero piacerti anche

- 3800 Main OMDocumento64 pagine3800 Main OMgauravNessuna valutazione finora

- 2012 Goldman ConferenceDocumento26 pagine2012 Goldman ConferenceDipo Satria RamliNessuna valutazione finora

- How We Compare Listing PresentationDocumento1 paginaHow We Compare Listing PresentationmiguelnunezNessuna valutazione finora

- UBS Technology M&A: Discussion of Current Industry TrendsDocumento19 pagineUBS Technology M&A: Discussion of Current Industry TrendsEram MeiyantoNessuna valutazione finora

- Simulasi Nilai Jabatan TikepDocumento7 pagineSimulasi Nilai Jabatan TikepAntho TaqyNessuna valutazione finora

- REAA - CPPREP4101 - Property Appraisal Report (Rawdon Hill Drive) v1.0Documento18 pagineREAA - CPPREP4101 - Property Appraisal Report (Rawdon Hill Drive) v1.0Mani Megalai SNessuna valutazione finora

- EPAM Systems Company OverviewDocumento9 pagineEPAM Systems Company OverviewMac DNessuna valutazione finora

- Top 500 E Retailer Executive List PDFDocumento37 pagineTop 500 E Retailer Executive List PDFCloud Nausor50% (2)

- Design Review Team (DRC) Site Plan Application: Sieger Suarez Architects LLCDocumento107 pagineDesign Review Team (DRC) Site Plan Application: Sieger Suarez Architects LLCthe next miamiNessuna valutazione finora

- Satisfied Clients: Your #1 Real Estate Company in SedonaDocumento1 paginaSatisfied Clients: Your #1 Real Estate Company in SedonaErika GarrowNessuna valutazione finora

- Shallow Bay Industrial Design Development and Market Trends PDFDocumento41 pagineShallow Bay Industrial Design Development and Market Trends PDFmahavirochanaNessuna valutazione finora

- Beronio Wainscot CatalogDocumento23 pagineBeronio Wainscot Catalogjiwakacau1978Nessuna valutazione finora

- UBS Pitchbook TemplateDocumento19 pagineUBS Pitchbook Templatektp24415Nessuna valutazione finora

- Cel 2022 CompensationsurveyresultsDocumento4 pagineCel 2022 Compensationsurveyresultsyjj856765Nessuna valutazione finora

- Wah Seong Corporation Berhad: More Earnings Disappointment Likely in 3Q-09/09/2010Documento4 pagineWah Seong Corporation Berhad: More Earnings Disappointment Likely in 3Q-09/09/2010Rhb InvestNessuna valutazione finora

- 2002-2008 LUXURY HOMES SOLD-7 Yr End Summaries-Mukilteo School Dist $50,000 Price Range 08-10-08Documento1 pagina2002-2008 LUXURY HOMES SOLD-7 Yr End Summaries-Mukilteo School Dist $50,000 Price Range 08-10-08Bruce W. McKinnon MBA100% (1)

- Money Matters 6 - 2011Documento4 pagineMoney Matters 6 - 2011Peggy DoviakNessuna valutazione finora

- LT 0456Documento1 paginaLT 0456gutierkNessuna valutazione finora

- San Diego Business JournalDocumento1 paginaSan Diego Business JournalmiguelnunezNessuna valutazione finora

- Fast 50 Minneapolis BLASTED 5-30-17Documento2 pagineFast 50 Minneapolis BLASTED 5-30-17Paul SkoneyNessuna valutazione finora

- Zoominfo 2Documento1 paginaZoominfo 2Aditya TamminaNessuna valutazione finora

- SSKD 111.1R T1Documento1 paginaSSKD 111.1R T1Elias JamhourNessuna valutazione finora

- Chairmans CornerDocumento3 pagineChairmans Cornerjstamp02Nessuna valutazione finora

- Ratio AnalysisDocumento32 pagineRatio AnalysisSohail SohailsaleemNessuna valutazione finora

- Berhad: Iphone A Potential Game Changer? - 11/03/2010Documento4 pagineBerhad: Iphone A Potential Game Changer? - 11/03/2010Rhb InvestNessuna valutazione finora

- 2005-2011 LAND SOLD-7 Year End Summaries-Mukilteo School Dist 50,000 Price Range 08-10-08Documento1 pagina2005-2011 LAND SOLD-7 Year End Summaries-Mukilteo School Dist 50,000 Price Range 08-10-08Bruce W. McKinnon MBANessuna valutazione finora

- US Salary Guide and Market Report 2022Documento11 pagineUS Salary Guide and Market Report 2022ismailambengueNessuna valutazione finora

- Struktur Organisasi Bank Muamalat Indonesia: Treasury DivisionDocumento60 pagineStruktur Organisasi Bank Muamalat Indonesia: Treasury DivisionSivaNabillaNessuna valutazione finora

