Potrebbero piacerti anche

- Accounting For Income Tax: LiabilityDocumento28 pagineAccounting For Income Tax: Liabilityadmiral spongebobNessuna valutazione finora

- Deferred TaxesDocumento17 pagineDeferred Taxesasdfghjkl100% (2)

- ALL Quiz Ia 3Documento29 pagineALL Quiz Ia 3julia4razoNessuna valutazione finora

- 62230126Documento20 pagine62230126ROMULO CUBIDNessuna valutazione finora

- Chapter 15 Ia2Documento21 pagineChapter 15 Ia2JM Valonda Villena, CPA, MBANessuna valutazione finora

- Answer: C - 465,000Documento9 pagineAnswer: C - 465,000kyle G50% (2)

- Lease Modules ContinuedDocumento8 pagineLease Modules ContinuedKenneth Marcial Ege0% (1)

- Random Problem 2 (Pinky)Documento23 pagineRandom Problem 2 (Pinky)spur iousNessuna valutazione finora

- Perdizo, Miljane.-Activity-9-9Documento4 paginePerdizo, Miljane.-Activity-9-9Miljane Perdizo67% (3)

- Cpa Review School of The Philippines ManilaDocumento3 pagineCpa Review School of The Philippines ManilaAljur SalamedaNessuna valutazione finora

- San Beda College Alabang Homework Exercise-Act851RDocumento4 pagineSan Beda College Alabang Homework Exercise-Act851RJomel BaptistaNessuna valutazione finora

- Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionDocumento15 pagineIdentify The Letter of The Choice That Best Completes The Statement or Answers The QuestionGabrielle100% (1)

- This Study Resource Was: Operating Lease and LeasebackDocumento7 pagineThis Study Resource Was: Operating Lease and LeasebackMarcus MonocayNessuna valutazione finora

- Contingent Liab Bonds PayableDocumento11 pagineContingent Liab Bonds PayableKristine Lirose Bordeos100% (1)

- R4acads Finacc ExtraDocumento5 pagineR4acads Finacc ExtraChristine Herico CurryNessuna valutazione finora

- A Professional Business School Financial Accounting and Reporting Exercises On Leases Finance Lease - LesseeDocumento4 pagineA Professional Business School Financial Accounting and Reporting Exercises On Leases Finance Lease - LesseeDaryl Dizon Cabanza100% (1)

- QuizDocumento32 pagineQuizEloisaNessuna valutazione finora

- (Pfrs/Ifrs 16) LeasesDocumento11 pagine(Pfrs/Ifrs 16) LeasesBromanineNessuna valutazione finora

- Ias 19 - Employee Benefits QUESTION 57-17Documento9 pagineIas 19 - Employee Benefits QUESTION 57-17Janella Gail ArenasNessuna valutazione finora

- Defined Benefit Plan-LectureDocumento17 pagineDefined Benefit Plan-LectureDyen100% (1)

- This Study Resource Was Shared Via: de La Salle LipaDocumento2 pagineThis Study Resource Was Shared Via: de La Salle LipaAngel ObligacionNessuna valutazione finora

- PAS37 ProbsDocumento4 paginePAS37 ProbsAngelicaNessuna valutazione finora

- 2.1.3 Statement of Financial PositionDocumento2 pagine2.1.3 Statement of Financial Positionjoint accountNessuna valutazione finora

- All Seatworks PDFDocumento14 pagineAll Seatworks PDFLouiseNessuna valutazione finora

- CSC 201-Leones, Mary Grace O. - IntermediateDocumento28 pagineCSC 201-Leones, Mary Grace O. - IntermediateMary Grace Ocampo LeonesNessuna valutazione finora

- Postemployment Benefits: Employee's Employee Employee Obligation DecemberDocumento25 paginePostemployment Benefits: Employee's Employee Employee Obligation DecemberGabriel PanganNessuna valutazione finora

- LeasesDocumento5 pagineLeasesCamille BacaresNessuna valutazione finora

- Financial Accounting: Theory & Practice Intangible AssetsDocumento81 pagineFinancial Accounting: Theory & Practice Intangible AssetsXNessuna valutazione finora

