Potrebbero piacerti anche

- Software Associates Case AnalysisDocumento8 pagineSoftware Associates Case AnalysisMuhammad AsifNessuna valutazione finora

- Software AssociatesDocumento6 pagineSoftware Associatesshshank pandeyNessuna valutazione finora

- Cost Management - Software Associate CaseDocumento7 pagineCost Management - Software Associate CaseVaibhav GuptaNessuna valutazione finora

- Cafés Monte Bianco - Questions and Additional DataDocumento1 paginaCafés Monte Bianco - Questions and Additional DataMarco BolzonelloNessuna valutazione finora

- MANAC-II Assignment: by Abhinav Prusty - B19001 Hari Sankar S - B19018 Soham Ghosh - B19052Documento6 pagineMANAC-II Assignment: by Abhinav Prusty - B19001 Hari Sankar S - B19018 Soham Ghosh - B19052harisankar sureshNessuna valutazione finora

- JHT Case ExcelDocumento4 pagineJHT Case Excelanup akasheNessuna valutazione finora

- SUBJECT: Analyses and Recommendations For The Different Cost AccountingDocumento4 pagineSUBJECT: Analyses and Recommendations For The Different Cost AccountinglddNessuna valutazione finora

- Mystic SportsDocumento34 pagineMystic SportshelloNessuna valutazione finora

- Cafe Monte BiancoDocumento21 pagineCafe Monte BiancoWilliam Torrez OrozcoNessuna valutazione finora

- Software Asssociates11Documento13 pagineSoftware Asssociates11Arslan ShaikhNessuna valutazione finora

- Chemalite Cash Flow StatementDocumento2 pagineChemalite Cash Flow Statementrishika rshNessuna valutazione finora

- Project Rosemont Hill Health CenterDocumento9 pagineProject Rosemont Hill Health CenterSANDEEP AGRAWALNessuna valutazione finora

- Vaibhav Maheshwari Merrimack Tractors 2011pgp926Documento3 pagineVaibhav Maheshwari Merrimack Tractors 2011pgp926studvabzNessuna valutazione finora

- Dave BrothersDocumento6 pagineDave BrothersSangtani PareshNessuna valutazione finora

- Rosemont Health Center Rev01Documento7 pagineRosemont Health Center Rev01Amit VishwakarmaNessuna valutazione finora

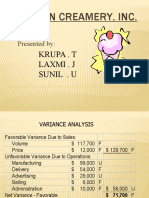

- Boston Creamery CaseDocumento9 pagineBoston Creamery Caselion_heart3001100% (1)

- Group - 9 - Sec - B - IQDM - Merton - Truck - CompanyDocumento8 pagineGroup - 9 - Sec - B - IQDM - Merton - Truck - CompanyMANVENDRA SINGH PGP 2019-21 BatchNessuna valutazione finora

- Otago MuseumDocumento19 pagineOtago MuseumFoamdomeNessuna valutazione finora

- Miles High Cycles Katherine Roland and John ConnorsDocumento4 pagineMiles High Cycles Katherine Roland and John ConnorsvivekNessuna valutazione finora

- 05 Wilkerson Company Solution - StudentsDocumento9 pagine05 Wilkerson Company Solution - StudentsVinyabhooshan Bajpai PGP 2022-24 Batch100% (1)

- Sharing Sheet Hallstead JewelersDocumento11 pagineSharing Sheet Hallstead JewelersHarpreet SinghNessuna valutazione finora

- Bill French Case Submitted By: Sourabh Phanase Section: ADocumento2 pagineBill French Case Submitted By: Sourabh Phanase Section: AsourabhphanaseNessuna valutazione finora

- Cafes Monte Biance Sol SelfDocumento2 pagineCafes Monte Biance Sol SelfahsanzmNessuna valutazione finora

- Hospital SupplyDocumento3 pagineHospital SupplyJeanne Madrona100% (1)

- Bill French - Write Up1Documento10 pagineBill French - Write Up1Nina EllyanaNessuna valutazione finora

- Millichem Solution XDocumento6 pagineMillichem Solution XMuhammad JunaidNessuna valutazione finora

