Potrebbero piacerti anche

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- FiguresDocumento1 paginaFigurescrisnaNessuna valutazione finora

- Eng PDFDocumento56 pagineEng PDFcrisnaNessuna valutazione finora

- CFDEx1 NotesDocumento25 pagineCFDEx1 NotescrisnaNessuna valutazione finora

- Linear Optimization - A ManufacturerDocumento62 pagineLinear Optimization - A ManufacturercrisnaNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- OPC UA Part 1 - Overview and Concepts 1.03 SpecificationDocumento27 pagineOPC UA Part 1 - Overview and Concepts 1.03 SpecificationKanenas KanenasNessuna valutazione finora

- Christian Kernozek ResumeDocumento2 pagineChristian Kernozek Resumeapi-279432673Nessuna valutazione finora

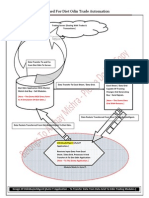

- Documentation - Diet Odin Demo ApplicationDocumento4 pagineDocumentation - Diet Odin Demo Applicationashucool23Nessuna valutazione finora

- Dorks-12 10 19-04 46 17Documento36 pagineDorks-12 10 19-04 46 17Jhon Mario CastroNessuna valutazione finora

- A Review On Plant Recognition and Classification Techniques Using Leaf ImagesDocumento6 pagineA Review On Plant Recognition and Classification Techniques Using Leaf ImagesseventhsensegroupNessuna valutazione finora

- March 2018 Fundamental IT Engineer Examination (Afternoon)Documento34 pagineMarch 2018 Fundamental IT Engineer Examination (Afternoon)Denz TajoNessuna valutazione finora

- IBM Rational Quality Manager 000-823 Practice Exam QuestionsDocumento20 pagineIBM Rational Quality Manager 000-823 Practice Exam QuestionsCahya PerdanaNessuna valutazione finora

- GROUP 3 Image CompressionDocumento31 pagineGROUP 3 Image CompressionPrayerNessuna valutazione finora

- Generic EULA template optimized for SEODocumento2 pagineGeneric EULA template optimized for SEONonoyLaurelFernandezNessuna valutazione finora

- AIF20 Master GuideDocumento52 pagineAIF20 Master GuideAntonio Di BellaNessuna valutazione finora

- MSIM 602 Simulation Fundamentals AssignmentDocumento2 pagineMSIM 602 Simulation Fundamentals Assignmentahaque08Nessuna valutazione finora

- Algebra 2 HN 1Documento9 pagineAlgebra 2 HN 1euclidpbNessuna valutazione finora

- PBS CCMD CVMD Administrator GuideDocumento40 paginePBS CCMD CVMD Administrator GuidesharadcsinghNessuna valutazione finora

- Digital Rights ManagementDocumento11 pagineDigital Rights ManagementVignesh KrishNessuna valutazione finora

- Mining Frequent Itemsets and Association RulesDocumento59 pagineMining Frequent Itemsets and Association RulesSandeep DwivediNessuna valutazione finora

- Sap HR FaqDocumento36 pagineSap HR FaqAnonymous 5mSMeP2jNessuna valutazione finora

- Noa MopDocumento103 pagineNoa MopRaja SolaimalaiNessuna valutazione finora

- Common Core Standardized Test Review Math TutorialsDocumento3 pagineCommon Core Standardized Test Review Math Tutorialsagonza70Nessuna valutazione finora

- Comprehensive Project Plan - Sean SectionsDocumento2 pagineComprehensive Project Plan - Sean SectionsSean HodgsonNessuna valutazione finora

- Computer Processing of Human LanguageDocumento2 pagineComputer Processing of Human LanguageKym Algarme50% (2)

- Lecture 11 Unsupervised LearningDocumento19 pagineLecture 11 Unsupervised LearningHodatama Karanna OneNessuna valutazione finora

- Planning Advertising Campaign to Maximize New CustomersDocumento4 paginePlanning Advertising Campaign to Maximize New CustomersAdmin0% (1)

- ReadmeDocumento18 pagineReadmeankit99ankitNessuna valutazione finora

- Platform1 Server and N-MINI 2 Configuration Guide V1.01Documento47 paginePlatform1 Server and N-MINI 2 Configuration Guide V1.01sirengeniusNessuna valutazione finora

- Idm CrackDocumento34 pagineIdm CracktilalmansoorNessuna valutazione finora

- Time Series Using Stata (Oscar Torres-Reyna Version) : December 2007Documento32 pagineTime Series Using Stata (Oscar Torres-Reyna Version) : December 2007Humayun KabirNessuna valutazione finora

- Robo Guide BookDocumento18 pagineRobo Guide BookVenkateswar Reddy MallepallyNessuna valutazione finora

- Integrating Siebel Web Services Aug2006Documento146 pagineIntegrating Siebel Web Services Aug2006api-3732129100% (1)

- Vamsi Krishna Myalapalli ResumeDocumento2 pagineVamsi Krishna Myalapalli ResumeVamsi KrishnaNessuna valutazione finora

- Programmers PDFDocumento5 pagineProgrammers PDFSrinivasan SridharanNessuna valutazione finora