Potrebbero piacerti anche

- The Misterious Power of Xingyi QuanDocumento353 pagineThe Misterious Power of Xingyi Quannajwa latifah96% (27)

- 1928 Clymer RosicruciansDocumento48 pagine1928 Clymer RosicruciansTóthné Mónika100% (2)

- Japanese Folk SongsDocumento22 pagineJapanese Folk SongsAndre Lorenz Feria100% (1)

- Letter To Alexander Cain & Interested PersonsDocumento4 pagineLetter To Alexander Cain & Interested PersonsDavid ZarquiNessuna valutazione finora

- Oceans of Love Empowerment Carol Ann TessierDocumento8 pagineOceans of Love Empowerment Carol Ann Tessierkoochimetal100% (1)

- NWS 96th International Exhibition (2016)Documento44 pagineNWS 96th International Exhibition (2016)nationalwatercolorsocietyNessuna valutazione finora

- Nipuna Perera CIM 40040324Documento31 pagineNipuna Perera CIM 40040324Nipuna Perera100% (3)

- Midterm Exam...Documento4 pagineMidterm Exam...Lhine KiwalanNessuna valutazione finora

- Media EntertainmentDocumento352 pagineMedia EntertainmentArun Venkataramani100% (2)

- Capote - The Walls Are Cold PDFDocumento5 pagineCapote - The Walls Are Cold PDFJulian Mancipe AcuñaNessuna valutazione finora

- GovTech Maturity Index: The State of Public Sector Digital TransformationDa EverandGovTech Maturity Index: The State of Public Sector Digital TransformationNessuna valutazione finora

- Gayatri Mantra and Shaap VimochanaDocumento4 pagineGayatri Mantra and Shaap VimochanaSharmila JainNessuna valutazione finora

- Impact of Television Digitization On Viewer Satisfaction and Media Consumption in India Ijariie5922 PDFDocumento11 pagineImpact of Television Digitization On Viewer Satisfaction and Media Consumption in India Ijariie5922 PDFVJ SoniNessuna valutazione finora

- TELECOM ORGANIZATIONS ADAPT IN A POST-COVID-19 REALITYDa EverandTELECOM ORGANIZATIONS ADAPT IN A POST-COVID-19 REALITYNessuna valutazione finora

- Biography Review Angela MerkelDocumento2 pagineBiography Review Angela Merkelxaskar epNessuna valutazione finora

- Ppt. Marketing of Media ServicesDocumento96 paginePpt. Marketing of Media ServicesANJUM ASHRI100% (1)

- Vietnam in View 2018 Full ReportDocumento65 pagineVietnam in View 2018 Full Reporthanam78Nessuna valutazione finora

- Virgin Media Inc.: NeutralDocumento7 pagineVirgin Media Inc.: NeutralSumayyah ArslanNessuna valutazione finora

- EY-Ficci Media and Entertainment Report April22 - 2Documento3 pagineEY-Ficci Media and Entertainment Report April22 - 2Sargam SinghalNessuna valutazione finora

- EMIS Insights - Colombia ICT Sector Report 2020 - 2021Documento79 pagineEMIS Insights - Colombia ICT Sector Report 2020 - 2021mjkoNessuna valutazione finora

- Indian Cable and Satellite Industry - A Brief IntroductionDocumento12 pagineIndian Cable and Satellite Industry - A Brief IntroductionAshish DwivediNessuna valutazione finora

- Media Apr 07Documento11 pagineMedia Apr 07uttaramenonNessuna valutazione finora

- TASK 1 (A) Organization Summary: Customer BaseDocumento32 pagineTASK 1 (A) Organization Summary: Customer BaseNipuna PereraNessuna valutazione finora

- MohanDocumento31 pagineMohanJenylen Tajanlangit-CabisoNessuna valutazione finora

- TELEVISINDocumento5 pagineTELEVISINtanishka kNessuna valutazione finora

- Network 18 Investors Update 30062022Documento13 pagineNetwork 18 Investors Update 30062022Dhanush Kumar RamanNessuna valutazione finora

- Dish TV - Would It Break or Break EvenDocumento29 pagineDish TV - Would It Break or Break EvenKomal RanaNessuna valutazione finora

- Media and Entertainment IndustryDocumento70 pagineMedia and Entertainment Industryyugesh dubey100% (2)

- On Demand Quarterly - March 2008Documento16 pagineOn Demand Quarterly - March 2008kwlow100% (1)

- Org StudyDocumento53 pagineOrg StudyArjun Sanal100% (1)

- Initiating Coverage - Den Networks LTDDocumento19 pagineInitiating Coverage - Den Networks LTDVinit Bolinjkar100% (1)

