Potrebbero piacerti anche

- TaxationDocumento7 pagineTaxationDorothy ApolinarioNessuna valutazione finora

- Auditing and Assurance Exam MidtermDocumento4 pagineAuditing and Assurance Exam MidtermMica Ella San DiegoNessuna valutazione finora

- Cup 3 Questions Answer KeyDocumento34 pagineCup 3 Questions Answer KeyDenmarc John AragosNessuna valutazione finora

- LiabilitiesDocumento15 pagineLiabilitiesegroj arucalamNessuna valutazione finora

- Cherein Pael - Midterm Project Sept 30 - PROBLEM1Documento1 paginaCherein Pael - Midterm Project Sept 30 - PROBLEM1cherein6soriano6paelNessuna valutazione finora

- Conceptual Framework and Accounting Standards Ms. Leslie Anne T. GandiaDocumento2 pagineConceptual Framework and Accounting Standards Ms. Leslie Anne T. GandiaJm SevallaNessuna valutazione finora

- Audit of SHE 1Documento2 pagineAudit of SHE 1Raz MahariNessuna valutazione finora

- Finals Quiz 2 Buscom Version 2Documento3 pagineFinals Quiz 2 Buscom Version 2Kristina Angelina ReyesNessuna valutazione finora

- Review - Practical Accounting 1Documento2 pagineReview - Practical Accounting 1Kath LeynesNessuna valutazione finora

- Chapter 8Documento7 pagineChapter 8Yenelyn Apistar CambarijanNessuna valutazione finora

- 105 PrelimDocumento10 pagine105 PrelimEly DoNessuna valutazione finora

- SCM Finals - Extra CreditDocumento16 pagineSCM Finals - Extra CreditEnola HolmesNessuna valutazione finora

- Franchise PDFDocumento1 paginaFranchise PDFJonathan VidarNessuna valutazione finora

- DocxDocumento10 pagineDocxAiziel OrenseNessuna valutazione finora

- Practice Set 1Documento4 paginePractice Set 1Shiela Mae BautistaNessuna valutazione finora

- Exercises - Percentage TaxesDocumento2 pagineExercises - Percentage TaxesMaristella GatonNessuna valutazione finora

- 11.11.2017 Audit of PPEDocumento9 pagine11.11.2017 Audit of PPEPatOcampoNessuna valutazione finora

- Semi Quiz 1Documento2 pagineSemi Quiz 1jp careNessuna valutazione finora

- This Study Resource Was: Mr. X Has The Following Data On His Passive Income Earned During 2019Documento1 paginaThis Study Resource Was: Mr. X Has The Following Data On His Passive Income Earned During 2019Anne Marieline BuenaventuraNessuna valutazione finora

- CMPC 221 Finals Quiz 2Documento5 pagineCMPC 221 Finals Quiz 2Maria CristinaNessuna valutazione finora

- You Will Be A CPA in 2019Documento12 pagineYou Will Be A CPA in 2019jose amoresNessuna valutazione finora

- Special Revenue Recognition Special Revenue RecognitionDocumento4 pagineSpecial Revenue Recognition Special Revenue RecognitionCee Gee BeeNessuna valutazione finora

- CE On Agriculture T1 AY2020-2021Documento2 pagineCE On Agriculture T1 AY2020-2021Luna MeowNessuna valutazione finora

- Audit Liability 09 Chapter 7Documento2 pagineAudit Liability 09 Chapter 7Ma Teresa B. CerezoNessuna valutazione finora

- 3.3 Exercise - Improperly Accumulated Earnings TaxDocumento2 pagine3.3 Exercise - Improperly Accumulated Earnings TaxRenzo KarununganNessuna valutazione finora

- An SME Prepared The Following Post Closing Trial Balance at YearDocumento1 paginaAn SME Prepared The Following Post Closing Trial Balance at YearRaca DesuNessuna valutazione finora

