Potrebbero piacerti anche

- Accounting Survival Guide: An Introduction to Accounting for BeginnersDa EverandAccounting Survival Guide: An Introduction to Accounting for BeginnersNessuna valutazione finora

- What is Financial Accounting and BookkeepingDa EverandWhat is Financial Accounting and BookkeepingValutazione: 4 su 5 stelle4/5 (10)

- Accounting OverviewDocumento13 pagineAccounting OverviewMae AroganteNessuna valutazione finora

- Accounting DefinitionsDocumento5 pagineAccounting DefinitionsAli GoharNessuna valutazione finora

- Accountancy T20Documento38 pagineAccountancy T20Nischal HathiNessuna valutazione finora

- Business AccountingDocumento16 pagineBusiness AccountingMark 42Nessuna valutazione finora

- Assignment 03Documento9 pagineAssignment 03duhkhabilasa4Nessuna valutazione finora

- Learning Tally Erp 9Documento385 pagineLearning Tally Erp 9Samuel Zodingliana100% (2)

- Assingment Financial Accounting1Documento9 pagineAssingment Financial Accounting1ANURAG SHUKLANessuna valutazione finora

- LESSON 1 Introduction To Accounting LectureDocumento3 pagineLESSON 1 Introduction To Accounting LectureACCOUNTING STRESSNessuna valutazione finora

- Accounting: What It IsDocumento2 pagineAccounting: What It IsKumarNessuna valutazione finora

- Tally ERP 9 - TutorialDocumento1.192 pagineTally ERP 9 - TutorialChandan Mundhra85% (68)

- Tally ERP 9.0 Material Basics of Accounting 01Documento10 pagineTally ERP 9.0 Material Basics of Accounting 01Raghavendra yadav KM100% (1)

- Introduction To AccountingDocumento8 pagineIntroduction To Accountingjesi zamoraNessuna valutazione finora

- Introduction To AccountingDocumento8 pagineIntroduction To Accountingjesi zamoraNessuna valutazione finora

- Introduction To AccountingDocumento8 pagineIntroduction To Accountingjesi zamora0% (1)

- GAURAVDocumento12 pagineGAURAVSaurabh MishraNessuna valutazione finora

- Accounting & Accounting CycleDocumento34 pagineAccounting & Accounting CyclechstuNessuna valutazione finora

- Tally Lesson 1Documento13 pagineTally Lesson 1kumarbcomca100% (1)

- The Purpose and Use of The Accounting Records Which Used in MontehodgeDocumento15 pagineThe Purpose and Use of The Accounting Records Which Used in MontehodgeNime AhmedNessuna valutazione finora

- Understanding AccountingDocumento20 pagineUnderstanding Accountingrainman54321Nessuna valutazione finora

- Lesson 1: Basics of AccountingDocumento8 pagineLesson 1: Basics of AccountingkharemixNessuna valutazione finora

- Financial Accounting WORDDocumento18 pagineFinancial Accounting WORDramakrishnanNessuna valutazione finora

- Modern History of AccountingDocumento6 pagineModern History of AccountingShamim HossainNessuna valutazione finora

- Principles of Basic BookkeepingDocumento8 paginePrinciples of Basic Bookkeepingtunde adeniranNessuna valutazione finora

- Basics of Cost AccountingDocumento21 pagineBasics of Cost AccountingRose DallyNessuna valutazione finora

- What Is Accounting?Documento29 pagineWhat Is Accounting?gowthami ACCOUNTSNessuna valutazione finora

- Basic AccountsDocumento51 pagineBasic AccountsNilesh Indikar100% (1)

- Financial AccoountingDocumento5 pagineFinancial AccoountingASR07Nessuna valutazione finora

- Financial Fraud SchemesDocumento9 pagineFinancial Fraud SchemesPrabhu SachuNessuna valutazione finora

- An Introduction AccountingDocumento16 pagineAn Introduction AccountingArathy KrishnaNessuna valutazione finora