- Media and Communication Services Industry in India. Report On CinepolisDocumento53 pagineMedia and Communication Services Industry in India. Report On CinepolisAtul GuptaNessuna valutazione finora

- GSMA Report AnnualDocumento2 pagineGSMA Report AnnualSyed Muhammad AfrazNessuna valutazione finora

- Ibok V1Documento11 pagineIbok V1abhi_mahnotNessuna valutazione finora

- VOD Quarterly Apr 2009Documento13 pagineVOD Quarterly Apr 2009mparesh100% (2)

- Over-The-Top Television (OTT)Documento17 pagineOver-The-Top Television (OTT)rammanohar22Nessuna valutazione finora

- AngelbrokingResearch Tejasnetwork IPONote 130617Documento12 pagineAngelbrokingResearch Tejasnetwork IPONote 130617durgasainathNessuna valutazione finora

- En DAY3 ABI Telcos As A Growth Accelerator enDocumento7 pagineEn DAY3 ABI Telcos As A Growth Accelerator endieuwrignNessuna valutazione finora

- Comcast Corporation: Case AnalysisDocumento15 pagineComcast Corporation: Case AnalysissaurabhNessuna valutazione finora

- Media and Entertainment IndustryDocumento70 pagineMedia and Entertainment IndustryAnkita RkNessuna valutazione finora

- Tuning in To Mobile TVDocumento6 pagineTuning in To Mobile TVkunal.nitwNessuna valutazione finora

- Media and EntertainmentDocumento5 pagineMedia and EntertainmentAhmed MastanNessuna valutazione finora

- Media and Entertainment January 2021Documento36 pagineMedia and Entertainment January 2021rakeshNessuna valutazione finora

- EMIS Insights - Brazil ICT Sector Report 2019 - 2023Documento91 pagineEMIS Insights - Brazil ICT Sector Report 2019 - 2023Rodrigo LisboaNessuna valutazione finora

- TiVo Q3 2017 Video Trends ReportDocumento39 pagineTiVo Q3 2017 Video Trends ReportKristina IrobalievaNessuna valutazione finora

- Ant Report Accounts 2009Documento54 pagineAnt Report Accounts 2009yochebaNessuna valutazione finora

- NW18 Investorsupdate 30092022Documento13 pagineNW18 Investorsupdate 30092022shishir5087Nessuna valutazione finora

- 10 Dr. Denny Setiawan Director Spectrum Planning KOMINFODocumento9 pagine10 Dr. Denny Setiawan Director Spectrum Planning KOMINFOindramaNessuna valutazione finora

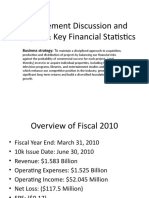

- Management Discussion and Analysis & Key Financial Statistics 33Documento14 pagineManagement Discussion and Analysis & Key Financial Statistics 33Jordan PinkusNessuna valutazione finora

- Media PDFDocumento37 pagineMedia PDFAyush AgrawalNessuna valutazione finora

- Network 18 Investor Update 30092019Documento11 pagineNetwork 18 Investor Update 30092019Pradeep YadavNessuna valutazione finora

- Shemaroo Entertainment Multibagger Stock PicDocumento19 pagineShemaroo Entertainment Multibagger Stock PicArunesh SinghNessuna valutazione finora

- 3Q 22 Corp PresDocumento18 pagine3Q 22 Corp PresArief KurniawanNessuna valutazione finora

- PT Telekomunikasi Indonesia, TBK: Fairly Steady 1Q20 ResultsDocumento9 paginePT Telekomunikasi Indonesia, TBK: Fairly Steady 1Q20 ResultsSugeng YuliantoNessuna valutazione finora

- Motion Pictures & Television & Music Industry: Reading SampleDocumento54 pagineMotion Pictures & Television & Music Industry: Reading SampleCah MakNessuna valutazione finora

- TelevisionDocumento44 pagineTelevisionajaylamaniyaplNessuna valutazione finora

- Indian Media & Entertainment Industry To TouchDocumento5 pagineIndian Media & Entertainment Industry To TouchCharu KrishnamurthyNessuna valutazione finora

- Ad Disappoints, Subscription Accelerates: Sun TV NetworkDocumento7 pagineAd Disappoints, Subscription Accelerates: Sun TV NetworkAshokNessuna valutazione finora

- IT Industry Factsheet-Mar 2009Documento5 pagineIT Industry Factsheet-Mar 2009Maruthi Krishna TuragaNessuna valutazione finora

- DishTV Investor PresentationDocumento32 pagineDishTV Investor Presentationmrinal_kakkar8215Nessuna valutazione finora

- Media IC in The Eye of The Storm 05oct2022 (1) - JM FinancialDocumento61 pagineMedia IC in The Eye of The Storm 05oct2022 (1) - JM FinancialPavanNessuna valutazione finora