- Wilkerson Company - Class PracticeDocumento5 pagineWilkerson Company - Class PracticeYAKSH DODIANessuna valutazione finora

- Solved The Dijon Company S Total Variable Cost Function Is TVC 50qDocumento1 paginaSolved The Dijon Company S Total Variable Cost Function Is TVC 50qM Bilal SaleemNessuna valutazione finora

- Wilkerson Company Case Numerical Approach SolutionDocumento3 pagineWilkerson Company Case Numerical Approach SolutionAbdul Rauf JamroNessuna valutazione finora

- EX 1 - WilkersonDocumento8 pagineEX 1 - WilkersonDror PazNessuna valutazione finora

- Boston CreameryDocumento11 pagineBoston CreameryJelline Gaza100% (3)

- Cost Management Accounting Assignment Bill French Case StudyDocumento5 pagineCost Management Accounting Assignment Bill French Case Studydeepak boraNessuna valutazione finora

- Case1 Nett Colorscope SaddamrobertobinuDocumento10 pagineCase1 Nett Colorscope SaddamrobertobinucicishintyaNessuna valutazione finora

- The ALLTEL Pavilion Case - Strategy and CVP Analysis PDFDocumento7 pagineThe ALLTEL Pavilion Case - Strategy and CVP Analysis PDFPritam Kumar NayakNessuna valutazione finora

- Manac Asn4 HydrochemDocumento6 pagineManac Asn4 HydrochemNikhil JindalNessuna valutazione finora

- Otago's MuseumDocumento5 pagineOtago's Museumyecika50% (2)

- This Study Resource Was: Forner CarpetDocumento4 pagineThis Study Resource Was: Forner CarpetLi CarinaNessuna valutazione finora

- Elwy Melina-Sarah MHCDocumento7 pagineElwy Melina-Sarah MHCpalak32Nessuna valutazione finora

- Sec-A - Group 8 - SecureNowDocumento7 pagineSec-A - Group 8 - SecureNowPuneet GargNessuna valutazione finora

- Vyaderm-Case Analysis 2006Documento4 pagineVyaderm-Case Analysis 2006Mridul SharmaNessuna valutazione finora

- PIA Hawaii Emirates Easy Jet: Breakeven AnalysisDocumento3 paginePIA Hawaii Emirates Easy Jet: Breakeven AnalysissaadsahilNessuna valutazione finora

- C1 - Rosemont MANAC SolutionDocumento13 pagineC1 - Rosemont MANAC Solutionkaushal dhapare100% (1)

- Chemalite Inc - Assignment - AccountingDocumento2 pagineChemalite Inc - Assignment - Accountingthi_aar100% (1)

- Baldwin Bicycle Company - Final Assignment - Group F - 20210728Documento4 pagineBaldwin Bicycle Company - Final Assignment - Group F - 20210728ApoorvaNessuna valutazione finora

- Case-5 Beauregard Textile CompanyDocumento8 pagineCase-5 Beauregard Textile CompanyMona SahooNessuna valutazione finora

- Guideline ICE1 TextOnlyDocumento4 pagineGuideline ICE1 TextOnlyRima AkidNessuna valutazione finora

- Hydrochem AnalysisDocumento7 pagineHydrochem AnalysisSaransh Kejriwal100% (2)

- Chapter 5Documento30 pagineChapter 5فاطمه حسينNessuna valutazione finora

- CVPDocumento3 pagineCVPRajShekarReddyNessuna valutazione finora

- Software Associates-Variance Analysis and Flexible BudgetingDocumento4 pagineSoftware Associates-Variance Analysis and Flexible Budgetingk_Dashy846550% (2)

- Baldwin Bicycle CompanyDocumento19 pagineBaldwin Bicycle CompanyMannu83Nessuna valutazione finora

- Anagene Case StudyDocumento1 paginaAnagene Case StudySam Man0% (3)

- The Quaker Oats Company and Subsidiaries Consolidated Statements of IncomeDocumento3 pagineThe Quaker Oats Company and Subsidiaries Consolidated Statements of IncomeNaseer AhmedNessuna valutazione finora

