Potrebbero piacerti anche

- Hotel Ibis Trans Studio BandungDocumento2 pagineHotel Ibis Trans Studio BandungTedy Andiono100% (4)

- Bank Stetment PDFDocumento21 pagineBank Stetment PDFraj100% (1)

- Comfort Inn & Suites Los Alamos: Your Reservation Is ConfirmedDocumento2 pagineComfort Inn & Suites Los Alamos: Your Reservation Is ConfirmedNagendra SinghNessuna valutazione finora

- The Need For It and Challenges Ahead: Oods & Ervice AXDocumento18 pagineThe Need For It and Challenges Ahead: Oods & Ervice AXKuthe Prashant GajananNessuna valutazione finora

- Presentation On : Kiet Group of InstitutionsDocumento27 paginePresentation On : Kiet Group of InstitutionsVaishali SharmaNessuna valutazione finora

- Presentation On : Kiet Group of InstitutionsDocumento27 paginePresentation On : Kiet Group of InstitutionsVaishali SharmaNessuna valutazione finora

- Overview of GSTDocumento25 pagineOverview of GSTjugr57Nessuna valutazione finora

- GST Oct 17Documento23 pagineGST Oct 17himanNessuna valutazione finora

- Basics of GSTDocumento40 pagineBasics of GSTsportnik.in100% (1)

- Goods and Services Tax (GST) : Simplified byDocumento14 pagineGoods and Services Tax (GST) : Simplified bypushpendra singh sodhaNessuna valutazione finora

- Agt GSTDocumento28 pagineAgt GSTAmit GuptaNessuna valutazione finora

- An Overview of GSTDocumento19 pagineAn Overview of GSTDharmesh BhikadiyaNessuna valutazione finora

- GST Overview: Pankaj S Jain 17 December, 2016Documento5 pagineGST Overview: Pankaj S Jain 17 December, 2016Venkatraman NatarajanNessuna valutazione finora

- GST in India: Prepared By:-Shubham SharmaDocumento57 pagineGST in India: Prepared By:-Shubham Sharmamurali140Nessuna valutazione finora

- Goods & Services Act FinalDocumento78 pagineGoods & Services Act FinalParvesh AghiNessuna valutazione finora

- Public Finance GSTDocumento10 paginePublic Finance GSTMamta KasodariyaNessuna valutazione finora

- GST BasicsDocumento56 pagineGST BasicsrahulNessuna valutazione finora

- Overview of GST - PPT For GACDocumento57 pagineOverview of GST - PPT For GACRonak DesaiNessuna valutazione finora

- GST Presentation FB SCNDocumento26 pagineGST Presentation FB SCNPallavi ChawlaNessuna valutazione finora

- Issues and Challanges of GSTDocumento20 pagineIssues and Challanges of GSTshaik nazneenNessuna valutazione finora

- Goods and Services Tax (GST) in IndiaDocumento30 pagineGoods and Services Tax (GST) in IndiarupalNessuna valutazione finora

- GST in India: Dawn of A New Indirect Tax EraDocumento8 pagineGST in India: Dawn of A New Indirect Tax Eragulatiankur2010Nessuna valutazione finora

- Overview GSTDocumento56 pagineOverview GSTrahulNessuna valutazione finora

- GST FrameworkDocumento21 pagineGST FrameworkExecutive EngineerNessuna valutazione finora

- GST Summary PDFDocumento96 pagineGST Summary PDFkinnar2013Nessuna valutazione finora

- A Study On Goods & Service TaxDocumento15 pagineA Study On Goods & Service Taxgaikwadswapnil0603Nessuna valutazione finora

- A Solution For Indian GST Implementation For Simple Procurement Scenario Using TAXINNDocumento3 pagineA Solution For Indian GST Implementation For Simple Procurement Scenario Using TAXINNramakrishnaNessuna valutazione finora

- Role of CS in GSTDocumento66 pagineRole of CS in GSThareshmsNessuna valutazione finora

- Goods & Services Tax: An IntroductionDocumento30 pagineGoods & Services Tax: An IntroductionaniketzawarNessuna valutazione finora

- Durgapur 28052018Documento23 pagineDurgapur 28052018BhargavNessuna valutazione finora

- Bird Eye View of GST ActDocumento34 pagineBird Eye View of GST ActNarayan KulkarniNessuna valutazione finora

- GST Ebook sk-1Documento89 pagineGST Ebook sk-1KunalKumarNessuna valutazione finora

- Goods and Service Tax (GST) : Biggest Indirect Tax Reform in IndiaDocumento26 pagineGoods and Service Tax (GST) : Biggest Indirect Tax Reform in Indiafal_engNessuna valutazione finora

- Revised Model GST LawDocumento39 pagineRevised Model GST LawkshitijsaxenaNessuna valutazione finora

- Calender of EventsDocumento89 pagineCalender of EventsShankar ReddyNessuna valutazione finora

