Potrebbero piacerti anche

- Comm 2Documento2 pagineComm 2the saintNessuna valutazione finora

- 2019 Bar ExaminationsDocumento62 pagine2019 Bar ExaminationsAllana Erica CortesNessuna valutazione finora

- Taxation Sia/Tabag TAX.2814-Community Tax MAY 2020: Lecture Notes A. IndividualsDocumento1 paginaTaxation Sia/Tabag TAX.2814-Community Tax MAY 2020: Lecture Notes A. IndividualsMay Grethel Joy PeranteNessuna valutazione finora

- Taxation Rules for Non-Resident Filipino and Capital GainsDocumento8 pagineTaxation Rules for Non-Resident Filipino and Capital GainsAnonymous oWQuKcUNessuna valutazione finora

- Far SummaryDocumento7 pagineFar SummaryKevinNessuna valutazione finora

- Vat With TrainDocumento16 pagineVat With TrainElla QuiNessuna valutazione finora

- Ra 10846 - PdicDocumento24 pagineRa 10846 - PdicJen AnchetaNessuna valutazione finora

- Revised Corporation Code (Sec. 45-139)Documento21 pagineRevised Corporation Code (Sec. 45-139)Scribd ScribdNessuna valutazione finora

- Intangibles PDFDocumento5 pagineIntangibles PDFJer RamaNessuna valutazione finora

- Spouses Pacquiao v. Court of Tax AppealsDocumento3 pagineSpouses Pacquiao v. Court of Tax AppealsFelicity HuffmanNessuna valutazione finora

- Strategic Management - Module 6 - Strategy Evaluation and ControlDocumento2 pagineStrategic Management - Module 6 - Strategy Evaluation and ControlEva Katrina R. LopezNessuna valutazione finora

- Receivables ProblemsDocumento4 pagineReceivables ProblemsLarpii MonameNessuna valutazione finora

- Midterms Case Study Week 7Documento7 pagineMidterms Case Study Week 7Dimple Mae CarilloNessuna valutazione finora

- Development Bank of The Philippines v. Felipe ArcillaDocumento17 pagineDevelopment Bank of The Philippines v. Felipe Arcillacyhaaangelaaa100% (1)

- SRC Cases DigestedDocumento5 pagineSRC Cases DigestedTalina BinondoNessuna valutazione finora

- Accounting For Franchise Operations - Franchisor: Name: Date: Professor: Section: Score: Quiz 1Documento2 pagineAccounting For Franchise Operations - Franchisor: Name: Date: Professor: Section: Score: Quiz 1Beverly ElepNessuna valutazione finora

- OpAudCh10-CBET-01-501E-Toralde, Ma - Kristine E.Documento6 pagineOpAudCh10-CBET-01-501E-Toralde, Ma - Kristine E.Kristine Esplana ToraldeNessuna valutazione finora

- Bar Questions in Negotiable InstrumentDocumento13 pagineBar Questions in Negotiable InstrumentAlyza Montilla BurdeosNessuna valutazione finora

- Input:Output Tax ReviewerDocumento2 pagineInput:Output Tax ReviewerHiedi SugamotoNessuna valutazione finora

- 1FDocumento2 pagine1FPaula Mae DacanayNessuna valutazione finora

- AC 3101 Discussion ProblemDocumento1 paginaAC 3101 Discussion ProblemYohann Leonard HuanNessuna valutazione finora

- Tax 2Documento3 pagineTax 2Emmanuel DiyNessuna valutazione finora

- Practical Accounting 2 Vol 2Documento129 paginePractical Accounting 2 Vol 2Boyd Banal100% (6)

- Advanced financial reporting and inventory managementDocumento9 pagineAdvanced financial reporting and inventory managementTh VNessuna valutazione finora

- Final 2 2Documento3 pagineFinal 2 2RonieOlarteNessuna valutazione finora

- Comprehensive QuizDocumento4 pagineComprehensive QuizBea LadaoNessuna valutazione finora

- ACCTG 2A and B Accounting For PartnershiDocumento16 pagineACCTG 2A and B Accounting For PartnershiMarvin RabinoNessuna valutazione finora

