Potrebbero piacerti anche

- San Miguel Corporation vs. Bartolome Puzon Jr.Documento2 pagineSan Miguel Corporation vs. Bartolome Puzon Jr.RavenFoxNessuna valutazione finora

- SMC Vs PuzonDocumento2 pagineSMC Vs Puzonaldenamell100% (2)

- 112 San Miguel Corp vs. Puzon, GR 167567, Sept 22, 2010Documento2 pagine112 San Miguel Corp vs. Puzon, GR 167567, Sept 22, 2010Alan GultiaNessuna valutazione finora

- San Miguel Corp v. PuzonDocumento2 pagineSan Miguel Corp v. PuzonchecpalawyerNessuna valutazione finora

- San Miguel Corporation Vs PuzonDocumento3 pagineSan Miguel Corporation Vs PuzonMon Che100% (1)

- San Miguel Corp V PuzonDocumento2 pagineSan Miguel Corp V PuzoneieipayadNessuna valutazione finora

- San Miguel Corp v. PuzonDocumento1 paginaSan Miguel Corp v. PuzonPre PacionelaNessuna valutazione finora

- DELIVERY OF POSTDATED CHECKS AND PRESUMPTION OF DEBTDocumento33 pagineDELIVERY OF POSTDATED CHECKS AND PRESUMPTION OF DEBTHoward DinumlaNessuna valutazione finora

- SMC v. PuzonDocumento1 paginaSMC v. PuzonReymart-Vin MagulianoNessuna valutazione finora

- Nego Week 5Documento15 pagineNego Week 5Elyn ApiadoNessuna valutazione finora

- Nego 1Documento9 pagineNego 1Aaron ReyesNessuna valutazione finora

- Nego 3 & 4, DigestedDocumento3 pagineNego 3 & 4, DigestedAubrey CaballeroNessuna valutazione finora

- 2 NEGO Digest and AnalysisDocumento82 pagine2 NEGO Digest and AnalysisJustin EnriquezNessuna valutazione finora

- Liability for dishonored checks and postdated checksDocumento9 pagineLiability for dishonored checks and postdated checksRobinson MojicaNessuna valutazione finora

- B. Completion and Delivery DraftDocumento9 pagineB. Completion and Delivery DraftMikkboy RosetNessuna valutazione finora

- Nego Cases Part 2Documento7 pagineNego Cases Part 2cute_treeena5326Nessuna valutazione finora

- BP Blg. 22 penalizes bouncing checksDocumento64 pagineBP Blg. 22 penalizes bouncing checksMae NiagaraNessuna valutazione finora

- Nego Cases 1st ExamDocumento6 pagineNego Cases 1st ExamAmanda ButtkissNessuna valutazione finora

- 252 Scra 620Documento5 pagine252 Scra 620Jan MadejaNessuna valutazione finora

- San Miguel Corporation v. Puzon Jr.Documento6 pagineSan Miguel Corporation v. Puzon Jr.lovekimsohyun89Nessuna valutazione finora

- CRISOLOGO JOSE V. CA - Accommodation Party 177 SCRA 594 Facts: Gempesaw V. Ca 218 SCRA 682 FactsDocumento7 pagineCRISOLOGO JOSE V. CA - Accommodation Party 177 SCRA 594 Facts: Gempesaw V. Ca 218 SCRA 682 FactsSheila May Panganiban LumardaNessuna valutazione finora

- Digest 2Documento6 pagineDigest 2Van CazNessuna valutazione finora

- DLSU COLLEGE OF LAW COMMERCIAL LAW REVIEWDocumento3 pagineDLSU COLLEGE OF LAW COMMERCIAL LAW REVIEWArjuna Guevara75% (4)

- Doctrines Prudential Bank vs. Intermediate Appellate Court, 216 SCRA 257Documento5 pagineDoctrines Prudential Bank vs. Intermediate Appellate Court, 216 SCRA 257Bechay PallasigueNessuna valutazione finora

- Bouncing Checks Law: June 29, 1979Documento40 pagineBouncing Checks Law: June 29, 1979Anabel Lajara AngelesNessuna valutazione finora

- B11 Allied Banking Corporation V Lim Sio WanDocumento3 pagineB11 Allied Banking Corporation V Lim Sio WanJ CaparasNessuna valutazione finora

- 2013 2014 2015 Q and A Commercial LawDocumento80 pagine2013 2014 2015 Q and A Commercial LawStarr Weigand100% (3)