- Template 01 Customer Relationship ManagementDocumento17 pagineTemplate 01 Customer Relationship ManagementFahmi AriyadiNessuna valutazione finora

- ALTN For SampleDocumento38 pagineALTN For SampleKanganFatimaNessuna valutazione finora

- Get Ready For Dreamforce 2019 (CF)Documento29 pagineGet Ready For Dreamforce 2019 (CF)hsadfj algioNessuna valutazione finora

- Final Presentation On India BullsDocumento17 pagineFinal Presentation On India BullsamitdhoteNessuna valutazione finora

- JAKS Resources Berhad: Powering Up-14/04/2010Documento9 pagineJAKS Resources Berhad: Powering Up-14/04/2010Rhb InvestNessuna valutazione finora

- Richmond Office Performance in DownturnsDocumento1 paginaRichmond Office Performance in DownturnsWilliam HarrisNessuna valutazione finora

- Lap PromkesDocumento197 pagineLap PromkesDesnawanta PadangNessuna valutazione finora

- Manufacturing 16 Sep 2010Documento22 pagineManufacturing 16 Sep 2010jpage9317Nessuna valutazione finora

- Empire Group 2022 Technology Salary GuideDocumento11 pagineEmpire Group 2022 Technology Salary GuideattiqqNessuna valutazione finora

- Newsbriefs 20110107Documento3 pagineNewsbriefs 20110107Maien VitalNessuna valutazione finora

- USPS Org ChartDocumento1 paginaUSPS Org ChartbsheehanNessuna valutazione finora

- Training Division Monthly Report - December 2023Documento4 pagineTraining Division Monthly Report - December 2023amanmudgal19Nessuna valutazione finora

- Salary Information - Asia: Banking & Financial Services - 2010Documento4 pagineSalary Information - Asia: Banking & Financial Services - 2010Vicky OngNessuna valutazione finora

- Fajarbaru Builder Group Berhad: To Embark On A Greenfield Hotel Project in Melaka - 31/5/2010Documento5 pagineFajarbaru Builder Group Berhad: To Embark On A Greenfield Hotel Project in Melaka - 31/5/2010Rhb InvestNessuna valutazione finora

- The New Office Landscape: Montgomery County Planning BoardDocumento50 pagineThe New Office Landscape: Montgomery County Planning BoardM-NCPPCNessuna valutazione finora

- W5 - V2 WorkingWithTables2Documento8 pagineW5 - V2 WorkingWithTables2Raj Kothari MNessuna valutazione finora

- Project 1: USD Jan FebDocumento5 pagineProject 1: USD Jan FebAnuj SachdevNessuna valutazione finora

- StoneWorld January 2021Documento76 pagineStoneWorld January 2021Aldo Vercetti JhonsonNessuna valutazione finora

- Wave1taxw2s000433 2019Documento2 pagineWave1taxw2s000433 2019Adonis TorresNessuna valutazione finora

- Structure DWGDocumento46 pagineStructure DWGLiesa StoneNessuna valutazione finora

- Michael Mauboussin E28093 Research Articles and Interviews 2017 2020 1Documento554 pagineMichael Mauboussin E28093 Research Articles and Interviews 2017 2020 1Xie Zheyuan100% (1)

- S Ebt2 102Documento1 paginaS Ebt2 102Rick PongiNessuna valutazione finora

- S Ebt2 201Documento1 paginaS Ebt2 201Rick PongiNessuna valutazione finora

- S Ebt2 101Documento1 paginaS Ebt2 101Rick PongiNessuna valutazione finora

- 2021 Budget Worksheeet 4Documento1 pagina2021 Budget Worksheeet 4staci holeNessuna valutazione finora

- Real Life. Real Answers.: NaborDocumento4 pagineReal Life. Real Answers.: Naborapi-26167871Nessuna valutazione finora

- BBVA OpenMind Libro El Proximo Paso Vida Exponencial2Documento59 pagineBBVA OpenMind Libro El Proximo Paso Vida Exponencial2giovanniNessuna valutazione finora

- LT 150: Maryland OfficesDocumento1 paginaLT 150: Maryland OfficesNationalLawJournalNessuna valutazione finora

- Perwaja Holdings Berhad: Better Quarters Ahead - 10/03/2010Documento4 paginePerwaja Holdings Berhad: Better Quarters Ahead - 10/03/2010Rhb InvestNessuna valutazione finora

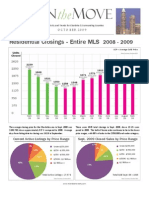

- N Ove: 2010 Residential Real Estate Forecast Residential Closings - Entire MLSDocumento4 pagineN Ove: 2010 Residential Real Estate Forecast Residential Closings - Entire MLShhesterNessuna valutazione finora

- Beverage Manufacturing Startup V04-1-DeMODocumento17 pagineBeverage Manufacturing Startup V04-1-DeMOTrịnh Minh TâmNessuna valutazione finora