- Dissolution of partnership journal entriesDocumento6 pagineDissolution of partnership journal entriesSethwilsonNessuna valutazione finora

- Philippine Percentage Tax and Common Carrier Tax GuideDocumento148 paginePhilippine Percentage Tax and Common Carrier Tax GuideReginald ValenciaNessuna valutazione finora

- Updted Rem 1 Cases Set 2Documento314 pagineUpdted Rem 1 Cases Set 2Bediones JANessuna valutazione finora

- Cost-Volume-Profit AnalysisDocumento6 pagineCost-Volume-Profit AnalysisCher NaNessuna valutazione finora

- Income Taxation Ind PracticeDocumento3 pagineIncome Taxation Ind PracticeJanine Tividad100% (1)

- Audit CIS 1.4Documento4 pagineAudit CIS 1.4Patrick AlvinNessuna valutazione finora

- Discontinuing OperationsDocumento16 pagineDiscontinuing OperationsNeil Bryle Orilla NotarioNessuna valutazione finora

- TAX-303 (Input Taxes)Documento7 pagineTAX-303 (Input Taxes)Princess ManaloNessuna valutazione finora

- Elimination RoundDocumento11 pagineElimination RoundDeeNessuna valutazione finora

- Local Government Taxation Short Cases ExplainedDocumento1 paginaLocal Government Taxation Short Cases ExplainedRichard Rhamil Carganillo Garcia Jr.Nessuna valutazione finora

- RA 9178 BMBE ActDocumento69 pagineRA 9178 BMBE Actinvictusinc100% (1)

- 06 x06 Incremental AnalysisDocumento39 pagine06 x06 Incremental AnalysisClarisse AlimotNessuna valutazione finora

- Bustamante, Jilian Kate A. (Activity 3)Documento4 pagineBustamante, Jilian Kate A. (Activity 3)Jilian Kate Alpapara BustamanteNessuna valutazione finora

- Business Aspects Objectives MeasuresDocumento1 paginaBusiness Aspects Objectives MeasuresMauiNessuna valutazione finora

- Unit 1 History and New Directions of Accounting Research Exercise 1Documento9 pagineUnit 1 History and New Directions of Accounting Research Exercise 1Ivan AnaboNessuna valutazione finora

- RFBT - CPAR Pre-Boards in RFBT Batch 87 RFBT - CPAR Pre-Boards in RFBT Batch 87Documento11 pagineRFBT - CPAR Pre-Boards in RFBT Batch 87 RFBT - CPAR Pre-Boards in RFBT Batch 87Adelio BalmezNessuna valutazione finora

- Tax CPAR Final Pre Board2Documento5 pagineTax CPAR Final Pre Board2Floyd delMundo100% (1)

- Donation Is SolelyDocumento2 pagineDonation Is SolelyAnthony Angel Tejares50% (2)

- Sintos QuantiMethodsDocumento3 pagineSintos QuantiMethodsDalla SintosNessuna valutazione finora

- DBP vs Arcilla residential loan disputeDocumento12 pagineDBP vs Arcilla residential loan disputePam ChuaNessuna valutazione finora

- Module 2 - Strat ManDocumento4 pagineModule 2 - Strat ManElla MaeNessuna valutazione finora

- Ra 9178Documento11 pagineRa 9178Rahul HumpalNessuna valutazione finora

- QuizletDocumento4 pagineQuizletKizzea Bianca GadotNessuna valutazione finora

- Walker Books Bab 4Documento7 pagineWalker Books Bab 4Nuraeni Alti RunaNessuna valutazione finora

- PDF Advanced Accounting Solman CompressDocumento91 paginePDF Advanced Accounting Solman CompressLeah Mae NolascoNessuna valutazione finora

- PRTC PARTNERSHIP HandoutDocumento11 paginePRTC PARTNERSHIP HandoutKristian ArdoñaNessuna valutazione finora

- SEC MC No. 24, Series of 2019 PDFDocumento39 pagineSEC MC No. 24, Series of 2019 PDFJoanness BatimanaNessuna valutazione finora

