Potrebbero piacerti anche

- The Valuation and Financing of Lady M Case StudyDocumento4 pagineThe Valuation and Financing of Lady M Case StudyUry Suryanti Rahayu100% (3)

- The Valuation and Financing of Lady M Case StudyDocumento4 pagineThe Valuation and Financing of Lady M Case StudyUry Suryanti RahayuNessuna valutazione finora

- Lupin's Foray Into Japan - SolutionDocumento14 pagineLupin's Foray Into Japan - Solutionvardhan100% (1)

- Wonder Study GuideDocumento52 pagineWonder Study GuideJoseph Lin67% (3)

- Boston Beer ExcelDocumento6 pagineBoston Beer ExcelNarinderNessuna valutazione finora

- HanssonDocumento11 pagineHanssonJust Some EditsNessuna valutazione finora

- AFDMDocumento6 pagineAFDMAhsan IqbalNessuna valutazione finora

- Sui Southern Gas Company Limited: Analysis of Financial Statements Financial Year 2004 - 2001 Q Financial Year 2010Documento17 pagineSui Southern Gas Company Limited: Analysis of Financial Statements Financial Year 2004 - 2001 Q Financial Year 2010mumairmalikNessuna valutazione finora

- Hindustan Petrolium Corporation LTD: ProsDocumento9 pagineHindustan Petrolium Corporation LTD: ProsChandan KokaneNessuna valutazione finora

- DCF Valuation Pre Merger Southern Union CompanyDocumento20 pagineDCF Valuation Pre Merger Southern Union CompanyIvan AlimirzoevNessuna valutazione finora

- FM 2 AssignmentDocumento337 pagineFM 2 AssignmentAvradeep DasNessuna valutazione finora

- Automobile Sales: Assets and Working CapitalDocumento16 pagineAutomobile Sales: Assets and Working CapitalKshitishNessuna valutazione finora

- Britannia IndustriesDocumento12 pagineBritannia Industriesmundadaharsh1Nessuna valutazione finora

- Ghazi Fabrics: Ratio Analysis of Last Five YearsDocumento6 pagineGhazi Fabrics: Ratio Analysis of Last Five YearsASIF RAFIQUE BHATTINessuna valutazione finora

- MSFTDocumento83 pagineMSFTJohn wickNessuna valutazione finora

- Caso TeuerDocumento46 pagineCaso Teuerjoaquin bullNessuna valutazione finora

- Primo BenzinaDocumento30 paginePrimo BenzinaSofía MargaritaNessuna valutazione finora

- Radico KhaitanDocumento38 pagineRadico Khaitantapasya khanijouNessuna valutazione finora

- 2006 2007 2008 Sales Net Sales Less CogsDocumento17 pagine2006 2007 2008 Sales Net Sales Less CogsMohammed ArifNessuna valutazione finora

- Book1 2Documento10 pagineBook1 2Aakash SinghalNessuna valutazione finora

- Horizontal Vertical AnalysisDocumento4 pagineHorizontal Vertical AnalysisAhmedNessuna valutazione finora

- Fin 448 Final PracticeDocumento2 pagineFin 448 Final PracticeMay ChenNessuna valutazione finora

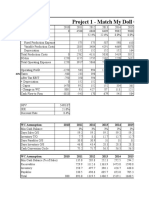

- Project 1 - Match My Doll Clothing Line: WC Assumption: 2010 2011 2012 2013 2014 2015Documento4 pagineProject 1 - Match My Doll Clothing Line: WC Assumption: 2010 2011 2012 2013 2014 2015rohitNessuna valutazione finora

- Allahabad Bank Sep 09Documento5 pagineAllahabad Bank Sep 09chetandusejaNessuna valutazione finora

- JSW SteelDocumento34 pagineJSW SteelShashank PatelNessuna valutazione finora

- Exhibit 1: Income Taxes 227.6 319.3 465.0 49.9Documento11 pagineExhibit 1: Income Taxes 227.6 319.3 465.0 49.9rendy mangunsongNessuna valutazione finora

