Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Strategic AlliancesDocumento15 pagineStrategic AlliancesAli AhmadNessuna valutazione finora

- 2016 Equipment Book PDFDocumento90 pagine2016 Equipment Book PDFJulie MyersNessuna valutazione finora

- Financial Accounting: A: How To Study AccountingDocumento29 pagineFinancial Accounting: A: How To Study Accountingrishi_positive1195Nessuna valutazione finora

- PSBA A.R. Handout SolvedDocumento13 paginePSBA A.R. Handout SolvedMikka100% (2)

- Skin Care - Malaysia Insights - August 2016Documento37 pagineSkin Care - Malaysia Insights - August 2016Yeong YeeNessuna valutazione finora

- (Paper Size 8.11x13) Economic Survey FormDocumento3 pagine(Paper Size 8.11x13) Economic Survey FormKevin Jove Yague100% (1)

- Asteri Capital (Glencore)Documento4 pagineAsteri Capital (Glencore)Brett Reginald ScottNessuna valutazione finora

- Ambassador CarDocumento16 pagineAmbassador CarPawan Swarnkar0% (1)

- Global Medical Systems #27, Model House II Street, Basavanagudi, Bengaluru - 560004 2661 7623, 2661 1679 9 4404979Documento2 pagineGlobal Medical Systems #27, Model House II Street, Basavanagudi, Bengaluru - 560004 2661 7623, 2661 1679 9 4404979Archesh DeepNessuna valutazione finora

- Case Study: High-Tech Startup's Struggles in TanzaniaDocumento5 pagineCase Study: High-Tech Startup's Struggles in TanzaniaMarshaPatterson0% (1)

- Monopolistic CompetitionDocumento2 pagineMonopolistic Competitionraisafkmui2010Nessuna valutazione finora

- Creation of AgencyDocumento3 pagineCreation of AgencyMeenal Pachory Pandey100% (1)

- Orden de Venta - 372 - 20181123 - 123904Documento2 pagineOrden de Venta - 372 - 20181123 - 123904l2oNnYNessuna valutazione finora

- CV Bernard Manurung UpdateDocumento4 pagineCV Bernard Manurung UpdateBernard Agus Lala ManurungNessuna valutazione finora

- The Europe Business Assembly Is Proud To Announce That ADITI IT SERVICES PVT. LTD. Has Received The Prestigious Best Enterprises AwardDocumento3 pagineThe Europe Business Assembly Is Proud To Announce That ADITI IT SERVICES PVT. LTD. Has Received The Prestigious Best Enterprises AwardMary Joy Dela MasaNessuna valutazione finora

- Produk BatalDocumento30 pagineProduk BatalNurul AtikNessuna valutazione finora

- Introduction To Venture Capital 5thDocumento37 pagineIntroduction To Venture Capital 5thSaili Sarmalkar100% (1)

- Ostriches, Wilful Blindness, and AML/CFTDocumento3 pagineOstriches, Wilful Blindness, and AML/CFTAlan PedleyNessuna valutazione finora

- Jack Ma: Ma Yun (Chinese: Born 10 September 1964), Known Professionally As Jack Ma, Is A ChineseDocumento3 pagineJack Ma: Ma Yun (Chinese: Born 10 September 1964), Known Professionally As Jack Ma, Is A ChineseAnnalyn MantillaNessuna valutazione finora

- Revised Policies on Granting Loyalty AwardsDocumento2 pagineRevised Policies on Granting Loyalty Awardskhaye_cee1150% (2)

- Af ManifestDocumento23 pagineAf ManifestCwasi Musicman100% (1)

- Tai Tong Chuache & Co. v. Insurance CommissionDocumento1 paginaTai Tong Chuache & Co. v. Insurance CommissionmastaacaNessuna valutazione finora

- Rulings2000 DigestDocumento21 pagineRulings2000 DigestArriane MartinezNessuna valutazione finora

- J Mike Football Camp Round 2 Donations - Sheet1Documento2 pagineJ Mike Football Camp Round 2 Donations - Sheet1api-322701803Nessuna valutazione finora

- Single Version Modeler Cash Flow AnalysisDocumento2 pagineSingle Version Modeler Cash Flow AnalysiskkayathwalNessuna valutazione finora

- Pepsico Brand Image Questionnaire ResearchDocumento3 paginePepsico Brand Image Questionnaire ResearchVipul Kanojia100% (1)

- Nestle USA Grainger purchases and paymentsDocumento81 pagineNestle USA Grainger purchases and paymentsnelsonNessuna valutazione finora

- Scholarship EssayDocumento2 pagineScholarship EssayRacheal ChinnNessuna valutazione finora

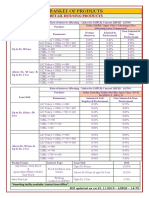

- BASKET OF RETAIL PRODUCTS RATESDocumento3 pagineBASKET OF RETAIL PRODUCTS RATESVirendra K VermaNessuna valutazione finora

- FINAL Mol 2 25 10 Opp Mot Viol StayDocumento65 pagineFINAL Mol 2 25 10 Opp Mot Viol StaysturdonNessuna valutazione finora