- Prudential Bank v. IACDocumento2 paginePrudential Bank v. IACEdward Kenneth KungNessuna valutazione finora

- ALL ABOUT CHECKS: COMMERCIAL LAW AND NEGOTIABLE INSTRUMENTSDocumento9 pagineALL ABOUT CHECKS: COMMERCIAL LAW AND NEGOTIABLE INSTRUMENTSCzarina JaneNessuna valutazione finora

- Digested Finals CasesDocumento6 pagineDigested Finals CasesGladden MacedaNessuna valutazione finora

- Nego Case DigestDocumento16 pagineNego Case DigestFatimaNessuna valutazione finora

- (C 01) DBP vs. Sima Wei, 219 SCRA 736, March 9, 1993Documento8 pagine(C 01) DBP vs. Sima Wei, 219 SCRA 736, March 9, 1993JJNessuna valutazione finora

- Dino Vs Judal LootDocumento3 pagineDino Vs Judal LootJohnNicoRamosLuceroNessuna valutazione finora

- Divina Nego OutlineDocumento16 pagineDivina Nego OutlineSamantha KingNessuna valutazione finora

- Intent Determines Ownership of CheckDocumento20 pagineIntent Determines Ownership of CheckJohn SanchezNessuna valutazione finora

- Delivery of Instrument Key to LiabilityDocumento3 pagineDelivery of Instrument Key to LiabilityAquino, JPNessuna valutazione finora

- Wala Ako Mahanap NG Fulltext. Citatiion Lang SiyaDocumento1 paginaWala Ako Mahanap NG Fulltext. Citatiion Lang SiyaVEDIA GENONNessuna valutazione finora

- Nego Jan 7Documento23 pagineNego Jan 7Michelle AsagraNessuna valutazione finora

- PNB V. CA-Material Alteration: 256 SCRA 491Documento5 paginePNB V. CA-Material Alteration: 256 SCRA 491frank japosNessuna valutazione finora

- An Act Penalizing The Making or Drawing and Issuance of A Check Without Sufficient Funds or Credit and For Other PurposesDocumento69 pagineAn Act Penalizing The Making or Drawing and Issuance of A Check Without Sufficient Funds or Credit and For Other PurposesHermay BanarioNessuna valutazione finora

- SC rules no payment without delivery to creditorDocumento28 pagineSC rules no payment without delivery to creditorMariaAyraCelinaBatacan100% (1)

- Dela Victoria v. BurgosDocumento4 pagineDela Victoria v. BurgosMoireeGNessuna valutazione finora

- 43 - Wong v. CaDocumento9 pagine43 - Wong v. CaVia Rhidda ImperialNessuna valutazione finora

- Nil-Midterm Cases CompilationDocumento14 pagineNil-Midterm Cases Compilationjpoy61494Nessuna valutazione finora

- RCBC vs. Hi-Tri Development Corp.Documento3 pagineRCBC vs. Hi-Tri Development Corp.Shiela PilarNessuna valutazione finora

- Bouncing Checks LawDocumento29 pagineBouncing Checks LawRowena Imperial Ramos67% (3)

- J.Y. Brothers vs. SalazarDocumento5 pagineJ.Y. Brothers vs. SalazarChammyNessuna valutazione finora

- PNB v. CA DigestDocumento2 paginePNB v. CA DigestdyosaNessuna valutazione finora

- DB vs Sima WeiDocumento1 paginaDB vs Sima WeiReena Alekssandra AcopNessuna valutazione finora

- Prudential Bank vs. IACDocumento2 paginePrudential Bank vs. IACVanya Klarika NuqueNessuna valutazione finora

- Nil 2Documento10 pagineNil 2KC ToraynoNessuna valutazione finora

- LBP Vs PerezDocumento1 paginaLBP Vs PerezSai RosalesNessuna valutazione finora

- Digest NegoDocumento16 pagineDigest Negoiceiceice023Nessuna valutazione finora

- Invocation of Pledge - Not A Transfer Under Sec.43 of The IBCDocumento5 pagineInvocation of Pledge - Not A Transfer Under Sec.43 of The IBCMin Ah ShinNessuna valutazione finora

- Held:: Trader's Royal v. CADocumento7 pagineHeld:: Trader's Royal v. CAAngela ParadoNessuna valutazione finora

- Crisologo Vs CADocumento19 pagineCrisologo Vs CALance RonquiloNessuna valutazione finora

- Negotiable Instrument (Discharge of Instrument)Documento15 pagineNegotiable Instrument (Discharge of Instrument)Sara Andrea Santiago100% (1)

