Potrebbero piacerti anche

- Data Section: Lynx Corporation-Financial Performance AnalysisDocumento7 pagineData Section: Lynx Corporation-Financial Performance AnalysisAnh VânNessuna valutazione finora

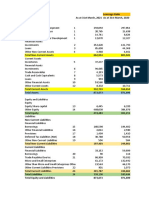

- Data Section: Lynx Corporation-Financial Performance AnalysisDocumento7 pagineData Section: Lynx Corporation-Financial Performance AnalysisLinh Tong Phuong QTKD-1TC-18Nessuna valutazione finora

- Go Rural FM AssignmentDocumento31 pagineGo Rural FM AssignmentHumphrey OsaigbeNessuna valutazione finora

- Corporate Valuation Day3Documento21 pagineCorporate Valuation Day3Pranay BansalNessuna valutazione finora

- The Relationship Bettwen NPV and Disco: NPV Sensitivity Analysis Data SectionDocumento11 pagineThe Relationship Bettwen NPV and Disco: NPV Sensitivity Analysis Data SectionMinh GiangNessuna valutazione finora

- Liston Mechanic CorporationDocumento14 pagineListon Mechanic CorporationKunal MehtaNessuna valutazione finora

- Accounting Information System HomeWork 1 Jazan UniversityDocumento7 pagineAccounting Information System HomeWork 1 Jazan Universityabdullah.masmaliNessuna valutazione finora

- Finance Project AMDDocumento35 pagineFinance Project AMDLuka KhmaladzeNessuna valutazione finora

- VIB - Section2 - Group5 - Final Project - ExcelDocumento70 pagineVIB - Section2 - Group5 - Final Project - ExcelShrishti GoyalNessuna valutazione finora

- Income Statement and Balance Sheet (LV & Parda)Documento30 pagineIncome Statement and Balance Sheet (LV & Parda)Pallavi KalraNessuna valutazione finora

- 2006 2007 June 2008Documento18 pagine2006 2007 June 2008Rishabh GigrasNessuna valutazione finora

- Mercury Athletic Footwear Answer Key FinalDocumento41 pagineMercury Athletic Footwear Answer Key FinalFatima ToapantaNessuna valutazione finora

- Q2 FY22 Financial TablesDocumento13 pagineQ2 FY22 Financial TablesDennis AngNessuna valutazione finora

- Financial AccountingDocumento21 pagineFinancial AccountingMariam KupravaNessuna valutazione finora

- Mercury Action Athletic Synergies & AssumptionsDocumento10 pagineMercury Action Athletic Synergies & AssumptionsSimón SegoviaNessuna valutazione finora

- INR Crore FY 16 FY 17 FY 18 FY 19 FY 20Documento5 pagineINR Crore FY 16 FY 17 FY 18 FY 19 FY 20Shivani SinghNessuna valutazione finora

- Financial Statement of JS Bank: Submitted ToDocumento22 pagineFinancial Statement of JS Bank: Submitted ToAtia KhalidNessuna valutazione finora

- Financial Statement AnalysisDocumento12 pagineFinancial Statement AnalysisjenNessuna valutazione finora

- AFM Project Sec J Group 10Documento32 pagineAFM Project Sec J Group 10J40Santhosh KrishnaNessuna valutazione finora

- FS Annual 2009 English STCDocumento25 pagineFS Annual 2009 English STCarkmaxNessuna valutazione finora

- Annual Report 2021Documento3 pagineAnnual Report 2021hxNessuna valutazione finora

- NKR Engineering (Private) Limited - June 2020Documento19 pagineNKR Engineering (Private) Limited - June 2020Mustafa hadiNessuna valutazione finora

- Chapter - 3 HW 3 - Apple RatiosDocumento4 pagineChapter - 3 HW 3 - Apple RatiosSubhash MishraNessuna valutazione finora