- 90,000 40,000 102,000 Correct Answer 110,000 100,000 300,000 312,000 314,000Documento11 pagine90,000 40,000 102,000 Correct Answer 110,000 100,000 300,000 312,000 314,000Hazel Grace PaguiaNessuna valutazione finora

- De Guzman Module 7Documento9 pagineDe Guzman Module 7Ma Ruby II SantosNessuna valutazione finora

- QUIZ REVIEW Homework Tutorial Chapter 5Documento5 pagineQUIZ REVIEW Homework Tutorial Chapter 5Cody TarantinoNessuna valutazione finora

- BLT 101Documento14 pagineBLT 101NIMOTHI LASENessuna valutazione finora

- LeasesDocumento5 pagineLeasesCamille BacaresNessuna valutazione finora

- ACCTSPTRANS All About PartnershipDocumento7 pagineACCTSPTRANS All About PartnershipShailene David0% (1)

- This Study Resource WasDocumento4 pagineThis Study Resource WasReznakNessuna valutazione finora

- 12 - Cost and Equity MethodDocumento2 pagine12 - Cost and Equity MethodregenNessuna valutazione finora

- Tax LQ1 2Documento21 pagineTax LQ1 2Maddy EscuderoNessuna valutazione finora

- Prac 1Documento9 paginePrac 1rayNessuna valutazione finora

- Chapter 09Documento16 pagineChapter 09FireBNessuna valutazione finora

- Far 6660Documento2 pagineFar 6660Glessy Anne Marie FernandezNessuna valutazione finora

- AUDIT Journal 6Documento17 pagineAUDIT Journal 6Daena NicodemusNessuna valutazione finora

- VatDocumento13 pagineVatJohn Derek GarreroNessuna valutazione finora

- Fedillaga Case13Documento19 pagineFedillaga Case13Luke Ysmael FedillagaNessuna valutazione finora

- p1 IaDocumento1 paginap1 IaLeika Gay Soriano OlarteNessuna valutazione finora

- Taxation KeyDocumento12 pagineTaxation KeyRerereNessuna valutazione finora

- Semi Final Exam AE23Documento6 pagineSemi Final Exam AE23HotcheeseramyeonNessuna valutazione finora

- Audit Liability 04 Chapter 7Documento1 paginaAudit Liability 04 Chapter 7Ma Teresa B. CerezoNessuna valutazione finora

- DocxDocumento35 pagineDocxjikee11Nessuna valutazione finora

- DeductionsDocumento4 pagineDeductionsDianna RabadonNessuna valutazione finora

- Self-Instructional Manual (SIM) For Self-Directed Learning (SDL)Documento106 pagineSelf-Instructional Manual (SIM) For Self-Directed Learning (SDL)Maria AnnaNessuna valutazione finora

- Practical Accounting 1: 2011 National Cpa Mock Board ExaminationDocumento7 paginePractical Accounting 1: 2011 National Cpa Mock Board Examinationcacho cielo graceNessuna valutazione finora

- ReportDocumento4 pagineReportryan angelica allanicNessuna valutazione finora

- 2018 - 2019 MAS 01 70mcqDocumento30 pagine2018 - 2019 MAS 01 70mcqMarc Allen Anthony GanNessuna valutazione finora

- Local Media271226407970108268Documento17 pagineLocal Media271226407970108268Jana Rose PaladaNessuna valutazione finora

- OPT QuizDocumento5 pagineOPT QuizAngeline VergaraNessuna valutazione finora

- Corumbrillo Far q1q2Documento7 pagineCorumbrillo Far q1q2Leane MarcoletaNessuna valutazione finora

- 5 6188442313212035099Documento19 pagine5 6188442313212035099JamieNessuna valutazione finora

- Answer The Following With Speed and Accuracy. Solutions Must Be DisclosedDocumento4 pagineAnswer The Following With Speed and Accuracy. Solutions Must Be DisclosedUNKNOWNNNessuna valutazione finora

- IAET TaxationDocumento2 pagineIAET TaxationRandy Manzano100% (1)

- Tax DeductionsDocumento4 pagineTax DeductionsAnonymous LC5kFdtcNessuna valutazione finora