- NEgo 2nd Exam ReviewerDocumento9 pagineNEgo 2nd Exam ReviewerStacy Shara OtazaNessuna valutazione finora

- Introduction to Negotiable Instruments: As per Indian LawsDa EverandIntroduction to Negotiable Instruments: As per Indian LawsValutazione: 5 su 5 stelle5/5 (1)

- Life, Accident and Health Insurance in the United StatesDa EverandLife, Accident and Health Insurance in the United StatesValutazione: 5 su 5 stelle5/5 (1)

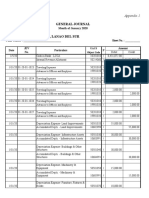

- General Journal: Appendix 1Documento5 pagineGeneral Journal: Appendix 1Mosarah AltNessuna valutazione finora

- 2021 Schedule of Preweek LecturesDocumento1 pagina2021 Schedule of Preweek LecturesMarcky MarionNessuna valutazione finora

- Pretrial Process FlowDocumento1 paginaPretrial Process FlowMosarah AltNessuna valutazione finora

- LectureDocumento25 pagineLectureMarieNessuna valutazione finora

- Rights of Persons Under Custodial InvestigationDocumento13 pagineRights of Persons Under Custodial InvestigationLorebeth EspañaNessuna valutazione finora

- Tax Case Digests CompilationDocumento207 pagineTax Case Digests CompilationFrancis Ray Arbon Filipinas83% (24)

- Tax Case Digests CompilationDocumento207 pagineTax Case Digests CompilationFrancis Ray Arbon Filipinas83% (24)

- Banking and AMLADocumento26 pagineBanking and AMLAMosarah AltNessuna valutazione finora

- Rescission of Contracts & ChecksDocumento1 paginaRescission of Contracts & ChecksMosarah AltNessuna valutazione finora

- Politicsl LawDocumento91 paginePoliticsl LawMosarah AltNessuna valutazione finora

- Civil Law Compilation Bar Q&a 1990-2017 PDFDocumento380 pagineCivil Law Compilation Bar Q&a 1990-2017 PDFReynaldo Yu100% (10)

- Equitable PCI Vs TanDocumento2 pagineEquitable PCI Vs TanMosarah AltNessuna valutazione finora

- People V WagasDocumento1 paginaPeople V WagasMosarah AltNessuna valutazione finora

- Abad Vs PhilcomsatDocumento2 pagineAbad Vs PhilcomsatFiels GamboaNessuna valutazione finora

- Tax DigestsDocumento13 pagineTax DigestsMosarah AltNessuna valutazione finora

- PNB Vs BalmacedaDocumento2 paginePNB Vs BalmacedaMosarah AltNessuna valutazione finora

- Tax ReviewerDocumento45 pagineTax ReviewerMosarah AltNessuna valutazione finora

- Siochi Vs CA 2010 PDFDocumento9 pagineSiochi Vs CA 2010 PDFMosarah AltNessuna valutazione finora

- Equitable Bank Liable for Depositing Crossed Checks in Wrong AccountDocumento1 paginaEquitable Bank Liable for Depositing Crossed Checks in Wrong AccountMosarah AltNessuna valutazione finora

- Salazar Vs JY BrothersDocumento4 pagineSalazar Vs JY BrothersMosarah AltNessuna valutazione finora

- Ching Vs CA 1990Documento6 pagineChing Vs CA 1990Mosarah AltNessuna valutazione finora

- Equitable PCI Vs TanDocumento2 pagineEquitable PCI Vs TanMosarah AltNessuna valutazione finora

- Spec Com BQsDocumento15 pagineSpec Com BQsMosarah AltNessuna valutazione finora

- Cayanan Vs North StarDocumento2 pagineCayanan Vs North StarMosarah AltNessuna valutazione finora

- Ting Ting Pua V Sps TiongDocumento2 pagineTing Ting Pua V Sps TiongeieipayadNessuna valutazione finora

- Politicsl LawDocumento91 paginePoliticsl LawMosarah AltNessuna valutazione finora

- Court Overturns Sale of Family PropertyDocumento7 pagineCourt Overturns Sale of Family PropertyMosarah AltNessuna valutazione finora

- Sps Ros Vs PNB 2011 PDFDocumento8 pagineSps Ros Vs PNB 2011 PDFMosarah AltNessuna valutazione finora

- Mock Trial ScriptDocumento25 pagineMock Trial ScriptRonilo Subaan94% (18)