- Data Section: Ratio Analysis Chisholm Company 2015 & 2016Documento19 pagineData Section: Ratio Analysis Chisholm Company 2015 & 2016Hằngg ĐỗNessuna valutazione finora

- Q4 FY22 Financial TablesDocumento11 pagineQ4 FY22 Financial TablesDennis AngNessuna valutazione finora

- Balance Sheet & P & LDocumento3 pagineBalance Sheet & P & LSatish WagholeNessuna valutazione finora

- PSO StatementDocumento1 paginaPSO StatementNaseeb Ullah TareenNessuna valutazione finora

- 4 Years of Financial Data - v4Documento25 pagine4 Years of Financial Data - v4khusus downloadNessuna valutazione finora

- Hull Fund 9 Ech 12 Problem SolutionsDocumento8 pagineHull Fund 9 Ech 12 Problem SolutionsJitendra YadavNessuna valutazione finora

- Geojit Annual ReportDocumento144 pagineGeojit Annual ReportDeven ZanjarkiyaNessuna valutazione finora

- Maruti Suzuki ValuationDocumento39 pagineMaruti Suzuki ValuationritususmitakarNessuna valutazione finora

- Nke Model Di VincompleteDocumento10 pagineNke Model Di VincompletesalambakirNessuna valutazione finora

- Accounts AssignsmentDocumento8 pagineAccounts Assignsmentadityatiwari8303Nessuna valutazione finora

- Annual Report 2015 EN 2 PDFDocumento132 pagineAnnual Report 2015 EN 2 PDFQusai BassamNessuna valutazione finora

- Sinosteel Luoyang Institute of Refractories Research Co., LTDDocumento3 pagineSinosteel Luoyang Institute of Refractories Research Co., LTDvenus gargNessuna valutazione finora

- FS AaplDocumento20 pagineFS AaplReza FachrizalNessuna valutazione finora

- Audited Financial Statements Airlines 2021Documento60 pagineAudited Financial Statements Airlines 2021VENICE OMOLONNessuna valutazione finora

- Figures in INR MN: FY14A FY15A FY16A FY17A AssetsDocumento2 pagineFigures in INR MN: FY14A FY15A FY16A FY17A AssetsDeepakNessuna valutazione finora

- Ejemplo de Analisis Vertical y Horizontal Caso NikeDocumento14 pagineEjemplo de Analisis Vertical y Horizontal Caso NikeDiego Blanco CastroNessuna valutazione finora

- Valuation PracticeDocumento19 pagineValuation PracticeAkash PatilNessuna valutazione finora

- Globe Telecom Inc and Subsidiaries 2016 FS FINALDocumento175 pagineGlobe Telecom Inc and Subsidiaries 2016 FS FINALZanderNessuna valutazione finora

- Change of Desert Market, Aug - Sep '66 Compared To Aug - Sep '65Documento6 pagineChange of Desert Market, Aug - Sep '66 Compared To Aug - Sep '65Shyamal VermaNessuna valutazione finora

- Colgate ModelDocumento19 pagineColgate ModelRajat Agarwal100% (1)

- Greenko - Investment - Company - Audited - Combined - Financial - Statements - FY 2018 - 19Documento102 pagineGreenko - Investment - Company - Audited - Combined - Financial - Statements - FY 2018 - 19hNessuna valutazione finora

- 07-MIAA2021 Part1-Financial StatementsDocumento4 pagine07-MIAA2021 Part1-Financial StatementsVENICE OMOLONNessuna valutazione finora

- Annual Report 2019 3Documento77 pagineAnnual Report 2019 3andreileonard.asigurariNessuna valutazione finora

- Merrill Lynch Saudi Arabia Co Annual Fs - 2021Documento35 pagineMerrill Lynch Saudi Arabia Co Annual Fs - 2021RANessuna valutazione finora

- 2 Income StatmentDocumento1 pagina2 Income StatmentKatia LopezNessuna valutazione finora