- Straight Problems Income Tax Bsa2Documento2 pagineStraight Problems Income Tax Bsa2dimpy dNessuna valutazione finora

- Name: Date: Score:: Property of STIDocumento3 pagineName: Date: Score:: Property of STICharise OlivaNessuna valutazione finora

- Microsoft CorporationDocumento2 pagineMicrosoft CorporationJefferson MañaleNessuna valutazione finora

- Microsoft ReferencesDocumento1 paginaMicrosoft ReferencesJefferson MañaleNessuna valutazione finora

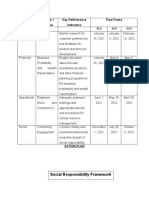

- Action Plan and Social Responsibility FrameworkDocumento2 pagineAction Plan and Social Responsibility FrameworkJefferson MañaleNessuna valutazione finora

- Microsoft ReferencesDocumento1 paginaMicrosoft ReferencesJefferson MañaleNessuna valutazione finora

- Microsoft CorporationDocumento2 pagineMicrosoft CorporationJefferson MañaleNessuna valutazione finora

- Jefferson M. Mañale Law On Obligations and ContractsDocumento9 pagineJefferson M. Mañale Law On Obligations and ContractsJefferson MañaleNessuna valutazione finora

- Answered Step-By-Step: Data Relating To The Shareholders' Equity of Martin Co. During..Documento8 pagineAnswered Step-By-Step: Data Relating To The Shareholders' Equity of Martin Co. During..Jefferson MañaleNessuna valutazione finora

- Answered Step-By-Step: Problem 1 Data Relating To The Shareholders' Equity of Carlo Co...Documento5 pagineAnswered Step-By-Step: Problem 1 Data Relating To The Shareholders' Equity of Carlo Co...Jefferson MañaleNessuna valutazione finora

- Answered Step-By-Step: Problem 1 Data Relating To The Shareholders' Equity of Carlo Co...Documento5 pagineAnswered Step-By-Step: Problem 1 Data Relating To The Shareholders' Equity of Carlo Co...Jefferson MañaleNessuna valutazione finora

- 14 x11 Financial Management BDocumento10 pagine14 x11 Financial Management Balexandro_novora639671% (14)

- Book ReviewDocumento1 paginaBook ReviewJefferson MañaleNessuna valutazione finora

- Gurus of Total QualityDocumento24 pagineGurus of Total QualityJefferson MañaleNessuna valutazione finora

- Ralph P 658 662Documento4 pagineRalph P 658 662Jefferson MañaleNessuna valutazione finora

- Management Advisory Services PDFDocumento50 pagineManagement Advisory Services PDFDea Lyn Bacula100% (6)

- Lit PpopDocumento3 pagineLit PpopJefferson MañaleNessuna valutazione finora

- Abridged PDP 2017 2022 FinalDocumento56 pagineAbridged PDP 2017 2022 FinalMJ CarreonNessuna valutazione finora

- Chapter 10Documento41 pagineChapter 10Jefferson MañaleNessuna valutazione finora

- Exercise CorporationDocumento3 pagineExercise CorporationJefferson MañaleNessuna valutazione finora

- CommerceDocumento1 paginaCommerceJefferson MañaleNessuna valutazione finora

- Multiple Choice Questions: Appendix II 81Documento7 pagineMultiple Choice Questions: Appendix II 81Smile LyNessuna valutazione finora

- Buckwold12e Solutions Ch11Documento40 pagineBuckwold12e Solutions Ch11Fang YanNessuna valutazione finora

- Introduction To Income TaxationDocumento4 pagineIntroduction To Income TaxationJean Diane JoveloNessuna valutazione finora

- Annisa Putri Ariyanto - Lembar Kerja Buku Besar - PT AC NOL DERAJATDocumento12 pagineAnnisa Putri Ariyanto - Lembar Kerja Buku Besar - PT AC NOL DERAJATannisa putriNessuna valutazione finora

