Potrebbero piacerti anche

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

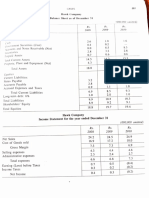

- BGS Case Study 1-10Documento5 pagineBGS Case Study 1-10gouse shareefNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- AFM Case 1Documento3 pagineAFM Case 1gouse shareefNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Accounts Case FolioDocumento9 pagineAccounts Case Foliogouse shareefNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- AFM Case 3Documento1 paginaAFM Case 3gouse shareefNessuna valutazione finora

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Round 7Documento4 pagineRound 7gouse shareefNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Nayak PDocumento17 pagineNayak Pgouse shareefNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Organisation Study PDFDocumento1 paginaThe Organisation Study PDFgouse shareefNessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Nayak PDocumento17 pagineNayak Pgouse shareefNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Impact of Strategic Human Resource Management On PerformnceDocumento11 pagineThe Impact of Strategic Human Resource Management On PerformnceMahmud AbdullahNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- ReportDocumento17 pagineReportgouse shareefNessuna valutazione finora

- Nayak PDocumento17 pagineNayak Pgouse shareefNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Nayak PDocumento17 pagineNayak Pgouse shareefNessuna valutazione finora

- Predicting The Tigris River Water Quality Within Baghdad, Iraq PDFDocumento9 paginePredicting The Tigris River Water Quality Within Baghdad, Iraq PDFSalam H AlhelaliNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Quality Engineering of Crude Palm Oil (Cpo) : Using Multiple Linear Regression To Estimate Free Fatty AcidDocumento8 pagineQuality Engineering of Crude Palm Oil (Cpo) : Using Multiple Linear Regression To Estimate Free Fatty AcidKalana JayatillakeNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- 2017 - OPUS Quant Advanced PDFDocumento205 pagine2017 - OPUS Quant Advanced PDFIngeniero Alfonzo Díaz Guzmán100% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Problem Set 10 (With Instructions) : Regression AnalysisDocumento6 pagineProblem Set 10 (With Instructions) : Regression AnalysisLily TranNessuna valutazione finora

- Franchising and Firm RiskDocumento11 pagineFranchising and Firm RiskWesley KristiantoNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Retail Store Operations Reliance Retail LTD: Summer Project/Internship ReportDocumento48 pagineRetail Store Operations Reliance Retail LTD: Summer Project/Internship ReportRaviRamchandaniNessuna valutazione finora

- T-Statistics:: ECON3014 (Fall 2011) 30. 9 & 6.10. 2011 (Tutorial 3)Documento3 pagineT-Statistics:: ECON3014 (Fall 2011) 30. 9 & 6.10. 2011 (Tutorial 3)skywalker_handsomeNessuna valutazione finora

- Datum ShiftDocumento11 pagineDatum ShiftHarshottam DhakadNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- An Introduction To Monte Carlo Simulations: Mattias JonssonDocumento26 pagineAn Introduction To Monte Carlo Simulations: Mattias JonssonAarohiShirkeNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Lesson 5 - Advanced Forecasting TopicsDocumento10 pagineLesson 5 - Advanced Forecasting TopicsAnuj BhasinNessuna valutazione finora

- 2011 12BScMathSciSylDocumento44 pagine2011 12BScMathSciSylramlal chapriNessuna valutazione finora

- Structural Equation ModelingDocumento42 pagineStructural Equation ModelingMuhammad Asad AliNessuna valutazione finora

- Adhe Friam Budhi 2015210068 Ekon0Mi Pembangunan Reguler 1 Cluster 2 3ADocumento17 pagineAdhe Friam Budhi 2015210068 Ekon0Mi Pembangunan Reguler 1 Cluster 2 3AALVEENNessuna valutazione finora

- Hasil SPSS: Tests of NormalityDocumento6 pagineHasil SPSS: Tests of NormalityAtin SagitaNessuna valutazione finora

- Bike Rental (Project)Documento16 pagineBike Rental (Project)abhishek singhNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- 19bit0404 VL2020210101940 Ast02Documento11 pagine19bit0404 VL2020210101940 Ast02Saji JosephNessuna valutazione finora

- University of Cambridge International Examinations General Certificate of Education Advanced LevelDocumento4 pagineUniversity of Cambridge International Examinations General Certificate of Education Advanced LevelHubbak KhanNessuna valutazione finora

- GigDocumento23 pagineGigsmudxxNessuna valutazione finora

- 3 SimpleLinearRegressionDocumento30 pagine3 SimpleLinearRegression2022CEP006 AYANKUMAR NASKARNessuna valutazione finora

- Functions AlphabeticalDocumento6 pagineFunctions AlphabeticalomraviNessuna valutazione finora

- ISLRDocumento9 pagineISLRAnuar YeraliyevNessuna valutazione finora

- Orthogonal Designs With MinitabDocumento11 pagineOrthogonal Designs With MinitabSetia LesmanaNessuna valutazione finora

- One-Sample Kolmogorov-Smirnov TestDocumento5 pagineOne-Sample Kolmogorov-Smirnov TestSatira BayuNessuna valutazione finora

- Propagation of Systematic and Random ErrorsDocumento3 paginePropagation of Systematic and Random ErrorsLourenz BiñasNessuna valutazione finora

- Trend AnalysisDocumento16 pagineTrend AnalysisNateNessuna valutazione finora

- Spatial AutocorrelationDocumento10 pagineSpatial AutocorrelationNanin Trianawati SugitoNessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Predicting Expressive Vocabulary Acquisition in Children With Intellectual Disabilities: A 2-Year Longitudinal StudyDocumento14 paginePredicting Expressive Vocabulary Acquisition in Children With Intellectual Disabilities: A 2-Year Longitudinal StudyMariana JaymeNessuna valutazione finora

- Addis Ababa University Libraries Electronic Thesis and DissertationDocumento5 pagineAddis Ababa University Libraries Electronic Thesis and Dissertationkatieellismanchester100% (1)

- ML (15cs73) Question BankDocumento6 pagineML (15cs73) Question BankKaushik SANessuna valutazione finora

- Stats Test IIDocumento3 pagineStats Test IILourdes1991Nessuna valutazione finora