- Annual-Accounts-2021 (2) - Pages-DeletedDocumento6 pagineAnnual-Accounts-2021 (2) - Pages-DeletedShehzad QureshiNessuna valutazione finora

- DG Khan Cement Financial StatementsDocumento8 pagineDG Khan Cement Financial StatementsAsad BumbiaNessuna valutazione finora

- Ratio Analysis of Lanka Ashok Leyland PLCDocumento6 pagineRatio Analysis of Lanka Ashok Leyland PLCThe MutantzNessuna valutazione finora

- Greenko Investment Company - Financial Statements 2017-18Documento93 pagineGreenko Investment Company - Financial Statements 2017-18DSddsNessuna valutazione finora

- Profit and LossDocumento1 paginaProfit and LossYagika JagnaniNessuna valutazione finora

- Chapter No 6Documento19 pagineChapter No 6AliNessuna valutazione finora

- Ind AS Balance Sheet of Dr. Reddy Labs 2020 2021: Non-Current AssetsDocumento24 pagineInd AS Balance Sheet of Dr. Reddy Labs 2020 2021: Non-Current Assetssumeet kumarNessuna valutazione finora

- Particulars (INR in Crores) FY2015A FY2016A FY2017A FY2018ADocumento6 pagineParticulars (INR in Crores) FY2015A FY2016A FY2017A FY2018AHamzah HakeemNessuna valutazione finora

- Mercury Case ExhibitsDocumento10 pagineMercury Case ExhibitsjujuNessuna valutazione finora

- Leverage RatioDocumento3 pagineLeverage RatioRahul PrasadNessuna valutazione finora

- Schaum's Outline of Bookkeeping and Accounting, Fourth EditionDa EverandSchaum's Outline of Bookkeeping and Accounting, Fourth EditionValutazione: 5 su 5 stelle5/5 (1)

- Chapter 17Documento7 pagineChapter 17Linh ChiNessuna valutazione finora

- CH 11Documento27 pagineCH 11Linh ChiNessuna valutazione finora

- MCQ Chapter 11Documento3 pagineMCQ Chapter 11Linh Chi100% (1)

- AnovaDocumento5 pagineAnovaLinh Chi0% (1)

- Question 1: Inference TechniqueDocumento1 paginaQuestion 1: Inference TechniqueLinh ChiNessuna valutazione finora

- Assignment 2 Group 101 291018Documento9 pagineAssignment 2 Group 101 291018Linh ChiNessuna valutazione finora

- Return On Equity (ROE) & Return On Asset (ROA) : Net Income Total Equity CapitalDocumento7 pagineReturn On Equity (ROE) & Return On Asset (ROA) : Net Income Total Equity CapitalLinh ChiNessuna valutazione finora

- Net Income Total Equity CapitalDocumento3 pagineNet Income Total Equity CapitalLinh ChiNessuna valutazione finora

- Shareholder Agreement 06Documento19 pagineShareholder Agreement 06Josmar TelloNessuna valutazione finora

- Bridging: Transportation: Chapter 3: The Transportation Planning ProcessDocumento28 pagineBridging: Transportation: Chapter 3: The Transportation Planning ProcesspercyNessuna valutazione finora

- Lucero Flores Resume 2Documento2 pagineLucero Flores Resume 2api-260292914Nessuna valutazione finora

- Chapter 01Documento26 pagineChapter 01zwright172Nessuna valutazione finora

- Tarlac - San Antonio - Business Permit - NewDocumento2 pagineTarlac - San Antonio - Business Permit - Newarjhay llave100% (1)

- Lenovo Security ThinkShield-Solutions-Guide Ebook IDG NA HV DownloadDocumento10 pagineLenovo Security ThinkShield-Solutions-Guide Ebook IDG NA HV DownloadManeshNessuna valutazione finora

- Circular Motion ProblemsDocumento4 pagineCircular Motion ProblemsGheline LexcieNessuna valutazione finora