- Projected 2013 2014 2015 2016 2017Documento11 pagineProjected 2013 2014 2015 2016 2017Aijaz AslamNessuna valutazione finora

- Nike Case Study VrindaDocumento4 pagineNike Case Study VrindaAnchal ChokhaniNessuna valutazione finora

- Tech MahindraDocumento17 pagineTech Mahindrapiyushpatil749Nessuna valutazione finora

- Altagas Green Exhibits With All InfoDocumento4 pagineAltagas Green Exhibits With All InfoArjun NairNessuna valutazione finora

- DCF TVSDocumento17 pagineDCF TVSSunilNessuna valutazione finora

- AttachmentDocumento19 pagineAttachmentSanjay MulviNessuna valutazione finora

- The Valuation and Financing of Lady M Confections: 23600 Cash BEP 1888000,00Documento4 pagineThe Valuation and Financing of Lady M Confections: 23600 Cash BEP 1888000,00Rahul VenugopalanNessuna valutazione finora

- Safari 3Documento4 pagineSafari 3Bharti SutharNessuna valutazione finora

- Lady M SolutionDocumento4 pagineLady M SolutionRahul VenugopalanNessuna valutazione finora

- Add Dep Less Tax OCF Change in Capex Change in NWC FCFDocumento5 pagineAdd Dep Less Tax OCF Change in Capex Change in NWC FCFGullible KhanNessuna valutazione finora

- Flow Valuation, Case #KEL778Documento20 pagineFlow Valuation, Case #KEL778SreeHarshaKazaNessuna valutazione finora

- AmcDocumento19 pagineAmcTimothy RenardusNessuna valutazione finora

- Discounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No FormulasDocumento2 pagineDiscounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No Formulasrito2005Nessuna valutazione finora

- Case 8-Group 16Documento14 pagineCase 8-Group 16reza041Nessuna valutazione finora

- Tiffany & Co's Analysis: Student Name Institutional Affiliation Course Name Instructor Name DateDocumento6 pagineTiffany & Co's Analysis: Student Name Institutional Affiliation Course Name Instructor Name DateOmer KhanNessuna valutazione finora

- PasfDocumento14 paginePasfAbhishek BhatnagarNessuna valutazione finora

- Book 1Documento2 pagineBook 1justingordanNessuna valutazione finora

- Common Size Income Statement - TATA MOTORS LTDDocumento6 pagineCommon Size Income Statement - TATA MOTORS LTDSubrat BiswalNessuna valutazione finora

- Valuation GroupNo.12Documento4 pagineValuation GroupNo.12John DummiNessuna valutazione finora

- Bharat Hotels Valuation Case StudyDocumento3 pagineBharat Hotels Valuation Case StudyRohitNessuna valutazione finora

- Sangam and Excel Mini Case Solution TemplateDocumento3 pagineSangam and Excel Mini Case Solution TemplateSHUBHAM DIXITNessuna valutazione finora

- Private Sector Banks Comparative Analysis 1HFY22Documento12 paginePrivate Sector Banks Comparative Analysis 1HFY22Tushar Mohan0% (1)

- Rosetta Stone IPODocumento5 pagineRosetta Stone IPOFatima Ansari d/o Muhammad AshrafNessuna valutazione finora

- Projections & ValuationDocumento109 pagineProjections & ValuationPulokesh GhoshNessuna valutazione finora

- Financial Model of Dmart - 5Documento4 pagineFinancial Model of Dmart - 5Shivam DubeyNessuna valutazione finora

- Supreme Annual Report 15 16Documento104 pagineSupreme Annual Report 15 16adoniscalNessuna valutazione finora

- SuganyaDocumento3 pagineSuganyaSenthil KumarNessuna valutazione finora

- Pinkerton (B)Documento3 paginePinkerton (B)Anupam Chaplot100% (1)

- Fin 421 AssignmentDocumento6 pagineFin 421 AssignmentKassaf ChowdhuryNessuna valutazione finora

