Potrebbero piacerti anche

- Chapter 9.handling Finacial ProceduresDocumento35 pagineChapter 9.handling Finacial ProceduresAngelica SamaniegoNessuna valutazione finora

- VouchersDocumento9 pagineVouchersRaviSankar100% (2)

- Cohen Letter To JudgeDocumento9 pagineCohen Letter To Judgepaul weichNessuna valutazione finora

- Citizenship-Immigration Status 2016Documento1 paginaCitizenship-Immigration Status 2016rendaoNessuna valutazione finora

- Nmims Sec A Test No 1Documento6 pagineNmims Sec A Test No 1ROHAN DESAI100% (1)

- Money and Monetarism: Unit HighlightsDocumento18 pagineMoney and Monetarism: Unit HighlightsprabodhNessuna valutazione finora

- Double EntryDocumento14 pagineDouble EntryHuleshwar Kumar Singh100% (1)

- Master AccountDocumento3 pagineMaster AccountkewasutaNessuna valutazione finora

- Ecs FormDocumento1 paginaEcs FormGAJAB SINGNNessuna valutazione finora

- ODonnell Monitor Second Report v. 31Documento101 pagineODonnell Monitor Second Report v. 31The TexanNessuna valutazione finora

- Request For Taxpayer Identification Number and CertificationDocumento1 paginaRequest For Taxpayer Identification Number and CertificationJude Thomas SmithNessuna valutazione finora

- General Banking and Foreign Exchange Activities of IFIC Bank LTDDocumento18 pagineGeneral Banking and Foreign Exchange Activities of IFIC Bank LTDsuviraiubNessuna valutazione finora

- Murgia V Municipal CourtDocumento12 pagineMurgia V Municipal CourtKate ChatfieldNessuna valutazione finora

- Macn-R000154ds David F. Sandbach Attorney at LawDocumento8 pagineMacn-R000154ds David F. Sandbach Attorney at LawDiane Peeples ElNessuna valutazione finora

- En 05 10096Documento2 pagineEn 05 10096Simón HerreraNessuna valutazione finora

- Fraud Asuransi KesehatanDocumento9 pagineFraud Asuransi KesehatanOlivia JosianaNessuna valutazione finora

- Affidavit of HardshipDocumento3 pagineAffidavit of HardshipSolomon ReynoldsNessuna valutazione finora

- Investors Sue Ligand Pharmaceuticals (NASDAQ: LGND) For $3.8 BillionDocumento28 pagineInvestors Sue Ligand Pharmaceuticals (NASDAQ: LGND) For $3.8 Billionamvona100% (1)

- Uthorization For Elease of Nformation: Financial Management ServiceDocumento1 paginaUthorization For Elease of Nformation: Financial Management ServiceortneraaronNessuna valutazione finora

- 150813bock AmicusbriefDocumento46 pagine150813bock AmicusbriefSamuelNessuna valutazione finora

- 3rd Sem B, L&o 1.docx 2Documento85 pagine3rd Sem B, L&o 1.docx 2shree harsha cNessuna valutazione finora

- Cash MemoDocumento6 pagineCash MemoPatricia Isabelle GutierrezNessuna valutazione finora

- BanksandbankingDocumento6 pagineBanksandbankingRene SmithNessuna valutazione finora

- Ken Strange IRS CompaintDocumento2 pagineKen Strange IRS CompaintReform AustinNessuna valutazione finora

- Policy Guidelines On Fair Practice Code - July 2016 PDFDocumento7 paginePolicy Guidelines On Fair Practice Code - July 2016 PDFDeepNessuna valutazione finora

- Cash and BankDocumento19 pagineCash and BankJatinNessuna valutazione finora

- AFFIDAVITDocumento14 pagineAFFIDAVITLeorebelle RacelisNessuna valutazione finora

- Wachovia (Wells Fargo) FHA Sabat Modification Scam ComplaintDocumento28 pagineWachovia (Wells Fargo) FHA Sabat Modification Scam ComplaintForeclosure FraudNessuna valutazione finora

- DBCC DMV CommandsDocumento6 pagineDBCC DMV Commandsadchy7Nessuna valutazione finora

- Claims Form - Government Claims Program - Office of Risk and Insurance ManagementDocumento5 pagineClaims Form - Government Claims Program - Office of Risk and Insurance ManagementCapital Public RadioNessuna valutazione finora

- MSB Registration From FinCENDocumento1 paginaMSB Registration From FinCENCoin FireNessuna valutazione finora

- Rights of Accused PersonsDocumento4 pagineRights of Accused PersonsSanni KumarNessuna valutazione finora

- Free Consent - FRAUD: Under Indian Contract Act 1872Documento2 pagineFree Consent - FRAUD: Under Indian Contract Act 1872SEKANISH KALPANA ANessuna valutazione finora

- The Parts of A CheckDocumento2 pagineThe Parts of A Checkjamaica dingleNessuna valutazione finora

- Sav 1048Documento7 pagineSav 1048Michael100% (2)