- Water Cooled Centrifugal Chiller (150-3000RT)Documento49 pagineWater Cooled Centrifugal Chiller (150-3000RT)remigius yudhiNessuna valutazione finora

- Ljubljana European Green Capital 2016Documento56 pagineLjubljana European Green Capital 2016Kann_dandy17Nessuna valutazione finora

- Human Resource Management - Introduction - A Revision Article - A Knol by Narayana RaoDocumento7 pagineHuman Resource Management - Introduction - A Revision Article - A Knol by Narayana RaoHimanshu ShuklaNessuna valutazione finora

- Digirig Mobile 1 - 9 SchematicDocumento1 paginaDigirig Mobile 1 - 9 SchematicKiki SolihinNessuna valutazione finora

- National Action Plan Implementation Gaps and SuccessesDocumento8 pagineNational Action Plan Implementation Gaps and SuccessesHamza MinhasNessuna valutazione finora

- FAA PUBLICATIONS May Be Purchased or Downloaded For FreeDocumento4 pagineFAA PUBLICATIONS May Be Purchased or Downloaded For FreeFlávio AlibertiNessuna valutazione finora

- Group9 SecADocumento7 pagineGroup9 SecAshivendrakadamNessuna valutazione finora

- Lae ReservingDocumento5 pagineLae ReservingEsra Gunes YildizNessuna valutazione finora

- CasesDocumento4 pagineCasesSheldonNessuna valutazione finora

- New Form 2550 M Monthly VAT Return P 1 2 1Documento3 pagineNew Form 2550 M Monthly VAT Return P 1 2 1The ApprenticeNessuna valutazione finora

- Motion To DismissDocumento24 pagineMotion To DismisssandyemerNessuna valutazione finora

- Ein Extensive ListDocumento60 pagineEin Extensive ListRoberto Monterrosa100% (2)

- GTT NO96 LNG TanksDocumento5 pagineGTT NO96 LNG TanksEdutamNessuna valutazione finora

- Deploying MVC5 Based Provider Hosted Apps For On-Premise SharePoint 2013Documento22 pagineDeploying MVC5 Based Provider Hosted Apps For On-Premise SharePoint 2013cilango1Nessuna valutazione finora

- Taller Sobre Preposiciones y Vocabulario - Exhibición Comercial SergioDocumento5 pagineTaller Sobre Preposiciones y Vocabulario - Exhibición Comercial SergioYovanny Peña Pinzon100% (2)

- HK Magazine 03082013Documento56 pagineHK Magazine 03082013apparition9Nessuna valutazione finora

- High-Definition Multimedia Interface SpecificationDocumento51 pagineHigh-Definition Multimedia Interface SpecificationwadrNessuna valutazione finora

- IMO Publication Catalogue List (June 2022)Documento17 pagineIMO Publication Catalogue List (June 2022)Seinn NuNessuna valutazione finora

- Lab ManualDocumento15 pagineLab ManualsamyukthabaswaNessuna valutazione finora

- BW-Africa 2023 BrochureDocumento12 pagineBW-Africa 2023 BrochureDanial DarimiNessuna valutazione finora

- Applicant Details : Government of Tamilnadu Application Form For Vehicle E-Pass For Essential ServicesDocumento1 paginaApplicant Details : Government of Tamilnadu Application Form For Vehicle E-Pass For Essential ServicesŠářoĵ PrinceNessuna valutazione finora

- Philippine Multimodal Transportation and Logistics Industry Roadmap - Key Recommendations - 2016.04.14Documento89 paginePhilippine Multimodal Transportation and Logistics Industry Roadmap - Key Recommendations - 2016.04.14PortCalls50% (4)

- 1.2 Installation of SSH Keys On Linux-A Step-By Step GuideDocumento3 pagine1.2 Installation of SSH Keys On Linux-A Step-By Step GuideMada ChouchouNessuna valutazione finora