Potrebbero piacerti anche

- Before Analysing Whether To Go For 1Documento2 pagineBefore Analysing Whether To Go For 1Shivani KarkeraNessuna valutazione finora

- We Analyze Disruption Was Analyzed To Identify Ways in Which It Could Be ImprovedDocumento2 pagineWe Analyze Disruption Was Analyzed To Identify Ways in Which It Could Be ImprovedShivani KarkeraNessuna valutazione finora

- DOE Solar Foundation PDFDocumento13 pagineDOE Solar Foundation PDFShivani KarkeraNessuna valutazione finora

- The Ceiling On Project Capacity and Contracted Load RemovedDocumento1 paginaThe Ceiling On Project Capacity and Contracted Load RemovedShivani KarkeraNessuna valutazione finora

- BENEFITS and ChallengesDocumento2 pagineBENEFITS and ChallengesShivani KarkeraNessuna valutazione finora

- TPT 2 PipelineDocumento21 pagineTPT 2 PipelineShivani KarkeraNessuna valutazione finora

- Ship Name: Date: SPEED (MPH) Rotation DISTANCE/miles: Cargo DiscriptionDocumento1 paginaShip Name: Date: SPEED (MPH) Rotation DISTANCE/miles: Cargo DiscriptionShivani KarkeraNessuna valutazione finora

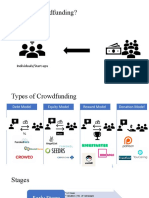

- What Is Crowdfunding?: Individuals/Start-ups FundingDocumento3 pagineWhat Is Crowdfunding?: Individuals/Start-ups FundingShivani KarkeraNessuna valutazione finora

- 2019 AnalysisDocumento3 pagine2019 AnalysisShivani KarkeraNessuna valutazione finora

- Amplus Off Site ModelDocumento4 pagineAmplus Off Site ModelShivani KarkeraNessuna valutazione finora

- Basic Intermodal OperationDocumento3 pagineBasic Intermodal OperationShivani KarkeraNessuna valutazione finora

- Sample Notification Letters SchoolDocumento3 pagineSample Notification Letters SchoolShivani KarkeraNessuna valutazione finora

- 2009 12 JRC White Certificates PDFDocumento62 pagine2009 12 JRC White Certificates PDFShivani KarkeraNessuna valutazione finora

- Travelers Insurance: Focusing On Climate Change and Natural Disaster RiskDocumento1 paginaTravelers Insurance: Focusing On Climate Change and Natural Disaster RiskShivani KarkeraNessuna valutazione finora

- Case Facts and AnalysisDocumento2 pagineCase Facts and AnalysisShivani KarkeraNessuna valutazione finora

- Pros and ConsDocumento4 paginePros and ConsShivani KarkeraNessuna valutazione finora

- SITUATION ANALYSIS Morgan StanleyDocumento1 paginaSITUATION ANALYSIS Morgan StanleyShivani KarkeraNessuna valutazione finora

- BENEFITS and ChallengesDocumento2 pagineBENEFITS and ChallengesShivani KarkeraNessuna valutazione finora

- Caprica Energy and Its ChoicesDocumento1 paginaCaprica Energy and Its ChoicesShivani KarkeraNessuna valutazione finora

- AC2ID Test: Identities Misaligned: Actual and CommunicatedDocumento4 pagineAC2ID Test: Identities Misaligned: Actual and CommunicatedShivani KarkeraNessuna valutazione finora

- 2019 AnalysisDocumento3 pagine2019 AnalysisShivani KarkeraNessuna valutazione finora

- Instruments For Financing Carbon Savings For Large ProgrammesDocumento20 pagineInstruments For Financing Carbon Savings For Large ProgrammesShivani KarkeraNessuna valutazione finora

- Template Positive Case With Exposure in Schools - 07202020Documento2 pagineTemplate Positive Case With Exposure in Schools - 07202020Shivani KarkeraNessuna valutazione finora

- EU Case StudyDocumento1 paginaEU Case StudyShivani KarkeraNessuna valutazione finora

- Real World Examples of Successful Crowdfunding Ventures: Social MediaDocumento2 pagineReal World Examples of Successful Crowdfunding Ventures: Social MediaShivani KarkeraNessuna valutazione finora

- Venture Capital Method: Investment ScenariosDocumento2 pagineVenture Capital Method: Investment ScenariosShivani KarkeraNessuna valutazione finora

- Energy Management 20-21Documento11 pagineEnergy Management 20-21Shivani KarkeraNessuna valutazione finora

- Venture Capital Method With Dilution.Documento6 pagineVenture Capital Method With Dilution.Shivani KarkeraNessuna valutazione finora

- Venture Capital Method.Documento2 pagineVenture Capital Method.Shivani KarkeraNessuna valutazione finora