- Finance 2Documento208 pagineFinance 2B SNessuna valutazione finora

- Dec 2021 enDocumento21 pagineDec 2021 enMohammed ShbairNessuna valutazione finora

- AirThread SecBC Group9Documento4 pagineAirThread SecBC Group9Vishal BhanushaliNessuna valutazione finora

- Maruti Suzuki Balance SheetDocumento6 pagineMaruti Suzuki Balance SheetMasoud AfzaliNessuna valutazione finora

- Mercury Athletic Footwear Case (Work Sheet)Documento16 pagineMercury Athletic Footwear Case (Work Sheet)Bharat KoiralaNessuna valutazione finora

- United States Census Figures Back to 1630Da EverandUnited States Census Figures Back to 1630Nessuna valutazione finora

- Netra Early Warnings Signals Through Charts - May 2022Documento16 pagineNetra Early Warnings Signals Through Charts - May 2022Adhiraj MukherjeeNessuna valutazione finora

- FA-Depreciation - Inventory SolvedDocumento13 pagineFA-Depreciation - Inventory SolvedAdhiraj MukherjeeNessuna valutazione finora

- Fiction of Motivated Soyl UbDocumento2 pagineFiction of Motivated Soyl UbAdhiraj MukherjeeNessuna valutazione finora

- Task 2Documento1 paginaTask 2Adhiraj MukherjeeNessuna valutazione finora

- FA-Depreciation - Inventory SolvedDocumento13 pagineFA-Depreciation - Inventory SolvedAdhiraj MukherjeeNessuna valutazione finora

- Operations Research: Case Let 1: Production PlanningDocumento1 paginaOperations Research: Case Let 1: Production PlanningAdhiraj MukherjeeNessuna valutazione finora

- Renault's Ride Into India: Discussion QuestionsDocumento1 paginaRenault's Ride Into India: Discussion QuestionsAdhiraj MukherjeeNessuna valutazione finora

- Inference:: Lower Slightly Lower LowerDocumento14 pagineInference:: Lower Slightly Lower LowerAdhiraj MukherjeeNessuna valutazione finora

- Suzlon Case 15juneDocumento2 pagineSuzlon Case 15juneAdhiraj MukherjeeNessuna valutazione finora

- Inference:: Lower Slightly Lower LowerDocumento14 pagineInference:: Lower Slightly Lower LowerAdhiraj MukherjeeNessuna valutazione finora

- TIB Class Exercise: Consumer Connected Wearable Smart DevicesDocumento1 paginaTIB Class Exercise: Consumer Connected Wearable Smart DevicesAdhiraj MukherjeeNessuna valutazione finora

- Introduction To Financial System: 5.a Commercial BankDocumento6 pagineIntroduction To Financial System: 5.a Commercial BankAdhiraj MukherjeeNessuna valutazione finora

- Suzlon Case 15juneDocumento2 pagineSuzlon Case 15juneAdhiraj MukherjeeNessuna valutazione finora

- Operations Research: Case Let 1: Production PlanningDocumento1 paginaOperations Research: Case Let 1: Production PlanningAdhiraj MukherjeeNessuna valutazione finora

- Trade, Commerce and PetroliumDocumento4 pagineTrade, Commerce and PetroliumAdhiraj MukherjeeNessuna valutazione finora

- Legal History Project .....Documento16 pagineLegal History Project .....sayed abdul jamayNessuna valutazione finora

- Ity of OS Ngeles: GENERAL APPROVAL - Initial Approval - Concrete and Masonry Strengthening Using TheDocumento3 pagineIty of OS Ngeles: GENERAL APPROVAL - Initial Approval - Concrete and Masonry Strengthening Using TheAntonio CastilloNessuna valutazione finora

- Tips and TricksDocumento1 paginaTips and TricksTOPdeskNessuna valutazione finora

- Puyo vs. Judge Go (2018)Documento2 paginePuyo vs. Judge Go (2018)Mara VinluanNessuna valutazione finora

- 090 People V RealDocumento3 pagine090 People V RealTeodoro Jose BrunoNessuna valutazione finora