- ED Note Module - 3Documento63 pagineED Note Module - 3SATYARANJAN PATTANAIKNessuna valutazione finora

- Module 3 CFAS PDFDocumento7 pagineModule 3 CFAS PDFErmelyn GayoNessuna valutazione finora

- What Is Accounting?: Cash FlowsDocumento4 pagineWhat Is Accounting?: Cash FlowsMamun RezaNessuna valutazione finora

- The Essentials of Accounting BasicsDocumento21 pagineThe Essentials of Accounting Basicsbarber bobNessuna valutazione finora

- Safari - 7 Jul 2022 at 3:41 PMDocumento1 paginaSafari - 7 Jul 2022 at 3:41 PMKristy Veyna BautistaNessuna valutazione finora

- Fundamental of Accounting and Taxation NotesDocumento20 pagineFundamental of Accounting and Taxation NotesMohit100% (1)

- General AccountingDocumento94 pagineGeneral Accountingswaroopbaskey2100% (1)

- Equation Becomes: Assets A Liabilities L + Stockholders' Equity SEDocumento2 pagineEquation Becomes: Assets A Liabilities L + Stockholders' Equity SEJorge L CastelarNessuna valutazione finora

- Bookkeeping Is The Recording of Financial Transactions. Transactions Include SalesDocumento247 pagineBookkeeping Is The Recording of Financial Transactions. Transactions Include SalesSantosh PanigrahiNessuna valutazione finora

- Introduction To AccountsDocumento8 pagineIntroduction To AccountsSuraj MahantNessuna valutazione finora

- Assignment 7 Bhs. Inggris SintaDocumento3 pagineAssignment 7 Bhs. Inggris Sintasinta NuriaNessuna valutazione finora

- Chap 1 Accounting Nature Scope Concept and ConventionDocumento5 pagineChap 1 Accounting Nature Scope Concept and Conventionyousaf.mast777Nessuna valutazione finora

- What Is AccountingDocumento4 pagineWhat Is AccountingRechie Gimang AlferezNessuna valutazione finora

- Accountancy/Introduction To AccountancyDocumento16 pagineAccountancy/Introduction To AccountancyfaceandmaskNessuna valutazione finora

- Accounting: Step by Step Guide to Accounting Principles & Basic Accounting for Small businessDa EverandAccounting: Step by Step Guide to Accounting Principles & Basic Accounting for Small businessValutazione: 4.5 su 5 stelle4.5/5 (9)

- Accounting: A Simple Guide to Financial and Managerial Accounting for BeginnersDa EverandAccounting: A Simple Guide to Financial and Managerial Accounting for BeginnersNessuna valutazione finora

- Financial Accounting - Want to Become Financial Accountant in 30 Days?Da EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Valutazione: 5 su 5 stelle5/5 (1)

- Accounting: Accounting Made Simple for Beginners, Basic Accounting Principles and How to Do Your Own BookkeepingDa EverandAccounting: Accounting Made Simple for Beginners, Basic Accounting Principles and How to Do Your Own BookkeepingValutazione: 5 su 5 stelle5/5 (2)

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Da Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Nessuna valutazione finora

- Bookkeeping 101 For Business Professionals | Increase Your Accounting Skills And Create More Financial Stability And WealthDa EverandBookkeeping 101 For Business Professionals | Increase Your Accounting Skills And Create More Financial Stability And WealthNessuna valutazione finora

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersDa EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNessuna valutazione finora

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursDa EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNessuna valutazione finora

- CH 8Documento64 pagineCH 8Chang Chan ChongNessuna valutazione finora

- BMC 301 Case StudyDocumento22 pagineBMC 301 Case StudyTayaban Van GihNessuna valutazione finora

- Market Structures AADocumento30 pagineMarket Structures AAMohit WaniNessuna valutazione finora

- Value Chain Definition Model Analysis and ExampleDocumento9 pagineValue Chain Definition Model Analysis and ExampleSR-Rain Daniel EspinozaNessuna valutazione finora