- About The Software Associates CaseDocumento7 pagineAbout The Software Associates CaseNikita GulguleNessuna valutazione finora

- Software Associate SolutionDocumento6 pagineSoftware Associate SolutionAnupam SinghNessuna valutazione finora

- Software AssociatesDocumento5 pagineSoftware AssociatesAgrata Pandey77% (13)

- Variance Assignment Managerial AccountingDocumento5 pagineVariance Assignment Managerial Accountingk_Dashy8465100% (4)

- Software Associates Assignment 2Documento8 pagineSoftware Associates Assignment 2Sahil Sheth100% (2)

- SOLUTIONS - Practice Final ExamDocumento12 pagineSOLUTIONS - Practice Final ExamsebmccabeeNessuna valutazione finora

- Module 6 SolutionsDocumento6 pagineModule 6 SolutionsNeha Wadhwani AhujaNessuna valutazione finora

- FM B19030Documento1 paginaFM B19030Nikhil JindalNessuna valutazione finora

- New Case ManacDocumento7 pagineNew Case ManacNikhil JindalNessuna valutazione finora

- Manac Asn4 HydrochemDocumento6 pagineManac Asn4 HydrochemNikhil JindalNessuna valutazione finora

- Manac Asn1 SiemensDocumento5 pagineManac Asn1 SiemensNikhil Jindal100% (1)

- Resume SampleDocumento3 pagineResume SampleNikhil JindalNessuna valutazione finora

- Bromelia in Bolivia Key Chiquitania PDFDocumento10 pagineBromelia in Bolivia Key Chiquitania PDFthrashingoNessuna valutazione finora

- Math Review 10 20222023Documento1 paginaMath Review 10 20222023Bui VyNessuna valutazione finora

- Grandparents 2Documento13 pagineGrandparents 2api-288503311Nessuna valutazione finora

- Republic Act. 10157Documento24 pagineRepublic Act. 10157roa yusonNessuna valutazione finora

- Mass of Christ The Savior by Dan Schutte LyricsDocumento1 paginaMass of Christ The Savior by Dan Schutte LyricsMark Greg FyeFye II33% (3)

- 520082272054091201Documento1 pagina520082272054091201Shaikh AdilNessuna valutazione finora

- Existentialist EthicsDocumento6 pagineExistentialist EthicsCarlos Peconcillo ImperialNessuna valutazione finora

- Education Rules 2012Documento237 pagineEducation Rules 2012Veimer ChanNessuna valutazione finora

- Ooad Lab Question SetDocumento3 pagineOoad Lab Question SetMUKESH RAJA P IT Student100% (1)

- Torrens System: Principle of TsDocumento11 pagineTorrens System: Principle of TsSyasya FatehaNessuna valutazione finora

- Adrian Campbell 2009Documento8 pagineAdrian Campbell 2009adrianrgcampbellNessuna valutazione finora

- Eapp Module 7 W11Documento5 pagineEapp Module 7 W11Valerie AsteriaNessuna valutazione finora

- Universalism and Cultural Relativism in Social Work EthicsDocumento16 pagineUniversalism and Cultural Relativism in Social Work EthicsEdu ArdoNessuna valutazione finora

- Tribunal Judgment On QLASSIC in MalaysiaDocumento14 pagineTribunal Judgment On QLASSIC in Malaysiatechiong ganNessuna valutazione finora

- A Princess With A Big Heart Grade4week1 q4Documento1 paginaA Princess With A Big Heart Grade4week1 q4Gelly FabricanteNessuna valutazione finora

- Business Plan FinalDocumento28 pagineBusiness Plan FinalErica Millicent TenecioNessuna valutazione finora

- Case LawsDocumento4 pagineCase LawsLalgin KurianNessuna valutazione finora

- Aquarium Aquarius Megalomania: Danish Norwegian Europop Barbie GirlDocumento2 pagineAquarium Aquarius Megalomania: Danish Norwegian Europop Barbie GirlTuan DaoNessuna valutazione finora

- Walt DisneyDocumento56 pagineWalt DisneyDaniela Denisse Anthawer Luna100% (6)