- CSC Personal Data SheetDocumento10 pagineCSC Personal Data SheetMaria LeeNessuna valutazione finora

- Halden Galway Int'L Corp.: GWP Packaging Malaysia SDN BHDDocumento13 pagineHalden Galway Int'L Corp.: GWP Packaging Malaysia SDN BHDCharles YapNessuna valutazione finora

- Stat Con Notes 1 (GujildeDocumento3 pagineStat Con Notes 1 (GujildeDave UrotNessuna valutazione finora

- RR No 21-2018 PDFDocumento3 pagineRR No 21-2018 PDFJames Salviejo PinedaNessuna valutazione finora

- USNORTHCOM FaithfulPatriotDocumento33 pagineUSNORTHCOM FaithfulPatriotnelson duringNessuna valutazione finora

- CV Business Adm Mgr-S.DridiDocumento2 pagineCV Business Adm Mgr-S.DridiMoaatazz NouisriNessuna valutazione finora

- Cada IntmgtAcctg3Exer1Documento7 pagineCada IntmgtAcctg3Exer1KrishNessuna valutazione finora

- AY Program For June 18th 2016Documento6 pagineAY Program For June 18th 2016Darnelle Allister-CelestineNessuna valutazione finora

- Module 6 - Technology in The Delivery of Healthcare and Ceps On Ethico-Moral Practice in NursingDocumento10 pagineModule 6 - Technology in The Delivery of Healthcare and Ceps On Ethico-Moral Practice in NursingKatie HolmesNessuna valutazione finora

- Conference Steel Joist InstituteDocumento3 pagineConference Steel Joist Instituteinsane88Nessuna valutazione finora

- Medical Ethics PaperDocumento4 pagineMedical Ethics PaperinnyNessuna valutazione finora

- Bharat Sookshma Udyam SurakshaDocumento12 pagineBharat Sookshma Udyam SurakshaPrakhar ShuklaNessuna valutazione finora

- Deadweight Loss and Price DiscriminationDocumento21 pagineDeadweight Loss and Price Discrimination0241ASHAYNessuna valutazione finora

- PlaceDocumento4 paginePlaceMark EvansNessuna valutazione finora

- Accountancy Topic:-Depreciation. SlidesDocumento83 pagineAccountancy Topic:-Depreciation. SlidesAkash SahNessuna valutazione finora

- The Meaning of Independence DayDocumento285 pagineThe Meaning of Independence DayCheryl MillerNessuna valutazione finora

- DAT Business EthicsDocumento6 pagineDAT Business EthicsMary Erat Dumaluan GulangNessuna valutazione finora

- Allen v. United States, 157 U.S. 675 (1895)Documento5 pagineAllen v. United States, 157 U.S. 675 (1895)Scribd Government DocsNessuna valutazione finora

- Alan Scott - New Critical Writings in Political Sociology Volume Three - Globalization and Contemporary Challenges To The Nation-State (2009, Ashgate - Routledge) PDFDocumento469 pagineAlan Scott - New Critical Writings in Political Sociology Volume Three - Globalization and Contemporary Challenges To The Nation-State (2009, Ashgate - Routledge) PDFkaranNessuna valutazione finora

- Federal Register / Vol. 70, No. 199 / Monday, October 17, 2005 / NoticesDocumento2 pagineFederal Register / Vol. 70, No. 199 / Monday, October 17, 2005 / NoticesJustia.comNessuna valutazione finora

- Anmol Kushwah (9669369115) : To Be Filled by InterviewerDocumento6 pagineAnmol Kushwah (9669369115) : To Be Filled by InterviewermbaNessuna valutazione finora

- Driver CPC - Periodic Training LeafletDocumento8 pagineDriver CPC - Periodic Training Leafletkokuroku100% (1)

- Vimal KumarDocumento2 pagineVimal KumarAkash ParnamiNessuna valutazione finora

- Citric Acid SDS11350 PDFDocumento7 pagineCitric Acid SDS11350 PDFSyafiq Mohd NohNessuna valutazione finora