Potrebbero piacerti anche

- Practical Guides to Testing and Commissioning of Mechanical, Electrical and Plumbing (Mep) InstallationsDa EverandPractical Guides to Testing and Commissioning of Mechanical, Electrical and Plumbing (Mep) InstallationsValutazione: 3.5 su 5 stelle3.5/5 (3)

- Waste to Energy in the Age of the Circular Economy: Compendium of Case Studies and Emerging TechnologiesDa EverandWaste to Energy in the Age of the Circular Economy: Compendium of Case Studies and Emerging TechnologiesValutazione: 5 su 5 stelle5/5 (1)

- Calculation Cost For The Production of Sodium Carbonate: Preparation: Class: SubjectDocumento10 pagineCalculation Cost For The Production of Sodium Carbonate: Preparation: Class: Subjectعبدالمحسن علي ENessuna valutazione finora

- 8.2.1 Fixed Capital Investment (Fci)Documento4 pagine8.2.1 Fixed Capital Investment (Fci)eze josephNessuna valutazione finora

- Financial Feasibility StudyDocumento24 pagineFinancial Feasibility StudyMaria Mikaela PelagioNessuna valutazione finora

- Cost EstimationDocumento8 pagineCost EstimationMuhammad Husnain ArshadNessuna valutazione finora

- Cost Estimation (August23)Documento51 pagineCost Estimation (August23)Lovely Rain100% (2)

- Capital Cost EstimationDocumento55 pagineCapital Cost EstimationMohammad Reza Anghaei100% (1)

- 11@ Costestimation Original at RevisedDocumento15 pagine11@ Costestimation Original at RevisedRajesh KtrNessuna valutazione finora

- Investment That Is To Use The Savings "To Promote The Production of Other Goods, Instead of BeingDocumento10 pagineInvestment That Is To Use The Savings "To Promote The Production of Other Goods, Instead of BeingRalph Carlo EvidenteNessuna valutazione finora

- Last ChapterDocumento18 pagineLast ChapterAqsa chNessuna valutazione finora

- Cost EstimationDocumento7 pagineCost Estimationrubesh_rajaNessuna valutazione finora

- Garrison 8 Ex 5-20, PR 5-25Documento17 pagineGarrison 8 Ex 5-20, PR 5-25Shalini VeluNessuna valutazione finora

- Total Capital Investment SummaryDocumento7 pagineTotal Capital Investment SummaryChewy ChocoNessuna valutazione finora

- Cost EstimationDocumento9 pagineCost EstimationAwais JavaidNessuna valutazione finora

- Alat Deskripsi Jumlah Harga (US$) (Matche, 2014) : Purchased Equipment DeliveryDocumento19 pagineAlat Deskripsi Jumlah Harga (US$) (Matche, 2014) : Purchased Equipment Deliveryikhwanudin husenNessuna valutazione finora

- SuppliesDocumento9 pagineSuppliesEngelbert AntodNessuna valutazione finora

- CHAPTER 5 So FarDocumento6 pagineCHAPTER 5 So FarkudaNessuna valutazione finora

- Equipments MUR (RS) : Cane Preparation and MillingDocumento25 pagineEquipments MUR (RS) : Cane Preparation and MillingManisha DeenaNessuna valutazione finora

- Construction Cost Estimate and The Factors Influencing Its AccuracyDocumento29 pagineConstruction Cost Estimate and The Factors Influencing Its AccuracyAaRichard ManaloNessuna valutazione finora

- Costing and Project EvaluationDocumento11 pagineCosting and Project EvaluationGunalan RNessuna valutazione finora

- Styrene Cost 2520Estimation&EconomicsDocumento8 pagineStyrene Cost 2520Estimation&EconomicsShravan BehalNessuna valutazione finora

- Capital Cost EstimationDocumento55 pagineCapital Cost EstimationKentDemeterioNessuna valutazione finora

- Lecture 6fDocumento30 pagineLecture 6fhiteshNessuna valutazione finora

- Capital Cost Estimation Dr. Rakesh KumarDocumento33 pagineCapital Cost Estimation Dr. Rakesh KumarDEV RAJNessuna valutazione finora