- Full Research PaperDocumento31 pagineFull Research PaperMeo ĐenNessuna valutazione finora

- Genealogy On June 09-2003Documento25 pagineGenealogy On June 09-2003syedyusufsam92100% (3)

- Human Resource Strategy: Atar Thaung HtetDocumento16 pagineHuman Resource Strategy: Atar Thaung HtetaungnainglattNessuna valutazione finora

- 5 Reasons To Exercise PDFReadingDocumento2 pagine5 Reasons To Exercise PDFReadingMỹ HàNessuna valutazione finora

- A Review of The Book That Made Your World. by Vishal MangalwadiDocumento6 pagineA Review of The Book That Made Your World. by Vishal Mangalwadigaylerob100% (1)

- HRM in InfosysDocumento11 pagineHRM in Infosysguptarahul27550% (4)

- Techno ReadDocumento11 pagineTechno ReadCelrose FernandezNessuna valutazione finora

- Template For Group AssignmentDocumento5 pagineTemplate For Group AssignmentIntan QamariaNessuna valutazione finora

- Semester I Listening Comprehension Test A Good Finder One Day Two Friends Went For A Walk. One of Them Had A Dog. "See HereDocumento13 pagineSemester I Listening Comprehension Test A Good Finder One Day Two Friends Went For A Walk. One of Them Had A Dog. "See HereRichard AndersonNessuna valutazione finora

- The Directors Six SensesDocumento31 pagineThe Directors Six SensesMichael Wiese Productions93% (14)

- Homework #3 - Coursera CorrectedDocumento10 pagineHomework #3 - Coursera CorrectedSaravind67% (3)

- Conversations With Scientists Initiates Brain and Technology UpdateDocumento48 pagineConversations With Scientists Initiates Brain and Technology UpdateJorge Baca LopezNessuna valutazione finora

- 101 Poisons Guide for D&D PlayersDocumento16 pagine101 Poisons Guide for D&D PlayersmighalisNessuna valutazione finora

- CSEC Physics P2 2013 JuneDocumento20 pagineCSEC Physics P2 2013 JuneBill BobNessuna valutazione finora

- Chicago Case InterviewsDocumento20 pagineChicago Case Interviewschakradhar.dandu@gmail.comNessuna valutazione finora

- Practices For Improving The PCBDocumento35 paginePractices For Improving The PCBmwuestNessuna valutazione finora

- Internship ReportDocumento24 pagineInternship ReportFaiz KhanNessuna valutazione finora

- Motor Driving School ReportDocumento39 pagineMotor Driving School ReportAditya Krishnakumar73% (11)

- Sheikh Yusuf Al-Qaradawi A Moderate Voice From TheDocumento14 pagineSheikh Yusuf Al-Qaradawi A Moderate Voice From ThedmpmppNessuna valutazione finora

- Chap 006Documento50 pagineChap 006Martin TrịnhNessuna valutazione finora

- Group Project Assignment Imc407Documento4 pagineGroup Project Assignment Imc407Anonymous nyN7IVBMNessuna valutazione finora

- Central Venous Access Devices (Cvads) andDocumento68 pagineCentral Venous Access Devices (Cvads) andFitri ShabrinaNessuna valutazione finora

- Urology Semiology Guide for Renal Colic & HematuriaDocumento30 pagineUrology Semiology Guide for Renal Colic & HematuriaNikita KumariNessuna valutazione finora

- Psychotherapy Relationships That Work: Volume 1: Evidence-Based Therapist ContributionsDocumento715 paginePsychotherapy Relationships That Work: Volume 1: Evidence-Based Therapist ContributionsErick de Oliveira Tavares100% (5)

- Organizational Development ProcessDocumento1 paginaOrganizational Development ProcessMohit SharmaNessuna valutazione finora

- Women &literatureDocumento54 pagineWomen &literatureAicha ZianeNessuna valutazione finora

- DIASS - Quarter3 - Module1 - Week1 - Pure and Applied Social Sciences - V2Documento18 pagineDIASS - Quarter3 - Module1 - Week1 - Pure and Applied Social Sciences - V2Stephanie Tamayao Lumbo100% (1)

- 477382Documento797 pagine477382PradipGhandiNessuna valutazione finora

- Oracle Induction - Introduction Foot Print and Instances For Perfect ExecutionDocumento11 pagineOracle Induction - Introduction Foot Print and Instances For Perfect Executioneuge_prime2001Nessuna valutazione finora