- Ch10&11. Shareholders' EquityDocumento29 pagineCh10&11. Shareholders' EquityHazell DNessuna valutazione finora

- Problem 5-31 (Verna Company)Documento7 pagineProblem 5-31 (Verna Company)Jannefah Irish SaglayanNessuna valutazione finora

- Quiz ReorganizationDocumento7 pagineQuiz ReorganizationJam SurdivillaNessuna valutazione finora

- 2nd Yr Midterm (2nd Sem) ReviewerDocumento19 pagine2nd Yr Midterm (2nd Sem) ReviewerC H ♥ N T Z60% (5)

- Group Activity 2 Answer KeyDocumento4 pagineGroup Activity 2 Answer Keykrisha milloNessuna valutazione finora

- Act Day 1-3Documento45 pagineAct Day 1-3Joyce Anne GarduqueNessuna valutazione finora

- Quiz 2-Current LiabilitiesDocumento6 pagineQuiz 2-Current LiabilitiesJam SurdivillaNessuna valutazione finora

- Finance Lease Lessee 1Documento23 pagineFinance Lease Lessee 1Judy100% (1)

- Activity 3-4 SB CompensationDocumento3 pagineActivity 3-4 SB CompensationNhel Alvaro0% (1)

- Sales&leasebackDocumento15 pagineSales&leasebackeulhiemae arong0% (1)

- Intacc Chapt 11 18 NoneDocumento24 pagineIntacc Chapt 11 18 NoneSean AustinNessuna valutazione finora

- Leases Part 3 - Other Accounting IssuesDocumento33 pagineLeases Part 3 - Other Accounting IssuesDanica RamosNessuna valutazione finora

- Info 1Documento28 pagineInfo 1Veejay Soriano Cuevas0% (1)

- Examination About Investment 13Documento2 pagineExamination About Investment 13BLACKPINKLisaRoseJisooJennieNessuna valutazione finora

- C3 - Warranty LiabilityDocumento12 pagineC3 - Warranty LiabilityRiza Kristine DaytoNessuna valutazione finora

- Finals Questionnaire A31 PDFDocumento8 pagineFinals Questionnaire A31 PDFAnne Marieline BuenaventuraNessuna valutazione finora

- Far 6660Documento2 pagineFar 6660Glessy Anne Marie FernandezNessuna valutazione finora

- Quiz 1-Current LiabDocumento11 pagineQuiz 1-Current LiabBadAssNessuna valutazione finora

- Accounting For Joint Arrangements Material 1Documento5 pagineAccounting For Joint Arrangements Material 1Erika Mae BarizoNessuna valutazione finora

- Share-Based Compensation-Share OptionsDocumento16 pagineShare-Based Compensation-Share OptionsLawrence YusiNessuna valutazione finora

- MODULE Midterm FAR 3 Leases5Documento28 pagineMODULE Midterm FAR 3 Leases5francis dungcaNessuna valutazione finora

- Solve Me PDFDocumento1 paginaSolve Me PDFWinona Anne EscarezNessuna valutazione finora

- FranchisingDocumento10 pagineFranchisingKRABBYPATTY PHNessuna valutazione finora

- Answer-F UNIT 2 - Practice and Exercises Answer-F UNIT 2 - Practice and ExercisesDocumento3 pagineAnswer-F UNIT 2 - Practice and Exercises Answer-F UNIT 2 - Practice and ExercisesDaniella Mae ElipNessuna valutazione finora

- ACC 211 SIM Week 6 7Documento40 pagineACC 211 SIM Week 6 7Threcia Rota50% (2)

- Accounting For Income TaxDocumento4 pagineAccounting For Income TaxRed YuNessuna valutazione finora

- FA2-08 Income TaxesDocumento3 pagineFA2-08 Income Taxeskrisha millo0% (1)

- Income Taxes: ProblemsDocumento12 pagineIncome Taxes: ProblemsCharles MateoNessuna valutazione finora

- Chapter 22 Deferred Tax Asset and LiabilityDocumento8 pagineChapter 22 Deferred Tax Asset and LiabilityCheesca Macabanti - 12 Euclid-Digital ModularNessuna valutazione finora