- Finance Activity in Sap MMDocumento27 pagineFinance Activity in Sap MMAnilGawandNessuna valutazione finora

- Goods and Services Tax: Group 3Documento16 pagineGoods and Services Tax: Group 3Kaushik ChakrabortyNessuna valutazione finora

- GST PWCDocumento24 pagineGST PWCsgk1611Nessuna valutazione finora

- GST - Final Presentation On Mutual Funds Sector - FINALDocumento44 pagineGST - Final Presentation On Mutual Funds Sector - FINALSulochana ChoudhuryNessuna valutazione finora

- GST Presentation With Ug Syllabus and Bengali Ug 2nd Year SyllabusDocumento16 pagineGST Presentation With Ug Syllabus and Bengali Ug 2nd Year Syllabusanirudra6aniNessuna valutazione finora

- PC Chart Book + Revision Videos On Youtube Guaranteed SuccessDocumento48 paginePC Chart Book + Revision Videos On Youtube Guaranteed SuccessPallab BaruahNessuna valutazione finora

- GST in IndiaDocumento13 pagineGST in IndiadiyasiddhuNessuna valutazione finora

- Background Material For 3days Refresher Course On GSTDocumento34 pagineBackground Material For 3days Refresher Course On GSTDevika JauhariNessuna valutazione finora

- Goods and Services Tax (GST) : Simplified byDocumento14 pagineGoods and Services Tax (GST) : Simplified byMohan ChoudharyNessuna valutazione finora

- Goods and Service TaxDocumento35 pagineGoods and Service Taxaditya2110Nessuna valutazione finora

- Goods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLADocumento30 pagineGoods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLAKrishna ShuklaNessuna valutazione finora

- GST - PersonalDocumento62 pagineGST - PersonalSri NiNessuna valutazione finora

- GST PPT June19Documento65 pagineGST PPT June19yash bhushanNessuna valutazione finora

- GST PPT Tkil FinalDocumento53 pagineGST PPT Tkil FinalVikas SharmaNessuna valutazione finora

- Goods and Services Tax (GST) in India: CA. Preeti GoyalDocumento30 pagineGoods and Services Tax (GST) in India: CA. Preeti GoyalArvind PalNessuna valutazione finora

- Micro Economic Project Work: TopicDocumento13 pagineMicro Economic Project Work: TopicRahul MuraliNessuna valutazione finora

- Goods & Services Tax: Make GST Work For YouDocumento7 pagineGoods & Services Tax: Make GST Work For Yougulatiankur2010Nessuna valutazione finora

- Chapter-12 GSTDocumento28 pagineChapter-12 GSTMohammad ZaynNessuna valutazione finora

- Goods & Services Tax - An Overview - ERO0240651 - ITT Batch 606Documento12 pagineGoods & Services Tax - An Overview - ERO0240651 - ITT Batch 606Siddharth Shankar PaikrayNessuna valutazione finora

- Goods and Services Tax " Future in India": by - Joe Suhas Thambi Rahul Aurade MET Institute of Management, NasikDocumento33 pagineGoods and Services Tax " Future in India": by - Joe Suhas Thambi Rahul Aurade MET Institute of Management, NasikJOEMEETSMONUNessuna valutazione finora

- Indirect Tax Revision Notes-CS Exe June 23 Lyst3130Documento56 pagineIndirect Tax Revision Notes-CS Exe June 23 Lyst3130tskpestsolutions.chennaiNessuna valutazione finora

- Goods and Services Tax (GST) Presentation To The Members of GJEPCDocumento53 pagineGoods and Services Tax (GST) Presentation To The Members of GJEPCAnkita TomarNessuna valutazione finora

- GST MSOP Project FinalDocumento19 pagineGST MSOP Project FinalAnjli SampatNessuna valutazione finora

- GST Intro - V 2 0Documento44 pagineGST Intro - V 2 0RaghuNessuna valutazione finora

- Goods & Service Tax (GST) : by CMA - Sameer EpariDocumento15 pagineGoods & Service Tax (GST) : by CMA - Sameer Eparihitesh nandawaniNessuna valutazione finora

- GST in BankingDocumento23 pagineGST in BankingNareshaasatNessuna valutazione finora

- CS Exe GST New PDFDocumento238 pagineCS Exe GST New PDFArundhati PawarNessuna valutazione finora

- Pricesystem - NovDocumento46 paginePricesystem - NovjaiswaniNessuna valutazione finora

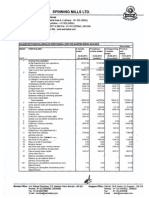

- Nahar Spinning Mills LTDDocumento3 pagineNahar Spinning Mills LTDjaiswaniNessuna valutazione finora

- Nahar Spinning Mills LTDDocumento3 pagineNahar Spinning Mills LTDjaiswaniNessuna valutazione finora

- Trading Holidays - List of Stock Market Holidays - BSEDocumento1 paginaTrading Holidays - List of Stock Market Holidays - BSEjaiswaniNessuna valutazione finora

