Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Chapter 3 Income Taxation Tabag 2019 Sol ManDocumento21 pagineChapter 3 Income Taxation Tabag 2019 Sol ManFMM50% (2)

- MS 55Documento10 pagineMS 55AnjnaKandariNessuna valutazione finora

- Bes 121 AssignmentDocumento10 pagineBes 121 AssignmentAnjnaKandariNessuna valutazione finora

- Bes 123 AssignmentDocumento10 pagineBes 123 AssignmentAnjnaKandariNessuna valutazione finora

- Ms 11Documento8 pagineMs 11AnjnaKandariNessuna valutazione finora

- MS 27Documento9 pagineMS 27AnjnaKandariNessuna valutazione finora

- MS 29Documento10 pagineMS 29AnjnaKandariNessuna valutazione finora

- Ms 91Documento8 pagineMs 91AnjnaKandariNessuna valutazione finora

- MS 44Documento9 pagineMS 44AnjnaKandariNessuna valutazione finora

- Assignment Course Code: MS - 56 Course Title: Materials Management Assignment Code: MS-56 /TMA/SEM - II/2020 Coverage: All BlocksDocumento6 pagineAssignment Course Code: MS - 56 Course Title: Materials Management Assignment Code: MS-56 /TMA/SEM - II/2020 Coverage: All BlocksAnjnaKandariNessuna valutazione finora

- MS 57Documento9 pagineMS 57AnjnaKandariNessuna valutazione finora

- MS 10Documento10 pagineMS 10AnjnaKandariNessuna valutazione finora

- MS 07Documento8 pagineMS 07AnjnaKandariNessuna valutazione finora

- MS 09Documento12 pagineMS 09AnjnaKandariNessuna valutazione finora

- MS 45Documento8 pagineMS 45AnjnaKandariNessuna valutazione finora

- Assignment Reference Material BPCE - 017 Introduction To Counselling PsychologyDocumento8 pagineAssignment Reference Material BPCE - 017 Introduction To Counselling PsychologyAnjnaKandariNessuna valutazione finora

- Assignment Reference Material (2020-21) I.B.O.-05 International Marketing LogisticsDocumento10 pagineAssignment Reference Material (2020-21) I.B.O.-05 International Marketing LogisticsAnjnaKandariNessuna valutazione finora

- Assignment Reference Material (2020-219 BPCE-018 NeuropsychologyDocumento11 pagineAssignment Reference Material (2020-219 BPCE-018 NeuropsychologyAnjnaKandariNessuna valutazione finora

- Assignment Reference Material (2020-21) I.B.O.-03 India's Foreign TradeDocumento8 pagineAssignment Reference Material (2020-21) I.B.O.-03 India's Foreign TradeAnjnaKandariNessuna valutazione finora

- Assignment Reference Material (2020-21) BPC - 002 Developmental PsychologyDocumento9 pagineAssignment Reference Material (2020-21) BPC - 002 Developmental PsychologyAnjnaKandariNessuna valutazione finora

- Assignment Reference Material (2020-21) I.B.O.-06 International Business FinanceDocumento6 pagineAssignment Reference Material (2020-21) I.B.O.-06 International Business FinanceAnjnaKandariNessuna valutazione finora

- Assignment Reference Material (2020-21) BPCE - 019 Environmental PsychologyDocumento10 pagineAssignment Reference Material (2020-21) BPCE - 019 Environmental PsychologyAnjnaKandariNessuna valutazione finora

- Assignment Reference Material (2020-21) BPCE - 011 School PsychologyDocumento10 pagineAssignment Reference Material (2020-21) BPCE - 011 School PsychologyAnjnaKandariNessuna valutazione finora

- Assignment Reference Material (2020-21) BPC - 001 General PsychologyDocumento9 pagineAssignment Reference Material (2020-21) BPC - 001 General PsychologyAnjnaKandariNessuna valutazione finora

- Assignment Reference Material (2020-21) BPCE-13 Motivation and EmotionDocumento10 pagineAssignment Reference Material (2020-21) BPCE-13 Motivation and EmotionAnjnaKandariNessuna valutazione finora

- Assignment Reference Material (2020-21) BPCE - 015 Industrial and Organisational PsychologyDocumento10 pagineAssignment Reference Material (2020-21) BPCE - 015 Industrial and Organisational PsychologyAnjnaKandari100% (1)