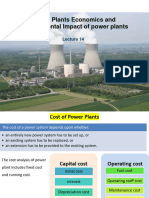

- Lec - 14 PP - Economics and Environmental Impact of PPsDocumento42 pagineLec - 14 PP - Economics and Environmental Impact of PPsLog XNessuna valutazione finora

- Trade-Off Analysis: Technological Institute of TheDocumento41 pagineTrade-Off Analysis: Technological Institute of TheJared OcampoNessuna valutazione finora

- Ethylene 2520oxide Cost 2520Estimation&EconomicsDocumento14 pagineEthylene 2520oxide Cost 2520Estimation&EconomicsBelema Thomson100% (1)

- Che - Engg Economics (Project)Documento28 pagineChe - Engg Economics (Project)Ahmad SaleemNessuna valutazione finora

- Chapter IvDocumento39 pagineChapter Ivdainty mojaresNessuna valutazione finora

- Hydrodealkylation Plant Economic AnalysisDocumento5 pagineHydrodealkylation Plant Economic AnalysisVinayak PathakNessuna valutazione finora

- Cost Estimation of Reactor - 060Documento36 pagineCost Estimation of Reactor - 060Muhammad UsamaNessuna valutazione finora

- Ethylene Oxide ProductionDocumento22 pagineEthylene Oxide Productionsaleem razaNessuna valutazione finora

- Cash Flow Estimation Models: Estimating Relationships and ProblemsDocumento30 pagineCash Flow Estimation Models: Estimating Relationships and ProblemsSenthil RNessuna valutazione finora

- Cost EstDocumento6 pagineCost Estchaitanya_scribdNessuna valutazione finora

- Cost Accounting AssignmentDocumento6 pagineCost Accounting AssignmentRamalu Dinesh ReddyNessuna valutazione finora

- Cost Estimation PDFDocumento16 pagineCost Estimation PDFemadsabriNessuna valutazione finora

- 10.1.2 Costing Data: Chapter 10 - Integrated Cost-Based Design and Operation 457Documento6 pagine10.1.2 Costing Data: Chapter 10 - Integrated Cost-Based Design and Operation 457WONG TS75% (4)

- Cost Estimation - Aadarsh ShuklaDocumento6 pagineCost Estimation - Aadarsh Shuklavidit Singh100% (1)

- Economic Evaluation Report: 1. EXECUTIVE SUMMARY (2021 Prices)Documento10 pagineEconomic Evaluation Report: 1. EXECUTIVE SUMMARY (2021 Prices)Adrián GpNessuna valutazione finora

- C C M Constant Depending On Equipment Type F F F: 2. Economics and Cost Estimation: 2.1. Battery Limits InvestmentDocumento5 pagineC C M Constant Depending On Equipment Type F F F: 2. Economics and Cost Estimation: 2.1. Battery Limits Investmentshuraj k.c.Nessuna valutazione finora

- EconomicsDocumento177 pagineEconomicsOscar CamposNessuna valutazione finora

- Feasibility Study For An Investment of An Industrial Plant Evaluating Red Mud by An Innovating Method. A Case StudyDocumento8 pagineFeasibility Study For An Investment of An Industrial Plant Evaluating Red Mud by An Innovating Method. A Case StudyAnele HadebeNessuna valutazione finora

- 2.0 Total Cost Estimation 2.1 Bare Module / Guthrie Method: P BM BMDocumento9 pagine2.0 Total Cost Estimation 2.1 Bare Module / Guthrie Method: P BM BMFathihah AnuarNessuna valutazione finora

- Costing With DescriptionDocumento9 pagineCosting With DescriptionTal PeraltaNessuna valutazione finora

- Land Acquisition Cost 579,549,000 PHP: Cost Per SQ.MDocumento21 pagineLand Acquisition Cost 579,549,000 PHP: Cost Per SQ.MArnold DominguezNessuna valutazione finora

- Report of Equipment DesignDocumento10 pagineReport of Equipment DesignHussein Al HabebNessuna valutazione finora

- Chapter 9Documento7 pagineChapter 9Gospel EmeaNessuna valutazione finora

- Cost and Management Accounting 01 - Class NotesDocumento114 pagineCost and Management Accounting 01 - Class NotessaurabhNessuna valutazione finora