- Brazil Telecom & Tech 2009 EconomistDocumento12 pagineBrazil Telecom & Tech 2009 EconomistimangoliniNessuna valutazione finora

- EY-Ficci Media and Entertainment Report April22Documento5 pagineEY-Ficci Media and Entertainment Report April22AADI SHANKARNessuna valutazione finora

- Motion Pictures & Television & Music Industry: COVID-19 ImpactDocumento51 pagineMotion Pictures & Television & Music Industry: COVID-19 ImpactPrabha GuptaNessuna valutazione finora

- DMX Technologies Annual Report 2008Documento116 pagineDMX Technologies Annual Report 2008WeR1 Consultants Pte LtdNessuna valutazione finora

- Set Top BoxDocumento9 pagineSet Top BoxVaibhav MisraNessuna valutazione finora

- MKT 465slidesDocumento21 pagineMKT 465slidesredwan999Nessuna valutazione finora

- PWC India em Outlook 2011 081211Documento152 paginePWC India em Outlook 2011 081211Chetan SagarNessuna valutazione finora

- Radio Network Revenues World Summary: Market Values & Financials by CountryDa EverandRadio Network Revenues World Summary: Market Values & Financials by CountryNessuna valutazione finora

- Wireless Telecommunications Carrier Revenues World Summary: Market Values & Financials by CountryDa EverandWireless Telecommunications Carrier Revenues World Summary: Market Values & Financials by CountryNessuna valutazione finora

- Soal Jawab Pondasi Tiang Pancang RegDocumento7 pagineSoal Jawab Pondasi Tiang Pancang RegLarno BeNessuna valutazione finora

- GROUP 5 PE & Health PDFDocumento72 pagineGROUP 5 PE & Health PDFallysa canaleNessuna valutazione finora

- Kaori's LetterDocumento3 pagineKaori's LetterOriza Praba AlbaniNessuna valutazione finora

- Daftar SitusDocumento3 pagineDaftar SitusSaleho BikanNessuna valutazione finora

- Second Conditional Fun Activities Games Grammar Guides Oneonone Activ - 125322Documento9 pagineSecond Conditional Fun Activities Games Grammar Guides Oneonone Activ - 125322Mark-Shelly BalolongNessuna valutazione finora

- "Philosophy Has Become Worldly": Marx On Ruthless Critique: Judith ButlerDocumento9 pagine"Philosophy Has Become Worldly": Marx On Ruthless Critique: Judith ButlerJoão josé carlosNessuna valutazione finora

- Goldmund The Malady of Elegance ReviewDocumento3 pagineGoldmund The Malady of Elegance ReviewMarquelNessuna valutazione finora

- JPRCP Manual FullDocumento243 pagineJPRCP Manual FullHanuman BuildersNessuna valutazione finora

- TH THDocumento6 pagineTH THSamiksha JainNessuna valutazione finora

- Apple FruitingDocumento37 pagineApple FruitingzhorvatovicNessuna valutazione finora

- Twang NNS 101Documento10 pagineTwang NNS 101ntv2000100% (1)

- J.cocker Discography.1969 2013.MP3.320 TracklistDocumento14 pagineJ.cocker Discography.1969 2013.MP3.320 TracklistMarius Stefan BerindeNessuna valutazione finora

- Super Dungeon Explore Arena PDFDocumento3 pagineSuper Dungeon Explore Arena PDFlars gunnarNessuna valutazione finora

- 2019 TMT Residential BrochureDocumento5 pagine2019 TMT Residential BrochureGabby CardosoNessuna valutazione finora

- Prepositions Worksheet Reading Level 02Documento4 paginePrepositions Worksheet Reading Level 02FiorE' BellE'Nessuna valutazione finora

- XV-DV323 XV-DV424 S-DV323 S-DV424: DVD/CD ReceiverDocumento74 pagineXV-DV323 XV-DV424 S-DV323 S-DV424: DVD/CD Receiverkosty.eu85Nessuna valutazione finora

- Amelia Spokes Warwick Primary School Wellingborough NorthamptonshireDocumento4 pagineAmelia Spokes Warwick Primary School Wellingborough NorthamptonshireDiamonds Study CentreNessuna valutazione finora

- Lesson Plan in Contemporary ArtsDocumento2 pagineLesson Plan in Contemporary ArtsCristine Joy Caminoc-HechanovaNessuna valutazione finora

- Atelier Annie: Alchemists of Sera Island - Guide and WalkthroughDocumento45 pagineAtelier Annie: Alchemists of Sera Island - Guide and WalkthroughMateiMaria-MihaelaNessuna valutazione finora

- Bluestone Alley LTR NoteDocumento2 pagineBluestone Alley LTR NoteArvin John Masuela88% (8)