- Chapter - 1 Computation of Tax LiabilityDocumento6 pagineChapter - 1 Computation of Tax LiabilityNitin RajNessuna valutazione finora

- 2019 Ust Pre Week Taxation LawDocumento36 pagine2019 Ust Pre Week Taxation Lawdublin80% (20)

- 01 - ACCLAW Case DigestDocumento45 pagine01 - ACCLAW Case DigestNatalie SerranoNessuna valutazione finora

- Taxation Topic 3Documento29 pagineTaxation Topic 3Philip Gwadenya100% (2)

- Taxation Bar Q&A 1994-2006Documento86 pagineTaxation Bar Q&A 1994-2006LR FNessuna valutazione finora

- KPMG - Fiji COVID-19 Response Budget Newsletter1859921916929410238Documento2 pagineKPMG - Fiji COVID-19 Response Budget Newsletter1859921916929410238Louchrisha HussainNessuna valutazione finora

- Business Organization I Cases - Digest (3manresa - 12)Documento172 pagineBusiness Organization I Cases - Digest (3manresa - 12)Izza GonzalesNessuna valutazione finora

- Instructions For Filling The Tax Calculator For Financial Year 2017-18Documento2 pagineInstructions For Filling The Tax Calculator For Financial Year 2017-18SubramanyaNessuna valutazione finora

- Summary of Thailand-Tax-Guide and LawsDocumento34 pagineSummary of Thailand-Tax-Guide and LawsPranav BhatNessuna valutazione finora

- 1700 Job AidDocumento12 pagine1700 Job AidAljohn Stephen Dela cruzNessuna valutazione finora

- Income Tax Procedure PracticeU 12345 RB PDFDocumento41 pagineIncome Tax Procedure PracticeU 12345 RB PDFBrindha BabuNessuna valutazione finora

- Purpose and Scope of TaxationDocumento6 paginePurpose and Scope of TaxationMaria ThereseNessuna valutazione finora

- Hilado V Collector of Internal RevenueDocumento2 pagineHilado V Collector of Internal RevenueErnest Levanza83% (6)

- Rmo 34-04Documento20 pagineRmo 34-04nathalie velasquezNessuna valutazione finora

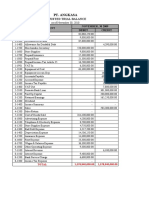

- Kerja Kelompok PT Angkasa BDocumento28 pagineKerja Kelompok PT Angkasa BElisa EndrianiiNessuna valutazione finora

- TaxDocumento18 pagineTaxPatrickBeronaNessuna valutazione finora

- Taxation Chap 1 2 Tabag GarciaDocumento4 pagineTaxation Chap 1 2 Tabag GarciaZedie Leigh VioletaNessuna valutazione finora

- Basic Terms MCQDocumento40 pagineBasic Terms MCQSarvar PathanNessuna valutazione finora

- Fisher Vs TrinidadDocumento11 pagineFisher Vs TrinidadJeff GomezNessuna valutazione finora

- Tax Planning CasesDocumento68 pagineTax Planning CasesHomework PingNessuna valutazione finora

- Income Taxation T or F ReviewerDocumento13 pagineIncome Taxation T or F ReviewerZalaR0cksNessuna valutazione finora

- Factors Influencing Tax EvasionDocumento59 pagineFactors Influencing Tax EvasionLyka Trisha Uy SagoliliNessuna valutazione finora

- Petitioner,: Republic of The Philippine Court of Tax Appeal Quezon ITYDocumento32 paginePetitioner,: Republic of The Philippine Court of Tax Appeal Quezon ITYMaria Diory RabajanteNessuna valutazione finora

- What Are The Kinds of TaxpayersDocumento4 pagineWhat Are The Kinds of TaxpayersALee Bud100% (1)

- Tax 3Documento15 pagineTax 3Mark Lawrence YusiNessuna valutazione finora

- 05 Bir - SMRDocumento1 pagina05 Bir - SMRMelany Trazo Calvez-EvangelistaNessuna valutazione finora

- Paper7 Set2 SolutionDocumento17 paginePaper7 Set2 SolutionMayuri KolheNessuna valutazione finora

- Items of Gross Income Subject To RegularDocumento2 pagineItems of Gross Income Subject To Regularace zeroNessuna valutazione finora

- Pre - Lim Business TaxDocumento7 paginePre - Lim Business TaxRenalyn ParasNessuna valutazione finora