Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

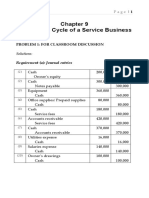

- Sol. Man. - Chapter 9 - Acctg Cycle of A Service BusinessDocumento52 pagineSol. Man. - Chapter 9 - Acctg Cycle of A Service Businesscan't yujout80% (5)

- 06 - Xyz Contracting Corporation Sample Financial Statements PDFDocumento11 pagine06 - Xyz Contracting Corporation Sample Financial Statements PDFFauTahudAmparoNessuna valutazione finora

- Copy Treasury StocksDocumento213 pagineCopy Treasury StocksJuren Demotor Dublin100% (2)

- A Coffee Shop Business PlandddDocumento12 pagineA Coffee Shop Business PlandddJholo AlvaradoNessuna valutazione finora

- Contract CostingDocumento18 pagineContract CostingAnant Jain100% (2)

- Assignment Questions For Financial StatementsDocumento5 pagineAssignment Questions For Financial StatementsAejaz Mohamed100% (2)

- Fabm 2-3Documento34 pagineFabm 2-3Janine Balcueva40% (5)

- Basic Accounting: Accounts Titles Date Debit CreditDocumento5 pagineBasic Accounting: Accounts Titles Date Debit CreditJamel torres82% (17)

- Testing & Educational Support in The US Industry Report PDFDocumento37 pagineTesting & Educational Support in The US Industry Report PDFbaiduyonghuwangyuan100% (1)

- Fra Solutions Chapter 1 Complete SolutionDocumento18 pagineFra Solutions Chapter 1 Complete SolutionViren DeshpandeNessuna valutazione finora

- Calculate Your Federal TaxesDocumento6 pagineCalculate Your Federal Taxesapi-719544021Nessuna valutazione finora

- Cost AccountingDocumento36 pagineCost AccountingNikhil PatelNessuna valutazione finora

- Fixed CostDocumento4 pagineFixed CostNiño Rey LopezNessuna valutazione finora

- P2 Question 2012Documento18 pagineP2 Question 2012Jake ManansalaNessuna valutazione finora

- Project Profile For Remica Woven Sack Tape Line 90MM With Hot Air Oven For 5.5 Tone - Per DayDocumento8 pagineProject Profile For Remica Woven Sack Tape Line 90MM With Hot Air Oven For 5.5 Tone - Per DayShivang BhavsarNessuna valutazione finora

- IM ACCO 20033 Financial Accounting and Reporting Part 1Documento95 pagineIM ACCO 20033 Financial Accounting and Reporting Part 1Montales, Julius Cesar D.Nessuna valutazione finora

- Tax, Budget, InterstDocumento10 pagineTax, Budget, InterstNegese MinaluNessuna valutazione finora

- PNG Rules 2008Documento30 paginePNG Rules 2008sunshine dreamNessuna valutazione finora

- Sample Grant AgreementDocumento6 pagineSample Grant Agreementemmanuel mwesigaNessuna valutazione finora

- Class 11 Accountancy Part 1 Chapter 2Documento4 pagineClass 11 Accountancy Part 1 Chapter 2Ioanna Maria MonopoliNessuna valutazione finora

- Glendale International School Offer Letter UaeDocumento5 pagineGlendale International School Offer Letter UaeTejas JadhavNessuna valutazione finora

- Revenue and Monetary Assets: Mcgraw-Hill/IrwinDocumento36 pagineRevenue and Monetary Assets: Mcgraw-Hill/IrwinAnkit KumarNessuna valutazione finora

- 9MFY18 MylanDocumento94 pagine9MFY18 MylanRahul GautamNessuna valutazione finora

- UOM Students' Union Bilan 2013/14Documento153 pagineUOM Students' Union Bilan 2013/14Rishikesh PoorunNessuna valutazione finora

- Final ProjectDocumento55 pagineFinal Projectpurva maratheNessuna valutazione finora

- Nonprofit AccountingDocumento19 pagineNonprofit AccountingMayari de AmanteNessuna valutazione finora

- Section 13: Fund Accounting Accounting Entries: Accounts ReceivableDocumento5 pagineSection 13: Fund Accounting Accounting Entries: Accounts ReceivablethisisghostactualNessuna valutazione finora

- Bank of The Philippine IslandsDocumento40 pagineBank of The Philippine IslandsRed Christian PalustreNessuna valutazione finora

- The Principles and History of Accounting: Block ReviewDocumento88 pagineThe Principles and History of Accounting: Block ReviewLlora Jane GuillermoNessuna valutazione finora