- Prelim DataDocumento10 paginePrelim DatajerrenjgNessuna valutazione finora

- B. Land Cost: Description Price (RP) Area (m2) Total Price (RP)Documento31 pagineB. Land Cost: Description Price (RP) Area (m2) Total Price (RP)dimasNessuna valutazione finora

- Preliminary Cost Estimation: 13.1. Cost of Major EquipmentsDocumento4 paginePreliminary Cost Estimation: 13.1. Cost of Major EquipmentsVenu AngirekulaNessuna valutazione finora

- Report EconomicoDocumento10 pagineReport EconomicoMartin Torres RuedaNessuna valutazione finora

- Economic ReportDocumento9 pagineEconomic ReportYeeXuan TenNessuna valutazione finora

- 4) Profitability AnalysisDocumento39 pagine4) Profitability AnalysisNurul A'ashikhinNessuna valutazione finora

- Toluene Cost Estimation&EconomicsDocumento10 pagineToluene Cost Estimation&EconomicssapooknikNessuna valutazione finora

- CMA CU - Chap5Documento29 pagineCMA CU - Chap5TAMANNANessuna valutazione finora

- Capcost Wartsila 85MWDocumento5 pagineCapcost Wartsila 85MWJosé NunesNessuna valutazione finora

- Energy Management Principles: Applications, Benefits, SavingsDa EverandEnergy Management Principles: Applications, Benefits, SavingsValutazione: 4.5 su 5 stelle4.5/5 (3)

- Super Duper Final 3Documento40 pagineSuper Duper Final 3Kim AridaNessuna valutazione finora

- HPHTDocumento3 pagineHPHTKim AridaNessuna valutazione finora

- MoistureDocumento1 paginaMoistureKim AridaNessuna valutazione finora

- AppendixDocumento35 pagineAppendixKim AridaNessuna valutazione finora

- BibliographyDocumento2 pagineBibliographyKim AridaNessuna valutazione finora

- Super Final Front Page PDFDocumento1 paginaSuper Final Front Page PDFKim AridaNessuna valutazione finora

- Chapter IIIDocumento22 pagineChapter IIIKim AridaNessuna valutazione finora

- Table of Contents FinalDocumento13 pagineTable of Contents FinalKim AridaNessuna valutazione finora

- Super Final TocDocumento4 pagineSuper Final TocKim AridaNessuna valutazione finora

- Chapter IIDocumento2 pagineChapter IIKim AridaNessuna valutazione finora

- Chapter IDocumento9 pagineChapter IKim AridaNessuna valutazione finora

- Gantt ChartDocumento4 pagineGantt ChartKim AridaNessuna valutazione finora

- Chapter VDocumento8 pagineChapter VKim AridaNessuna valutazione finora

- Chapter IDocumento9 pagineChapter IKim AridaNessuna valutazione finora

- Front PageDocumento1 paginaFront PageKim AridaNessuna valutazione finora

- Design and Development of A Mixer For The Evaluation of Best Alternative Retarder Cement Additives From Agricultural WastesDocumento2 pagineDesign and Development of A Mixer For The Evaluation of Best Alternative Retarder Cement Additives From Agricultural WastesKim AridaNessuna valutazione finora

- Bibliography FinalDocumento3 pagineBibliography FinalKim AridaNessuna valutazione finora

- Summary of ThesisDocumento9 pagineSummary of ThesisKim AridaNessuna valutazione finora

- Examiners Report - January 2008 All Units PDFDocumento0 pagineExaminers Report - January 2008 All Units PDFbtjajadiNessuna valutazione finora

- Design and Development of A Mixer For The Evaluation of Best Alternative Retarder Cement Additives From Agricultural WastesDocumento2 pagineDesign and Development of A Mixer For The Evaluation of Best Alternative Retarder Cement Additives From Agricultural WastesKim AridaNessuna valutazione finora

- Cement Additive Thesis BrochureDocumento2 pagineCement Additive Thesis BrochureKim AridaNessuna valutazione finora

- Design and Development of A Mixer For The Evaluation of Best Alternative Retarder Cement Additive From Agricultural WastesDocumento87 pagineDesign and Development of A Mixer For The Evaluation of Best Alternative Retarder Cement Additive From Agricultural WastesKim Arida100% (1)

- QUIZ1 - Finacc3Documento4 pagineQUIZ1 - Finacc3Jonnie RegalaNessuna valutazione finora

