Potrebbero piacerti anche

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Media Conglomerate PaperDocumento6 pagineMedia Conglomerate PaperLauren K. MeltonNessuna valutazione finora

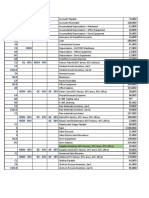

- Sales 140, 800 Less: Cost of Sales (84, 480) Gross ProfitDocumento5 pagineSales 140, 800 Less: Cost of Sales (84, 480) Gross ProfitMichaela KowalskiNessuna valutazione finora

- Taxation Case DigestDocumento34 pagineTaxation Case DigestPau PerezNessuna valutazione finora

- FIN2004 - 2704 Week 2 SlidesDocumento60 pagineFIN2004 - 2704 Week 2 SlidesJalen GohNessuna valutazione finora

- fs4q19 Erajaya Swasembada TBK Billingual 31 Des PDFDocumento149 paginefs4q19 Erajaya Swasembada TBK Billingual 31 Des PDFIndahyuliaputriNessuna valutazione finora

- ACTBFAR Exercise Set #1 - Ex 5 - FS ClassificationsDocumento1 paginaACTBFAR Exercise Set #1 - Ex 5 - FS ClassificationsNikko Bowie PascualNessuna valutazione finora

- Tan v. Del RosarioDocumento5 pagineTan v. Del Rosarioalexis_beaNessuna valutazione finora

- Expenses:: Audit of Minor Operating DepartmentDocumento1 paginaExpenses:: Audit of Minor Operating DepartmentMedha SinghNessuna valutazione finora

- 07 Segment Reporting 1Documento4 pagine07 Segment Reporting 1Irtiza AbbasNessuna valutazione finora

- MI CH 10. Breakeven Analysis and Limiting Factor Analysis PDFDocumento5 pagineMI CH 10. Breakeven Analysis and Limiting Factor Analysis PDFPonkoj Sarker TutulNessuna valutazione finora

- Krispy Kreme DonutDocumento17 pagineKrispy Kreme DonuthannahkisNessuna valutazione finora

- WORKING CAPITAL DocxDocumento16 pagineWORKING CAPITAL DocxGab IgnacioNessuna valutazione finora

- Update Date: 15/03/2023 Unit: Million Dong: Balance Sheet - GTA 2018 2019 2020 2021Documento9 pagineUpdate Date: 15/03/2023 Unit: Million Dong: Balance Sheet - GTA 2018 2019 2020 2021The Meme ReaperNessuna valutazione finora

- Income TaxDocumento20 pagineIncome Taxjuliaysabellepepitoaguilar100% (1)

- 04 Long Term Construction Contracts PDFDocumento2 pagine04 Long Term Construction Contracts PDFKyla Valencia NgoNessuna valutazione finora

- Acc 124 - Week 13-14 - Ulob - Investment in Equity Securities - Assignment - CainDocumento2 pagineAcc 124 - Week 13-14 - Ulob - Investment in Equity Securities - Assignment - Cainslow dancerNessuna valutazione finora

- Kisi KisiDocumento14 pagineKisi KisiHairun NisaNessuna valutazione finora

- Topic: Comprehensive Final Case: Course Code: SemesterDocumento14 pagineTopic: Comprehensive Final Case: Course Code: SemesterPranto AhmedNessuna valutazione finora

- Taxation by Dastgir Mulla 2014Documento84 pagineTaxation by Dastgir Mulla 2014Tejasvini KhemajiNessuna valutazione finora

- Corporate Financial Accounting 13th Edition Warren Test Bank 1Documento106 pagineCorporate Financial Accounting 13th Edition Warren Test Bank 1john100% (38)

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 2Documento28 pagineSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 2jasperkennedy082% (22)

- Form5 PTDocumento2 pagineForm5 PTShilpa KapoorNessuna valutazione finora

- Chapter 13 - 8.9.2021Documento10 pagineChapter 13 - 8.9.2021Zi Yan HoonNessuna valutazione finora

- Analysis and Interpretation of Profitability: Operating ExpensesDocumento2 pagineAnalysis and Interpretation of Profitability: Operating ExpensesDavid Rolando García OpazoNessuna valutazione finora

- Researchpaper Measuring Financial Sustainability of Reliance Industries LimitedDocumento13 pagineResearchpaper Measuring Financial Sustainability of Reliance Industries Limitedcollege onnNessuna valutazione finora

- Solution Manual For Contemporary Financial Management 12th Edition by MoyerDocumento24 pagineSolution Manual For Contemporary Financial Management 12th Edition by MoyerMatthewGarciaqmen100% (48)

- Auditing Problems: Problem No. 1 - Audit of Property, Plant, and Equipment (Ppe)Documento19 pagineAuditing Problems: Problem No. 1 - Audit of Property, Plant, and Equipment (Ppe)Marco Louis Duval UyNessuna valutazione finora

- Relaxo Footwears Initiating Coverage 11062020Documento7 pagineRelaxo Footwears Initiating Coverage 11062020Vaishali AgrawalNessuna valutazione finora

- Mock Phinma Exam: Intermediate Accounting 3 Name: Date: Section: RatingDocumento14 pagineMock Phinma Exam: Intermediate Accounting 3 Name: Date: Section: RatingMichelle Ann Langbis VinoyaNessuna valutazione finora

- KALRAYDocumento2 pagineKALRAYMuhammad ImranNessuna valutazione finora