- Resolution No.23 2010Documento13 pagineResolution No.23 2010Ronald ParrenoNessuna valutazione finora

- Ans To Exercises Stice Chap 1 and Hall Chap 1234 5 11 All ProblemsDocumento188 pagineAns To Exercises Stice Chap 1 and Hall Chap 1234 5 11 All ProblemsLouise GazaNessuna valutazione finora

- SEC Regulation of Investment Contracts and Insider TradingDocumento4 pagineSEC Regulation of Investment Contracts and Insider TradingJave Mike AtonNessuna valutazione finora

- Insider Trading in India: From The Selectedworks of Pankaj SinghDocumento25 pagineInsider Trading in India: From The Selectedworks of Pankaj SinghLEX-57 the lex engineNessuna valutazione finora

- Legal Regime Insider TradingDocumento12 pagineLegal Regime Insider TradingSukhamrit Singh ALS, NoidaNessuna valutazione finora

- G.R. No. 135808 ESCRADocumento81 pagineG.R. No. 135808 ESCRASta Maria JamesNessuna valutazione finora

- Pretrial Process FlowDocumento1 paginaPretrial Process FlowMosarah AltNessuna valutazione finora

- 2021 Schedule of Preweek LecturesDocumento1 pagina2021 Schedule of Preweek LecturesMarcky MarionNessuna valutazione finora

- LectureDocumento25 pagineLectureMarieNessuna valutazione finora

- Tax DigestsDocumento13 pagineTax DigestsMosarah AltNessuna valutazione finora

- Tax Case Digests CompilationDocumento207 pagineTax Case Digests CompilationFrancis Ray Arbon Filipinas83% (24)

- Politicsl LawDocumento91 paginePoliticsl LawMosarah AltNessuna valutazione finora

- Rights of Persons Under Custodial InvestigationDocumento13 pagineRights of Persons Under Custodial InvestigationLorebeth EspañaNessuna valutazione finora

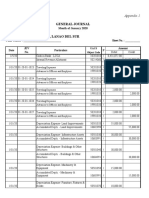

- General Journal: Appendix 1Documento5 pagineGeneral Journal: Appendix 1Mosarah AltNessuna valutazione finora

- Tax Case Digests CompilationDocumento207 pagineTax Case Digests CompilationFrancis Ray Arbon Filipinas83% (24)

- Banking and AMLADocumento26 pagineBanking and AMLAMosarah AltNessuna valutazione finora

- Civil Law Compilation Bar Q&a 1990-2017 PDFDocumento380 pagineCivil Law Compilation Bar Q&a 1990-2017 PDFReynaldo Yu100% (10)

- Abad Vs PhilcomsatDocumento2 pagineAbad Vs PhilcomsatFiels GamboaNessuna valutazione finora

- Rescission of Contracts & ChecksDocumento1 paginaRescission of Contracts & ChecksMosarah AltNessuna valutazione finora

- Equitable PCI Vs TanDocumento2 pagineEquitable PCI Vs TanMosarah AltNessuna valutazione finora

- Cayanan Vs North StarDocumento2 pagineCayanan Vs North StarMosarah AltNessuna valutazione finora

- PNB Vs BalmacedaDocumento2 paginePNB Vs BalmacedaMosarah AltNessuna valutazione finora

- Equitable Bank Liable for Depositing Crossed Checks in Wrong AccountDocumento1 paginaEquitable Bank Liable for Depositing Crossed Checks in Wrong AccountMosarah AltNessuna valutazione finora

- People V WagasDocumento1 paginaPeople V WagasMosarah AltNessuna valutazione finora

- Salazar Vs JY BrothersDocumento4 pagineSalazar Vs JY BrothersMosarah AltNessuna valutazione finora

- San Miguel Corp Vs PuzonDocumento2 pagineSan Miguel Corp Vs PuzonMosarah AltNessuna valutazione finora

- Tax ReviewerDocumento45 pagineTax ReviewerMosarah AltNessuna valutazione finora