- Class Action Complaint: Bandago v. Mercedes-Benz USADocumento35 pagineClass Action Complaint: Bandago v. Mercedes-Benz USAChrisCassidyNessuna valutazione finora

- Study Material For This LectureDocumento12 pagineStudy Material For This Lectureosaie100% (1)

- Instructions To SheriffDocumento1 paginaInstructions To SheriffTramiNgoNessuna valutazione finora

- Accruals and AdjustmentsDocumento14 pagineAccruals and AdjustmentsNepal Bishal Shrestha100% (1)

- Feasibility Study Final 1Documento40 pagineFeasibility Study Final 1Andrea Atonducan100% (1)

- Bureau of The Fiscal ServiceDocumento3 pagineBureau of The Fiscal Servicebeyy100% (1)

- Non Taxable IncomeDocumento4 pagineNon Taxable IncomeSesshomaruHimuraNessuna valutazione finora

- Request For Transcript of Tax ReturnDocumento2 pagineRequest For Transcript of Tax ReturnBilboDBagginsNessuna valutazione finora

- Credit Card Chargeback ReversalsDocumento2 pagineCredit Card Chargeback ReversalsCursedDiamondsNessuna valutazione finora

- Gardendale Probation LawsuitDocumento50 pagineGardendale Probation LawsuitMike CasonNessuna valutazione finora

- Annual Clean Note CertificateDocumento1 paginaAnnual Clean Note CertificateHaniyaHanifNessuna valutazione finora

- How To Open Letter of CreditDocumento2 pagineHow To Open Letter of Credit✬ SHANZA MALIK ✬Nessuna valutazione finora

- An Aid SuiteDocumento4 pagineAn Aid SuiteNaamir Wahiyd BeyNessuna valutazione finora

- Fdcpa HandoutsDocumento7 pagineFdcpa HandoutsStephen MonaghanNessuna valutazione finora

- Filed & Entered: Clerk U.S. Bankruptcy Court Central District of California by Deputy ClerkDocumento7 pagineFiled & Entered: Clerk U.S. Bankruptcy Court Central District of California by Deputy ClerkChapter 11 Dockets100% (1)

- Deposit and Borrowing OperationsDocumento5 pagineDeposit and Borrowing OperationsCinNessuna valutazione finora

- BankofAmericaCorporation 10KDocumento241 pagineBankofAmericaCorporation 10KParul MitterNessuna valutazione finora

- Today 10.lenderDocumento9 pagineToday 10.lenderGamaya EmmanuelNessuna valutazione finora

- Policyloanapplicationform PDFDocumento2 paginePolicyloanapplicationform PDFEdgar Compala100% (1)

- Bill of Lading (B/L) : What Is Bill of Exchange and State Its Essentials ?Documento4 pagineBill of Lading (B/L) : What Is Bill of Exchange and State Its Essentials ?Dhananjay KumarNessuna valutazione finora

- U S B C: Nited Tates Ankruptcy OurtDocumento4 pagineU S B C: Nited Tates Ankruptcy OurtChapter 11 DocketsNessuna valutazione finora

- Us Loan AuditorsDocumento28 pagineUs Loan Auditorsdean6265Nessuna valutazione finora

- The Numbers Refer To Section A-B Sheet, Section A DetailDocumento41 pagineThe Numbers Refer To Section A-B Sheet, Section A DetailenyonyoziNessuna valutazione finora

- Chapter 2 - Basic Documents and TransactionsDocumento33 pagineChapter 2 - Basic Documents and Transactionsmarissa casareno almuete100% (1)

- Abm Basic DocumentsDocumento6 pagineAbm Basic DocumentsAmimah Balt GuroNessuna valutazione finora

- PopDocumento13 paginePopMark AndrewNessuna valutazione finora

- Claire O. Obseñares: ResumeDocumento3 pagineClaire O. Obseñares: ResumeMark AndrewNessuna valutazione finora

- Bstellar RevolutionDocumento24 pagineBstellar RevolutionTrisha MagtibayNessuna valutazione finora

- Chapter Ten: Critical Reading: RecognizeDocumento17 pagineChapter Ten: Critical Reading: RecognizeMark AndrewNessuna valutazione finora

- Final Defense ScriptDocumento4 pagineFinal Defense Scriptandeng100% (1)

- Corporate Treasury ManagementDocumento9 pagineCorporate Treasury Managementdhanush_sophieNessuna valutazione finora

- ADVANCED FA Chap IIIDocumento7 pagineADVANCED FA Chap IIIFasiko Asmaro100% (1)

- Opportunity Cost in Finance and AccountingDocumento8 pagineOpportunity Cost in Finance and AccountingMary Grace GonzalesNessuna valutazione finora

- KSIE OsDocumento73 pagineKSIE OsAnush PrasannanNessuna valutazione finora

- Allux Indo 8301385679Documento2 pagineAllux Indo 8301385679Ardi dutaNessuna valutazione finora

- Fema Add CHDocumento54 pagineFema Add CHMukesh DholakiaNessuna valutazione finora

- Epc and Ppa ContractsDocumento12 pagineEpc and Ppa ContractsCOT Management Training InsituteNessuna valutazione finora