- 137684-1980-Serrano v. Central Bank of The PhilippinesDocumento5 pagine137684-1980-Serrano v. Central Bank of The Philippinespkdg1995Nessuna valutazione finora

- ORENDAIN vs. TRUSTEESHIP OF THE ESTATE OF DOÑA MARGARITA RODRIGUEZ PDFDocumento3 pagineORENDAIN vs. TRUSTEESHIP OF THE ESTATE OF DOÑA MARGARITA RODRIGUEZ PDFRhev Xandra Acuña100% (2)

- The Officers of Bardwell Company Are Reviewing The ProfitabilityDocumento1 paginaThe Officers of Bardwell Company Are Reviewing The ProfitabilityAmit PandeyNessuna valutazione finora

- Vespers Conversion of Saint PaulDocumento7 pagineVespers Conversion of Saint PaulFrancis Carmelle Tiu DueroNessuna valutazione finora

- 01 - Quality Improvement in The Modern Business Environment - Montgomery Ch01Documento75 pagine01 - Quality Improvement in The Modern Business Environment - Montgomery Ch01Ollyvia Faliani MuchlisNessuna valutazione finora

- Creating A Carwash Business PlanDocumento7 pagineCreating A Carwash Business PlanChai Yeng LerNessuna valutazione finora

- City Development PlanDocumento139 pagineCity Development Planstolidness100% (1)

- Qualified Written RequestDocumento9 pagineQualified Written Requestteachezi100% (3)

- Descriptive Text TaskDocumento12 pagineDescriptive Text TaskM Rhaka FirdausNessuna valutazione finora

- ЛексикологіяDocumento2 pagineЛексикологіяQwerty1488 No nameNessuna valutazione finora

- LWB Manual PDFDocumento1 paginaLWB Manual PDFKhalid ZgheirNessuna valutazione finora

- Getting to Yes: How to Negotiate Agreement Without Giving InDa EverandGetting to Yes: How to Negotiate Agreement Without Giving InValutazione: 4 su 5 stelle4/5 (652)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Da EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Valutazione: 4.5 su 5 stelle4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindDa EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindValutazione: 5 su 5 stelle5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Da EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Valutazione: 4.5 su 5 stelle4.5/5 (15)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineDa EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNessuna valutazione finora

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesDa EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNessuna valutazione finora

- The Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingDa EverandThe Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingValutazione: 4.5 su 5 stelle4.5/5 (760)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsDa EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNessuna valutazione finora

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Da EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Valutazione: 4.5 su 5 stelle4.5/5 (5)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookDa EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookValutazione: 5 su 5 stelle5/5 (4)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeDa EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeValutazione: 4 su 5 stelle4/5 (21)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCDa EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCValutazione: 5 su 5 stelle5/5 (1)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsDa EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsValutazione: 5 su 5 stelle5/5 (1)

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetDa EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetValutazione: 4.5 su 5 stelle4.5/5 (14)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessDa EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessValutazione: 4.5 su 5 stelle4.5/5 (28)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceDa EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceValutazione: 4 su 5 stelle4/5 (1)

- Beyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Da EverandBeyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Valutazione: 4.5 su 5 stelle4.5/5 (8)

- Project Control Methods and Best Practices: Achieving Project SuccessDa EverandProject Control Methods and Best Practices: Achieving Project SuccessNessuna valutazione finora

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyDa EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyNessuna valutazione finora

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Da EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Valutazione: 4 su 5 stelle4/5 (33)

- Small Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessDa EverandSmall Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessNessuna valutazione finora

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsDa EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsValutazione: 4 su 5 stelle4/5 (7)

- Contract Negotiation Handbook: Getting the Most Out of Commercial DealsDa EverandContract Negotiation Handbook: Getting the Most Out of Commercial DealsValutazione: 4.5 su 5 stelle4.5/5 (2)

- Financial Accounting For Dummies: 2nd EditionDa EverandFinancial Accounting For Dummies: 2nd EditionValutazione: 5 su 5 stelle5/5 (10)

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookDa EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookNessuna valutazione finora