- Quizzz Intac 3Documento10 pagineQuizzz Intac 3lana del reyNessuna valutazione finora

- Accounting For Income TaxDocumento4 pagineAccounting For Income TaxShaira Bugayong0% (2)

- Income Tax 2Documento12 pagineIncome Tax 2You're WelcomeNessuna valutazione finora

- Prepared By: Mohammad Muariff S. Balang, CPA, Second Semester, AY 2012-2013Documento4 paginePrepared By: Mohammad Muariff S. Balang, CPA, Second Semester, AY 2012-2013Jayr BV100% (1)

- Orca Share Media1577676537770-1Documento3 pagineOrca Share Media1577676537770-1Jayr BV100% (1)

- 12 x10 Financial Statement AnalysisDocumento22 pagine12 x10 Financial Statement AnalysisRaffi Tamayo92% (25)

- Microsoft Office Tips and TricksDocumento12 pagineMicrosoft Office Tips and TricksJayr BVNessuna valutazione finora

- Contoh Soal - Ch15Documento52 pagineContoh Soal - Ch15Nurhanifah SoedarsNessuna valutazione finora

- Orca Share Media1577676537770-1Documento3 pagineOrca Share Media1577676537770-1Jayr BV100% (1)

- Orca Share Media1577676523240Documento4 pagineOrca Share Media1577676523240Jayr BVNessuna valutazione finora

- Ap SheDocumento9 pagineAp SheBryan JamesNessuna valutazione finora

- Orca Share Media1575043628730Documento4 pagineOrca Share Media1575043628730Jayr BV100% (1)

- Audit of Shareholders EquityDocumento6 pagineAudit of Shareholders EquityMark Lord Morales Bumagat71% (7)

- Orca Share Media1577676574590Documento7 pagineOrca Share Media1577676574590Jayr BV100% (1)

- Chapter 5 The Impact On The Life of ColonyDocumento1 paginaChapter 5 The Impact On The Life of ColonyJayr BVNessuna valutazione finora

- Office2010 Tips TricksDocumento15 pagineOffice2010 Tips TricksJayr BVNessuna valutazione finora

- Contoh Soal - Ch15Documento52 pagineContoh Soal - Ch15Nurhanifah SoedarsNessuna valutazione finora

- Ap SheDocumento9 pagineAp SheBryan JamesNessuna valutazione finora

- Orca Share Media1577676507201Documento4 pagineOrca Share Media1577676507201Jayr BVNessuna valutazione finora

- Orca Share Media1577676574590Documento7 pagineOrca Share Media1577676574590Jayr BV100% (1)

- Orca Share Media1577676574590Documento7 pagineOrca Share Media1577676574590Jayr BV100% (1)

- Orca Share Media1575043628730Documento4 pagineOrca Share Media1575043628730Jayr BV100% (1)

- Microsoft Word HintsDocumento4 pagineMicrosoft Word HintsJayr BVNessuna valutazione finora

- Auditing ProblemsDocumento5 pagineAuditing ProblemsJayr BVNessuna valutazione finora

- Airvad Aharam BookDocumento5 pagineAirvad Aharam BookrajeshNessuna valutazione finora

- AP - Shareholders Equity PDFDocumento5 pagineAP - Shareholders Equity PDFJasmin NgNessuna valutazione finora

- Office2010 Tips TricksDocumento15 pagineOffice2010 Tips TricksJayr BVNessuna valutazione finora

- Microsoft Word HintsDocumento4 pagineMicrosoft Word HintsJayr BVNessuna valutazione finora

- Chap 012Documento84 pagineChap 012Noushin Khan0% (2)

- Fabm2 G12 Q1 M7 WK7 PDFDocumento8 pagineFabm2 G12 Q1 M7 WK7 PDFJhoanna Odias100% (2)

- Statement of Financial Position: 1. True 6. True 2. False 7. True 3. True 8. False 4. False 9. True 5. True 10. FALSEDocumento10 pagineStatement of Financial Position: 1. True 6. True 2. False 7. True 3. True 8. False 4. False 9. True 5. True 10. FALSEMcy CaniedoNessuna valutazione finora