- Venture Capital Method With Multiple Rounds.Documento4 pagineVenture Capital Method With Multiple Rounds.Shivani KarkeraNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (120)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Indo-Pak Foreign RelDocumento2 pagineIndo-Pak Foreign RelMuhammad EhtishamNessuna valutazione finora

- History GR 10 ADDENDUMDocumento9 pagineHistory GR 10 ADDENDUMNoma ButheleziNessuna valutazione finora

- Sufis and Sufism in India X-RayedDocumento8 pagineSufis and Sufism in India X-RayeddudhaiNessuna valutazione finora

- Prospective Member LetterDocumento1 paginaProspective Member LetterClinton ChanNessuna valutazione finora

- CH 21 Sec 1 - Spain's Empire and European AbsolutismDocumento7 pagineCH 21 Sec 1 - Spain's Empire and European AbsolutismMrEHsiehNessuna valutazione finora

- LibisDocumento39 pagineLibisAngelika CalingasanNessuna valutazione finora

- Application For Social Security Card - Ss-5Documento1 paginaApplication For Social Security Card - Ss-5Casey Orvis100% (1)

- Ips Gradation List With Medal 18.07.2018Documento47 pagineIps Gradation List With Medal 18.07.2018Sachin Shrivastava100% (1)

- Macklin Scheldrup: Lilliputian Choice: Explaining Small State Foreign Policy VariationsDocumento59 pagineMacklin Scheldrup: Lilliputian Choice: Explaining Small State Foreign Policy VariationsTamásKelemenNessuna valutazione finora

- Module 4Documento7 pagineModule 4LA Marie0% (1)

- Consortium of National Law Universities: Provisional 3rd List - CLAT 2019 - UGDocumento3 pagineConsortium of National Law Universities: Provisional 3rd List - CLAT 2019 - UGRAJA RASTOGINessuna valutazione finora

- Ellen Meiksins Wood - Locke Against Democracy Consent Representation and Suffrage in Two TreatisesDocumento33 pagineEllen Meiksins Wood - Locke Against Democracy Consent Representation and Suffrage in Two TreatisesKresimirZovakNessuna valutazione finora

- The Concerns of Composition - Zoe MihaliczDocumento6 pagineThe Concerns of Composition - Zoe MihaliczZoe MihaliczNessuna valutazione finora

- C Overt Action The Disappearing CDocumento13 pagineC Overt Action The Disappearing CSerkan KarakayaNessuna valutazione finora

- Article 15 of The Constitution Contents FinalDocumento15 pagineArticle 15 of The Constitution Contents FinalRAUNAK SHUKLANessuna valutazione finora

- 227 - Luna vs. IACDocumento3 pagine227 - Luna vs. IACNec Salise ZabatNessuna valutazione finora

- 201438769Documento68 pagine201438769The Myanmar TimesNessuna valutazione finora

- Thuy Hoang Thi ThuDocumento8 pagineThuy Hoang Thi Thukanehai09Nessuna valutazione finora

- Republic Vs Tipay Spec ProDocumento2 pagineRepublic Vs Tipay Spec ProLemuel Angelo M. Eleccion0% (2)

- 1947 Constitution of Burma English VersionDocumento76 pagine1947 Constitution of Burma English Versionminthukha100% (1)

- Dayao v. ComelecDocumento15 pagineDayao v. ComelecRichelle CartinNessuna valutazione finora

- Claus Offe - Capitalism by Democratic DesignDocumento29 pagineClaus Offe - Capitalism by Democratic DesignGuilherme Simões ReisNessuna valutazione finora

- Kipling Vs ConradDocumento2 pagineKipling Vs Conradapi-258322426100% (1)

- Internal Revenue Allotment-ALBERTDocumento14 pagineInternal Revenue Allotment-ALBERTJoy Dales100% (1)

- C.F. Sharp Crew Management, Inc.: Shipboard Application FormDocumento1 paginaC.F. Sharp Crew Management, Inc.: Shipboard Application FormRuviNessuna valutazione finora

- Locating and Defining The CaribbeanDocumento29 pagineLocating and Defining The CaribbeanRoberto Saladeen100% (2)

- TORRES Vs LEE COUNTY PDFDocumento17 pagineTORRES Vs LEE COUNTY PDFDevetta BlountNessuna valutazione finora

- J Logan-Saunders - Proposal Final Topic ChangeDocumento3 pagineJ Logan-Saunders - Proposal Final Topic Changeapi-315614961Nessuna valutazione finora

- 2nd Form Study GuideDocumento3 pagine2nd Form Study GuideVirgilio CusNessuna valutazione finora

- Form "D-1" Annual Return (See 2020-2021 General Information: Regulation 2.1.13)Documento2 pagineForm "D-1" Annual Return (See 2020-2021 General Information: Regulation 2.1.13)Shiv KumarNessuna valutazione finora