- Documentary Stamp TaxDocumento120 pagineDocumentary Stamp Taxnegotiator50% (2)

- Accounts PracticleDocumento75 pagineAccounts PracticleMITESHKADAKIA60% (5)

- Fac4863 104 - 2020 - 0 - BDocumento93 pagineFac4863 104 - 2020 - 0 - BNISSIBETINessuna valutazione finora

- Investment Environment and Investment Management Process-1Documento1 paginaInvestment Environment and Investment Management Process-1CalvinsNessuna valutazione finora

- POP DetailsDocumento15 paginePOP DetailsJitender KumarNessuna valutazione finora

- 6th Sem BComDocumento3 pagine6th Sem BComRichu ksNessuna valutazione finora

- BILTIR Fact Sheet 2019 PDFDocumento2 pagineBILTIR Fact Sheet 2019 PDFBernewsAdminNessuna valutazione finora

- Asset Declaration RahimaDocumento3 pagineAsset Declaration RahimaMukhlesur RahmanNessuna valutazione finora

- Solution: Econ 2123, Fall 2018, Problem Set 1Documento6 pagineSolution: Econ 2123, Fall 2018, Problem Set 1Pak Ho100% (1)

- Republic Act No. 7279Documento25 pagineRepublic Act No. 7279Sharmen Dizon GalleneroNessuna valutazione finora

- Why Investors Must Wring Out HIGH Beta From Portfolio?Documento4 pagineWhy Investors Must Wring Out HIGH Beta From Portfolio?Yogesh V GabaniNessuna valutazione finora

- The Last Mile Playbook For FinTech On Polygon 2Documento31 pagineThe Last Mile Playbook For FinTech On Polygon 2alexNessuna valutazione finora

- 201FIN Tutorial 3 Financial Statements Analysis and RatiosDocumento3 pagine201FIN Tutorial 3 Financial Statements Analysis and RatiosAbdulaziz HNessuna valutazione finora

- Mananquil, Julieta P. - Jeths JefrenDocumento12 pagineMananquil, Julieta P. - Jeths JefrenMarissa Bucad GomezNessuna valutazione finora

- EricssonDocumento47 pagineEricssonRafa BorgesNessuna valutazione finora

- 26nov2022 - 30jan2023Documento12 pagine26nov2022 - 30jan2023Srishti SharmaNessuna valutazione finora

- Chapter 9, 11: Assignment Questions (Ch9) P9-16 (Documento2 pagineChapter 9, 11: Assignment Questions (Ch9) P9-16 (Cheung HarveyNessuna valutazione finora

- Auditing Problem Assignment Lyeca JoieDocumento12 pagineAuditing Problem Assignment Lyeca JoieEsse ValdezNessuna valutazione finora

- Model Asset and Liability Affidavit D. VDocumento12 pagineModel Asset and Liability Affidavit D. VsavagecommentorNessuna valutazione finora

- Statute of Limitations For Collecting A DebtDocumento2 pagineStatute of Limitations For Collecting A DebtmikotanakaNessuna valutazione finora

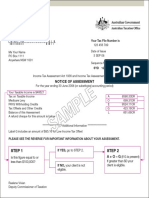

- Step 1 Step 2: Notice of AssessmentDocumento1 paginaStep 1 Step 2: Notice of Assessmentabinash manandharNessuna valutazione finora

- Day CareDocumento21 pagineDay CareSarfraz AliNessuna valutazione finora

- World Geography Puzzles: Countries of the World, Grades 5 - 12Da EverandWorld Geography Puzzles: Countries of the World, Grades 5 - 12Nessuna valutazione finora

- Teaching English: How to Teach English as a Second LanguageDa EverandTeaching English: How to Teach English as a Second LanguageNessuna valutazione finora

- World Geography - Time & Climate Zones - Latitude, Longitude, Tropics, Meridian and More | Geography for Kids | 5th Grade Social StudiesDa EverandWorld Geography - Time & Climate Zones - Latitude, Longitude, Tropics, Meridian and More | Geography for Kids | 5th Grade Social StudiesValutazione: 5 su 5 stelle5/5 (2)

- The Power of Our Supreme Court: How Supreme Court Cases Shape DemocracyDa EverandThe Power of Our Supreme Court: How Supreme Court Cases Shape DemocracyValutazione: 5 su 5 stelle5/5 (2)

- Successful Strategies for Teaching World GeographyDa EverandSuccessful Strategies for Teaching World GeographyValutazione: 5 su 5 stelle5/5 (1)

- World Geography Quick Starts WorkbookDa EverandWorld Geography Quick Starts WorkbookValutazione: 4 su 5 stelle4/5 (1)

- Archaeology for Kids - Australia - Top Archaeological Dig Sites and Discoveries | Guide on Archaeological Artifacts | 5th Grade Social StudiesDa EverandArchaeology for Kids - Australia - Top Archaeological Dig Sites and Discoveries | Guide on Archaeological Artifacts | 5th Grade Social StudiesNessuna valutazione finora