- 2018 DP World Annual Report EnglishDocumento77 pagine2018 DP World Annual Report EnglishGabriel CaraveteanuNessuna valutazione finora

- Sebi Rta Circular - 20.04.2018Documento10 pagineSebi Rta Circular - 20.04.2018Arun Kumar SharmaNessuna valutazione finora

- Module 1 - IntAcc1Documento7 pagineModule 1 - IntAcc1kakimog738Nessuna valutazione finora

- Limited Liability Partnership Act, 2008Documento13 pagineLimited Liability Partnership Act, 2008Yogendra PoswalNessuna valutazione finora

- Personal Finance AppendixDocumento27 paginePersonal Finance AppendixBara DanielNessuna valutazione finora

- Slate Finance Overview 3.0.2Documento20 pagineSlate Finance Overview 3.0.2Jesse Barrett-MillsNessuna valutazione finora

- Factors Affecting The Net Interest Margin of Commercial Bank of EthiopiaDocumento12 pagineFactors Affecting The Net Interest Margin of Commercial Bank of EthiopiaJASH MATHEWNessuna valutazione finora

- Ims GTDocumento6 pagineIms GTGijulOthmanNessuna valutazione finora

- Goodwill Valuation PartnershipDocumento12 pagineGoodwill Valuation PartnershipJmzkx SjxxkNessuna valutazione finora

- Ft232062 - Sec 2 - Rohit Gupta - SHG Business PlanDocumento8 pagineFt232062 - Sec 2 - Rohit Gupta - SHG Business PlanKanika SubbaNessuna valutazione finora

- TH TH THDocumento4 pagineTH TH THThia SolveNessuna valutazione finora

- Corporet ch2Documento57 pagineCorporet ch2birhanuNessuna valutazione finora

- BAC 112 Final Departmental Exam (Answer Key) RevisedDocumento12 pagineBAC 112 Final Departmental Exam (Answer Key) Revisedjanus lopezNessuna valutazione finora

- Rangkuman Bab 2 Akuntansi KeuanganDocumento11 pagineRangkuman Bab 2 Akuntansi KeuanganMuhammad Rusydi AzizNessuna valutazione finora

- Head Retail Banking President in Memphis TN Resume Terry RenouxDocumento3 pagineHead Retail Banking President in Memphis TN Resume Terry RenouxTerryRenouxNessuna valutazione finora

- Plant Maintenance StrategyDocumento8 paginePlant Maintenance Strategymirdza94Nessuna valutazione finora

- FR Compiler 4.0 - CA Final - by CA Ravi AgarwalDocumento1.312 pagineFR Compiler 4.0 - CA Final - by CA Ravi Agarwalaella shivani100% (1)

- Birch Paper Company FinalllllDocumento11 pagineBirch Paper Company FinalllllMadhuri Sangare100% (1)

- A Project Report: in Partial Fulfillment For The Award of The Degree ofDocumento56 pagineA Project Report: in Partial Fulfillment For The Award of The Degree ofTushar PatelNessuna valutazione finora

- 1211Documento201 pagine1211Angel CapellanNessuna valutazione finora

- Accounting MCQDocumento15 pagineAccounting MCQsamuelkish50% (2)

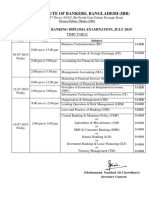

- 89th BDExam Time AbleDocumento1 pagina89th BDExam Time AblePair AhammedNessuna valutazione finora

- MSC Thesis ProposalDocumento47 pagineMSC Thesis ProposalEric Osei Owusu-kumihNessuna valutazione finora

- Vision 2021 BangladeshDocumento3 pagineVision 2021 BangladeshRiadush Shalehin JewelNessuna valutazione finora

- Vce Summmer Internship Program (Equity Research)Documento9 pagineVce Summmer Internship Program (Equity Research)Annu KashyapNessuna valutazione finora

- Finland Nokia Case StudyDocumento11 pagineFinland Nokia Case StudyBitan BanerjeeNessuna valutazione finora

- Annual ReportDocumento160 pagineAnnual ReportSivaNessuna valutazione finora