- Sigma TechDocumento16 pagineSigma TechㄎㄎㄎㄎNessuna valutazione finora

- Immitation To Innovation - 1Documento10 pagineImmitation To Innovation - 1manoj1jsrNessuna valutazione finora

- Bakels Acquires Aromatic EngDocumento2 pagineBakels Acquires Aromatic EngMishtar MorpheneNessuna valutazione finora

- ACCG 2000 Week 9 Homework QuestionsDocumento1 paginaACCG 2000 Week 9 Homework QuestionsAlexander TrovatoNessuna valutazione finora

- James Okpanachi David PDFDocumento3 pagineJames Okpanachi David PDFkelvinNessuna valutazione finora

- Dipasri FIN321 Syllabus Fall 2013 MW1130amDocumento4 pagineDipasri FIN321 Syllabus Fall 2013 MW1130amJGONessuna valutazione finora

- Chapter (14) : The Marketing Mix: Promotion and Technology in MarketingDocumento25 pagineChapter (14) : The Marketing Mix: Promotion and Technology in MarketingAung Toe OONessuna valutazione finora

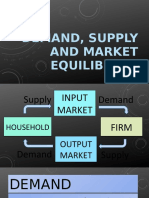

- Demand, Supply and Market EquilibriumDocumento102 pagineDemand, Supply and Market EquilibriumOG LautaNessuna valutazione finora

- Service Marketing ProjectDocumento8 pagineService Marketing ProjectRoyal WarjriNessuna valutazione finora

- A Research Proposal ON "A Study On Capital Structure of Indian Oil Corporation LTD"Documento8 pagineA Research Proposal ON "A Study On Capital Structure of Indian Oil Corporation LTD"DabiyalNessuna valutazione finora

- Problems Inter Acc1Documento10 pagineProblems Inter Acc1Chau NguyenNessuna valutazione finora

- Checklist - Loans and AdvancesDocumento11 pagineChecklist - Loans and AdvancesdasharathdhageNessuna valutazione finora

- BoilerJuice Dealer Deck For WebDocumento12 pagineBoilerJuice Dealer Deck For WebIan MarkowitzNessuna valutazione finora

- Business PlanDocumento7 pagineBusiness PlanKayla Dela Torre55% (11)

- Glamour National Days 2019 PDFDocumento6 pagineGlamour National Days 2019 PDFaminikoNessuna valutazione finora

- 5 MarksDocumento3 pagine5 MarksDharma ProductionsNessuna valutazione finora

- EcstasticDocumento82 pagineEcstasticCristian D. BaldozNessuna valutazione finora

- Lec # 01 Consumer BehaviorDocumento29 pagineLec # 01 Consumer Behaviormuhammad qasimNessuna valutazione finora

- Chapter 8 Brand PositioningDocumento15 pagineChapter 8 Brand PositioningThirumal ReddyNessuna valutazione finora

- Material ManagmentDocumento41 pagineMaterial ManagmentPremendra Sahu100% (1)

- TT-2 MCQDocumento7 pagineTT-2 MCQKapilBudhiraja100% (1)

- Module 3: Generally Accepted Accounting PrinciplesDocumento5 pagineModule 3: Generally Accepted Accounting PrinciplesDarwin AniarNessuna valutazione finora

- Economics: Questions FromDocumento5 pagineEconomics: Questions FromManupa PereraNessuna valutazione finora

- Rural Marketing Project in MaricoDocumento28 pagineRural Marketing Project in MaricoViresh N BhatNessuna valutazione finora

- AC7.02 Advanced Management Accounting: Theory of Constraints Lowdown Sandals QuestionDocumento2 pagineAC7.02 Advanced Management Accounting: Theory of Constraints Lowdown Sandals QuestionKumar BistaNessuna valutazione finora

- Santoshi Patil Pattan 11Documento60 pagineSantoshi Patil Pattan 11balaji xeroxNessuna valutazione finora