- Herbal GutkaDocumento8 pagineHerbal GutkaKamlesh Rajput0% (1)

- Bizualem BeleteDocumento101 pagineBizualem BeleteAnonymous qAegy6G100% (1)

- Question-1 I) : SKANS School of Accountancy Principles of Taxation Mid Term ExamDocumento4 pagineQuestion-1 I) : SKANS School of Accountancy Principles of Taxation Mid Term ExamMuhammad ArslanNessuna valutazione finora

- Migrating Fixed Assets Into SAPDocumento8 pagineMigrating Fixed Assets Into SAPAndreea OlteanuNessuna valutazione finora

- Acc 106Documento66 pagineAcc 106ananimus ananimusNessuna valutazione finora

- Significant Accounting Policies of IBMDocumento19 pagineSignificant Accounting Policies of IBMvivek799Nessuna valutazione finora

- Financial StatementsDocumento27 pagineFinancial StatementsIrish Castillo100% (1)

- QRB 501 Final Exam Study GuideDocumento8 pagineQRB 501 Final Exam Study GuidesidrazeekhanNessuna valutazione finora

- SS 08 Quiz 1Documento45 pagineSS 08 Quiz 1Van Le HaNessuna valutazione finora

- QuestionsDocumento5 pagineQuestionsYonas100% (1)

- XLS092 XLS EnG Tire City RaghuDocumento48 pagineXLS092 XLS EnG Tire City RaghuNaveen KumarNessuna valutazione finora

- Dow Chemical Company Annual Report - 1947Documento17 pagineDow Chemical Company Annual Report - 1947fresnoNessuna valutazione finora

- Example:: Construction Methods .. Ch.-2-Factors Affecting The Selection of Construction EquipmentDocumento2 pagineExample:: Construction Methods .. Ch.-2-Factors Affecting The Selection of Construction EquipmentAimen AhmedNessuna valutazione finora

- CH 19Documento12 pagineCH 19Felicia Carissa0% (1)

- Relevant Cost-Lecture NotesDocumento10 pagineRelevant Cost-Lecture NotesLee Jap OyNessuna valutazione finora

- Acc/563 Week 11 Final Exam QuizDocumento68 pagineAcc/563 Week 11 Final Exam QuizgoodNessuna valutazione finora

- Aud Application 2 - Handout 1 PPE Acquisition (UST)Documento3 pagineAud Application 2 - Handout 1 PPE Acquisition (UST)RNessuna valutazione finora

- Annual Report of IOCL 90Documento1 paginaAnnual Report of IOCL 90Nikunj ParmarNessuna valutazione finora

- Accounting For LeassesDocumento122 pagineAccounting For LeassesIntan ParamithaNessuna valutazione finora

- Fam Cia-1 Sec-BDocumento7 pagineFam Cia-1 Sec-BswathiNessuna valutazione finora

- 04 - Chapter 4 Cash Flow Financial PlanningDocumento68 pagine04 - Chapter 4 Cash Flow Financial Planninghunkie71% (7)

- Financial 1004Documento6 pagineFinancial 1004May Anne BarlisNessuna valutazione finora

- Abm 12 Fabm2 q1 Clas1 Elements of Sci v8 - Rhea Ann NavillaDocumento13 pagineAbm 12 Fabm2 q1 Clas1 Elements of Sci v8 - Rhea Ann NavillaKim Yessamin MadarcosNessuna valutazione finora

- Bharat Electronics Limited AssignmentDocumento10 pagineBharat Electronics Limited AssignmentAnusree SasidharanNessuna valutazione finora

- Solution Chapter 11Documento38 pagineSolution Chapter 11Anonymous CuUAaRSNNessuna valutazione finora

- A Practical Guide To GIS in Asset Management PDFDocumento12 pagineA Practical Guide To GIS in Asset Management PDFOmar Lobo GuillenNessuna valutazione finora

- Mini Case 4-Investment Property (Student) - A192Documento2 pagineMini Case 4-Investment Property (Student) - A192Chee Mei JeeNessuna valutazione finora

- Tally Ledgers and Groups ListDocumento12 pagineTally Ledgers and Groups ListDeepak GoswamiNessuna valutazione finora

- Slovakia 14Documento11 pagineSlovakia 14Edvin MusiNessuna valutazione finora