- Trading Holidays - List of Stock Market Holidays - BSEDocumento1 paginaTrading Holidays - List of Stock Market Holidays - BSEjaiswaniNessuna valutazione finora

- The Commodity Edge Short Term Update 20111010Documento7 pagineThe Commodity Edge Short Term Update 20111010jaiswaniNessuna valutazione finora

- Alok Industries LTD: Q1FY12 Result UpdateDocumento9 pagineAlok Industries LTD: Q1FY12 Result UpdatejaiswaniNessuna valutazione finora

- European Doom and GloomDocumento6 pagineEuropean Doom and GloomjaiswaniNessuna valutazione finora

- United Phos. - UNICONDocumento3 pagineUnited Phos. - UNICONjaiswaniNessuna valutazione finora

- Punj LloydDocumento10 paginePunj LloydAngel BrokingNessuna valutazione finora

- 7595XXXXXXXXX777705 11 2018 PDFDocumento3 pagine7595XXXXXXXXX777705 11 2018 PDFSugar SugarNessuna valutazione finora

- TRB V RPNDocumento1 paginaTRB V RPNeieipayadNessuna valutazione finora

- Principles of Taxation For Business and Investment Planning 2019 22nd Edition Jones Test BankDocumento13 paginePrinciples of Taxation For Business and Investment Planning 2019 22nd Edition Jones Test Bankavadavatvulgatem71u2100% (15)

- Invoice: Tesla Norway ASDocumento1 paginaInvoice: Tesla Norway ASThomas LingottNessuna valutazione finora

- Channel Access Request FormDocumento3 pagineChannel Access Request FormRavi RamrakhaniNessuna valutazione finora

- Statement 1698578808753Documento26 pagineStatement 1698578808753abhay singhNessuna valutazione finora

- How To Authorize ACHDocumento12 pagineHow To Authorize ACHPete NgNessuna valutazione finora

- Test On Cashbook and Petty CashbookDocumento5 pagineTest On Cashbook and Petty Cashbookshamawail hassanNessuna valutazione finora

- 64 Aba 2 AbDocumento5 pagine64 Aba 2 Abgi estevesNessuna valutazione finora

- Statement of AccountDocumento3 pagineStatement of AccountPRAKASH VERMANessuna valutazione finora

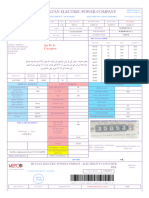

- Mepco Online BillDocumento2 pagineMepco Online Billsyedromanshah33Nessuna valutazione finora

- Maria Filipinas S. Joson Principal IIDocumento17 pagineMaria Filipinas S. Joson Principal IIAngela Maniego MendozaNessuna valutazione finora

- VAHAN 4.0 (Citizen Services) Onlineapp02 150 8013 GGDocumento1 paginaVAHAN 4.0 (Citizen Services) Onlineapp02 150 8013 GGmdneyaz9831Nessuna valutazione finora

- Income Tax Introduction FinalDocumento39 pagineIncome Tax Introduction FinalSammar EllahiNessuna valutazione finora

- 21 - 1040 (Forecast)Documento153 pagine21 - 1040 (Forecast)cjNessuna valutazione finora

- Buy Verified Stripe AccountDocumento10 pagineBuy Verified Stripe AccountUddin PhonesNessuna valutazione finora

- Dispute Resolution FormDocumento3 pagineDispute Resolution Formmerlin masterchiefNessuna valutazione finora

- Dinesh KumarDocumento3 pagineDinesh KumarHeri kimNessuna valutazione finora

- MBA Tuition Non Res FW 2022 2023Documento1 paginaMBA Tuition Non Res FW 2022 2023khabiranNessuna valutazione finora

- FAKE ITC SCN Instructions Cir-171!03!2022-CgstDocumento4 pagineFAKE ITC SCN Instructions Cir-171!03!2022-CgstGroupA PreventiveNessuna valutazione finora

- 2017 TXN - TXT 2 - PDF - BitcoinDocumento4 pagine2017 TXN - TXT 2 - PDF - BitcoinDaniel NaeNessuna valutazione finora

- Account Statement: Michael LoporchioDocumento2 pagineAccount Statement: Michael Loporchiodae ChoNessuna valutazione finora

- Purchase Order Purchase Order: Item Details Item DetailsDocumento1 paginaPurchase Order Purchase Order: Item Details Item Detailsnagesh99Nessuna valutazione finora

- Seabank Statement GiselaDocumento4 pagineSeabank Statement Giseladeajohn093Nessuna valutazione finora

- Quotation DotZotDocumento3 pagineQuotation DotZotGaurav singh BishtNessuna valutazione finora

- 360 Rewards Catalog PDFDocumento50 pagine360 Rewards Catalog PDFSyed Zain0% (1)

- Wak ContohDocumento5 pagineWak ContohDanial MustafaNessuna valutazione finora