- Treatment To GST While Assessing A LossDocumento3 pagineTreatment To GST While Assessing A LossAmit BakleNessuna valutazione finora

- Week 4 P4.21 Modified Question PDFDocumento1 paginaWeek 4 P4.21 Modified Question PDFalexandraNessuna valutazione finora

- Remedies Assessment DiagramDocumento3 pagineRemedies Assessment Diagramattymaneka100% (2)

- Domestice Tax Laws of Uganda (2017 Edition)Documento422 pagineDomestice Tax Laws of Uganda (2017 Edition)African Centre for Media Excellence100% (2)

- Solved John and Marsha Are Married and Filed A Joint ReturnDocumento1 paginaSolved John and Marsha Are Married and Filed A Joint ReturnAnbu jaromiaNessuna valutazione finora

- Information About Moving ExpensesDocumento6 pagineInformation About Moving ExpensesSebastien OuelletNessuna valutazione finora

- Four Year Profit ProjectionDocumento1 paginaFour Year Profit ProjectionDebbieNessuna valutazione finora

- Investment Declaration Format FY 2022-23Documento3 pagineInvestment Declaration Format FY 2022-23Divya WaghmareNessuna valutazione finora

- 85 Pacquiao v. CIRDocumento1 pagina85 Pacquiao v. CIRVon Lee De LunaNessuna valutazione finora

- First Lepanto Taisho Insurance Corporation vs. BirDocumento5 pagineFirst Lepanto Taisho Insurance Corporation vs. Birlaw mabaylabayNessuna valutazione finora

- Tax 1 Course OutlineDocumento5 pagineTax 1 Course OutlineChanel GarciaNessuna valutazione finora

- Benjamin Franklin Hipp AnalysisDocumento1 paginaBenjamin Franklin Hipp Analysisapi-318761358Nessuna valutazione finora

- Fit Chap012Documento56 pagineFit Chap012djkfhadskjfhksd100% (2)

- E20934 Payslip Aug2022Documento1 paginaE20934 Payslip Aug2022vikramNessuna valutazione finora

- Met Loan & Life Suraksha - Sample Premium Rates UIN:117N080V01Documento6 pagineMet Loan & Life Suraksha - Sample Premium Rates UIN:117N080V01Sadasivuni007Nessuna valutazione finora

- Order Confirmation-OC3309Documento1 paginaOrder Confirmation-OC3309Chetan patilNessuna valutazione finora

- Congress of The Philippines Metro ManilaDocumento13 pagineCongress of The Philippines Metro ManilaLyna Manlunas GayasNessuna valutazione finora

- Amazon InvoiceDocumento1 paginaAmazon InvoiceChandra BhushanNessuna valutazione finora

- Central Vs CTADocumento2 pagineCentral Vs CTATon Ton CananeaNessuna valutazione finora

- Transaction Report For Juan Pablo Rodriguez Virasoro Date Range Filter CustomerDocumento1 paginaTransaction Report For Juan Pablo Rodriguez Virasoro Date Range Filter CustomerJuan VirazoroNessuna valutazione finora

- BankDocumento1 paginaBankKixeagleNessuna valutazione finora

- 15 Sep 2022.PROPERTY - TAX - 0517 17 1201 0001 R3108942281157440176Documento1 pagina15 Sep 2022.PROPERTY - TAX - 0517 17 1201 0001 R3108942281157440176DHANU DANGINessuna valutazione finora

- Reliance Retail LimitedDocumento2 pagineReliance Retail LimitedKarna Satish KumarNessuna valutazione finora

- Invoice APFR 440Documento1 paginaInvoice APFR 440Loren AbantoNessuna valutazione finora

- Elmex Terminal Price ListDocumento5 pagineElmex Terminal Price ListJitendraAnneNessuna valutazione finora

- Vodafone Case SummaryDocumento3 pagineVodafone Case SummaryShubham NathNessuna valutazione finora

- TDS Report 27-06-2023Documento2 pagineTDS Report 27-06-2023AVDHESH YADAVNessuna valutazione finora