- Red2 Im2-D3Documento4 pagineRed2 Im2-D3api-498580117Nessuna valutazione finora

- Avl2 ImDocumento4 pagineAvl2 Imapi-498580117Nessuna valutazione finora

- Puget Sound Brochure12Documento2 paginePuget Sound Brochure12api-498580117Nessuna valutazione finora

- Nyu Brochure 2012 Final2Documento16 pagineNyu Brochure 2012 Final2api-498580117Nessuna valutazione finora

- Hospitality For Chinese Market8Documento4 pagineHospitality For Chinese Market8api-498580117Nessuna valutazione finora

- Amit SinghDocumento111 pagineAmit Singhashish_narula30Nessuna valutazione finora

- b19 Project Final Detailes - Bangalore ListDocumento7 pagineb19 Project Final Detailes - Bangalore ListsubuninanNessuna valutazione finora

- Project in Business TaxDocumento5 pagineProject in Business TaxJemalyn PiliNessuna valutazione finora

- South-East Journal Sept 2023Documento56 pagineSouth-East Journal Sept 2023unworahNessuna valutazione finora

- Wcms 629759Documento60 pagineWcms 629759Avril FerreiraNessuna valutazione finora

- Contemporary World Intensive ReviewDocumento11 pagineContemporary World Intensive ReviewULLASIC, JUSTINE D.Nessuna valutazione finora

- A Futures Contract Based On Brent Crude OilDocumento4 pagineA Futures Contract Based On Brent Crude OilJean-Louis KouassiNessuna valutazione finora

- KMI 30 IndexDocumento27 pagineKMI 30 IndexSyed NomaanNessuna valutazione finora

- Four Green Houses... One Red HotelDocumento325 pagineFour Green Houses... One Red HotelDhruv Thakkar100% (1)

- Far 250Documento18 pagineFar 250Aisyah SaaraniNessuna valutazione finora

- Revoobit - Extended Trial Balance 2022Documento3 pagineRevoobit - Extended Trial Balance 2022NURUL AIN EDIANNessuna valutazione finora

- 09 Jitendra KumarDocumento6 pagine09 Jitendra Kumarsurya prakashNessuna valutazione finora

- Cbleecpu 12Documento8 pagineCbleecpu 12Pubg GokrNessuna valutazione finora

- Rights of An Unpaid Seller Under The Sale of Goods ActDocumento6 pagineRights of An Unpaid Seller Under The Sale of Goods ActSreepathi ShettyNessuna valutazione finora

- FM W10a 1902Documento9 pagineFM W10a 1902jonathanchristiandri2258Nessuna valutazione finora

- Learning Elt Future PDFDocumento66 pagineLearning Elt Future PDFrafanrin9783Nessuna valutazione finora

- BUSINESS MODEL-paper Recycling AND PAPER PRODUCTS INdustry-1Documento23 pagineBUSINESS MODEL-paper Recycling AND PAPER PRODUCTS INdustry-1MunuNessuna valutazione finora

- Ümmüşnur Özcan - CartwrightlumberworksheetDocumento7 pagineÜmmüşnur Özcan - CartwrightlumberworksheetUMMUSNUR OZCANNessuna valutazione finora

- Solved Problems in Engineering Economy & AccountingDocumento10 pagineSolved Problems in Engineering Economy & AccountingMiko F. Rodriguez0% (2)

- 1Documento51 pagine1dakine.kdkNessuna valutazione finora

- Using Activity-Based Costing To Manage More EffectivelyDocumento36 pagineUsing Activity-Based Costing To Manage More EffectivelynandiniNessuna valutazione finora

- Thesis MBSDocumento66 pagineThesis MBSt tableNessuna valutazione finora

- Regular Result of Bba (B I) 2015 Batch e T Exam May-June 2016Documento35 pagineRegular Result of Bba (B I) 2015 Batch e T Exam May-June 2016Parmeet SinghNessuna valutazione finora

- F-Trend: Fashion Forecast 2020 Emotional Well-BeingDocumento16 pagineF-Trend: Fashion Forecast 2020 Emotional Well-Beingdhruva7Nessuna valutazione finora

- Chapter 04 Risk, Return, and The Portfolio TheoryDocumento55 pagineChapter 04 Risk, Return, and The Portfolio TheoryAGNessuna valutazione finora

- Real EstateDocumento38 pagineReal EstateRHEA19100% (3)

- Certificate of Residency Requirements For IndividualsDocumento2 pagineCertificate of Residency Requirements For IndividualsViAnne ReyesNessuna valutazione finora

- Drivers Behind Choices 1Documento2 pagineDrivers Behind Choices 1Thuan TruongNessuna valutazione finora

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocumento5 pagineStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSandesh Pujari100% (1)

- Business Plan of Agricultural MechanizationDocumento32 pagineBusiness Plan of Agricultural MechanizationTarik Kefale86% (90)