- Ting Ting Pua V Sps TiongDocumento2 pagineTing Ting Pua V Sps TiongeieipayadNessuna valutazione finora

- Siochi Vs CA 2010 PDFDocumento9 pagineSiochi Vs CA 2010 PDFMosarah AltNessuna valutazione finora

- Equitable PCI Vs TanDocumento2 pagineEquitable PCI Vs TanMosarah AltNessuna valutazione finora

- Mock Trial ScriptDocumento25 pagineMock Trial ScriptRonilo Subaan94% (18)

- Ching Vs CA 1990Documento6 pagineChing Vs CA 1990Mosarah AltNessuna valutazione finora

- Politicsl LawDocumento91 paginePoliticsl LawMosarah AltNessuna valutazione finora

- Sps Ros Vs PNB 2011 PDFDocumento8 pagineSps Ros Vs PNB 2011 PDFMosarah AltNessuna valutazione finora

- Court Overturns Sale of Family PropertyDocumento7 pagineCourt Overturns Sale of Family PropertyMosarah AltNessuna valutazione finora

- Jpowui 0Documento13 pagineJpowui 0RevathiNessuna valutazione finora

- Big Bazaar - India's largest retail chainDocumento8 pagineBig Bazaar - India's largest retail chainPrathip KumarNessuna valutazione finora

- MURABAHADocumento27 pagineMURABAHANauman AminNessuna valutazione finora

- G.R. No. L-8988 court decision on Nagtajan Hacienda property saleDocumento86 pagineG.R. No. L-8988 court decision on Nagtajan Hacienda property saleAlyssa IlaganNessuna valutazione finora

- 60Documento9 pagine60srinivassukhavasiNessuna valutazione finora

- Paypal User AgreementDocumento34 paginePaypal User Agreementspark4uNessuna valutazione finora

- Vol-1 - Issue-1 of International Journal of Research in Commerce, Economics & ManagementDocumento149 pagineVol-1 - Issue-1 of International Journal of Research in Commerce, Economics & ManagementDr-Shefali GargNessuna valutazione finora

- CapstoneDocumento23 pagineCapstoneJhayan Luna100% (1)

- Arun Ice CreamDocumento3 pagineArun Ice CreamAslam Khan0% (1)

- Asuncion vs. CADocumento6 pagineAsuncion vs. CAKennex de DiosNessuna valutazione finora

- BM 18046 PVMDocumento6 pagineBM 18046 PVMPrabhat GuptaNessuna valutazione finora

- 25 Hotel Management Interview QuestionsDocumento14 pagine25 Hotel Management Interview Questionsbagoes12875100% (1)

- Suggestion Answer MGT657Documento22 pagineSuggestion Answer MGT657Hidayah Zulkifly80% (5)

- Toyota Shaw, Inc. vs. Court of AppealsDocumento1 paginaToyota Shaw, Inc. vs. Court of Appealsetc23100% (1)

- EE On Ikea and Its Marketing StrategiesDocumento16 pagineEE On Ikea and Its Marketing StrategiesWilmore JulioNessuna valutazione finora

- Tonny Research FirstDocumento47 pagineTonny Research Firstmulabbi brianNessuna valutazione finora

- BAO3309 2015SAMPLEBv2Documento6 pagineBAO3309 2015SAMPLEBv2zakskt1Nessuna valutazione finora

- Chapter 2 Premium and Warranty LiabilityDocumento20 pagineChapter 2 Premium and Warranty LiabilityCarlo VillanNessuna valutazione finora

- Prospecting, Profiling and Closing the BusinessDocumento20 pagineProspecting, Profiling and Closing the BusinessservicerNessuna valutazione finora

- Binuatan CreationsDocumento35 pagineBinuatan Creationsmarymen_mestidio100% (3)

- Executive Summary: 1.1 ObjectivesDocumento14 pagineExecutive Summary: 1.1 ObjectivesDo Minh TamNessuna valutazione finora

- How Is Iphone DevelopedDocumento3 pagineHow Is Iphone DevelopedHaveanash ParanthamanNessuna valutazione finora

- Account ManagerDocumento3 pagineAccount Managerapi-76974376Nessuna valutazione finora

- Changing The Way, We Buy FurnitureDocumento2 pagineChanging The Way, We Buy Furnituresheersha kkNessuna valutazione finora

- Marketing Analysis of Bpo SectorDocumento6 pagineMarketing Analysis of Bpo SectorAjit TanwarNessuna valutazione finora

- SMU A S: Retail MarketingDocumento27 pagineSMU A S: Retail MarketingGYANENDRA KUMAR MISHRANessuna valutazione finora

- Strategic ManagementDocumento9 pagineStrategic ManagementSree Raja Sekhar KatamNessuna valutazione finora

- Direct Marketing Methods ExplainedDocumento5 pagineDirect Marketing Methods ExplainedUrooj MahmoodNessuna valutazione finora

- Unilever CaseDocumento3 pagineUnilever CaseMari BurjatoNessuna valutazione finora

- Chapter 07 Futures and OptiDocumento68 pagineChapter 07 Futures and OptiLia100% (1)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingDa EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingValutazione: 4.5 su 5 stelle4.5/5 (97)

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorDa EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorValutazione: 4.5 su 5 stelle4.5/5 (63)

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementDa EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementValutazione: 4.5 su 5 stelle4.5/5 (20)

- Introduction to Negotiable Instruments: As per Indian LawsDa EverandIntroduction to Negotiable Instruments: As per Indian LawsValutazione: 5 su 5 stelle5/5 (1)

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpDa EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpValutazione: 4 su 5 stelle4/5 (214)

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsDa EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsValutazione: 5 su 5 stelle5/5 (24)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorDa EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorValutazione: 4.5 su 5 stelle4.5/5 (132)

- The Complete Book of Wills, Estates & Trusts (4th Edition): Advice That Can Save You Thousands of Dollars in Legal Fees and TaxesDa EverandThe Complete Book of Wills, Estates & Trusts (4th Edition): Advice That Can Save You Thousands of Dollars in Legal Fees and TaxesValutazione: 4 su 5 stelle4/5 (1)

- The Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessDa EverandThe Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessNessuna valutazione finora

- Richardson's Growth Company Guide 5.0: Investors, Deal Structures, Legal StrategiesDa EverandRichardson's Growth Company Guide 5.0: Investors, Deal Structures, Legal StrategiesNessuna valutazione finora

- Dealing With Problem Employees: How to Manage Performance & Personal Issues in the WorkplaceDa EverandDealing With Problem Employees: How to Manage Performance & Personal Issues in the WorkplaceNessuna valutazione finora

- IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASDa EverandIFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASValutazione: 3 su 5 stelle3/5 (5)

- Export & Import - Winning in the Global Marketplace: A Practical Hands-On Guide to Success in International Business, with 100s of Real-World ExamplesDa EverandExport & Import - Winning in the Global Marketplace: A Practical Hands-On Guide to Success in International Business, with 100s of Real-World ExamplesValutazione: 5 su 5 stelle5/5 (1)

- Ben & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooDa EverandBen & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooValutazione: 5 su 5 stelle5/5 (2)

- California Employment Law: An Employer's Guide: Revised and Updated for 2022Da EverandCalifornia Employment Law: An Employer's Guide: Revised and Updated for 2022Nessuna valutazione finora

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesDa EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesValutazione: 5 su 5 stelle5/5 (1)

- Learn the Essentials of Business Law in 15 DaysDa EverandLearn the Essentials of Business Law in 15 DaysValutazione: 4 su 5 stelle4/5 (13)

- The Streetwise Guide to Going Broke without Losing your ShirtDa EverandThe Streetwise Guide to Going Broke without Losing your ShirtNessuna valutazione finora

- The HR Answer Book: An Indispensable Guide for Managers and Human Resources ProfessionalsDa EverandThe HR Answer Book: An Indispensable Guide for Managers and Human Resources ProfessionalsValutazione: 3.5 su 5 stelle3.5/5 (3)