Potrebbero piacerti anche

- DIY Credit Repair GuideDocumento21 pagineDIY Credit Repair GuideAnthony VinsonNessuna valutazione finora

- Price Determination Under Perfect CompetitionDocumento6 paginePrice Determination Under Perfect CompetitionDr. Swati Gupta100% (8)

- Unit-1 Scope of Economics Mechanism of Supply and DemandDocumento34 pagineUnit-1 Scope of Economics Mechanism of Supply and DemandsrivaruniNessuna valutazione finora

- Francis Nicholson, Richard Meek, Andrew Sherratt CIM Coursebook Managing MarketingDocumento284 pagineFrancis Nicholson, Richard Meek, Andrew Sherratt CIM Coursebook Managing MarketingRicky FernandoNessuna valutazione finora

- KIA MotorsDocumento20 pagineKIA MotorsNeha Ali25% (4)

- DisplayDocumento120 pagineDisplaySid Michael50% (2)

- Theory of ProductionDocumento19 pagineTheory of ProductionJessica Perez Pastorfide II100% (1)

- Economics For ManagersDocumento36 pagineEconomics For ManagersAmarNessuna valutazione finora

- IB Economics - Microeconomics NotesDocumento15 pagineIB Economics - Microeconomics NotesMICHELLE KARTIKA HS STUDENT100% (1)

- Khan General Stores 5lkhaDocumento28 pagineKhan General Stores 5lkhaakki_655150% (2)

- Solutions For Economics Review QuestionsDocumento28 pagineSolutions For Economics Review QuestionsDoris Acheng67% (3)

- Partial Equilibrium: EconomicsDocumento5 paginePartial Equilibrium: EconomicsSamantha SamdayNessuna valutazione finora

- Partial and General EquilibriumDocumento14 paginePartial and General EquilibriumkentbnxNessuna valutazione finora

- Intl Trade 09-12-2020Documento41 pagineIntl Trade 09-12-2020Mustansar saeedNessuna valutazione finora

- Chapter 5 - General EquilibrumDocumento23 pagineChapter 5 - General EquilibrumbashatigabuNessuna valutazione finora

- Princilpls of EconomicsDocumento31 paginePrincilpls of EconomicsRubina HannureNessuna valutazione finora

- ACC08/FMS01 Lectures: Economic Foundation of Financial ManagementDocumento15 pagineACC08/FMS01 Lectures: Economic Foundation of Financial ManagementmiolataNessuna valutazione finora

- Bba Chapter 4 Pricing Under Various Market ConditionsDocumento21 pagineBba Chapter 4 Pricing Under Various Market ConditionsDr-Abu Hasan Sonai SheikhNessuna valutazione finora

- Economics TheoryDocumento19 pagineEconomics TheoryadiNessuna valutazione finora

- Chapter 1 & 2: Normal Good Elasticity 1 Inferior Good Elasticity 1Documento7 pagineChapter 1 & 2: Normal Good Elasticity 1 Inferior Good Elasticity 1Assetou SinkaNessuna valutazione finora

- Summary of Demand, Supply, and Market EquilibriumDocumento3 pagineSummary of Demand, Supply, and Market EquilibriumAndreas Audi KemalNessuna valutazione finora

- Shivajirao S Jondhale Institute of Management Science & ResearchDocumento9 pagineShivajirao S Jondhale Institute of Management Science & Researchpravinpawar28Nessuna valutazione finora

- Engineering Economics Imon11Documento7 pagineEngineering Economics Imon1181Nessuna valutazione finora

- Business Economics: Mid Term SyllabusDocumento37 pagineBusiness Economics: Mid Term SyllabusZaigham AbbasNessuna valutazione finora

- Chapter 1: An Introduction To MicroeconomicsDocumento12 pagineChapter 1: An Introduction To MicroeconomicsBob SmithNessuna valutazione finora

- General Economics With Taxation and EntrepreneurshipDocumento56 pagineGeneral Economics With Taxation and EntrepreneurshipIc Rose2Nessuna valutazione finora

- General Economics With Taxation and EntrepreneurshipDocumento55 pagineGeneral Economics With Taxation and EntrepreneurshipZeejnANessuna valutazione finora

- ASSIGNMENT (Business Economic) : Aryan Goyal 18/FCBS/BBA (G) IB/003 Opportunity CostDocumento5 pagineASSIGNMENT (Business Economic) : Aryan Goyal 18/FCBS/BBA (G) IB/003 Opportunity CostAryan GoyalNessuna valutazione finora

- Economics NotesDocumento5 pagineEconomics NotesSpace Jam 2Nessuna valutazione finora

- Long Questions 1. Difference Between Micro and Macro EconomicsDocumento24 pagineLong Questions 1. Difference Between Micro and Macro EconomicsMac 02novNessuna valutazione finora

- M.B.A. (First Semester) Examination, 2014-15 Managerial Economics Model Answer Section - ADocumento28 pagineM.B.A. (First Semester) Examination, 2014-15 Managerial Economics Model Answer Section - AIjaz M.KNessuna valutazione finora

- Unit 4Documento65 pagineUnit 4M ChandruNessuna valutazione finora

- Managerial EconomicsDocumento6 pagineManagerial EconomicsDeepak YelwandeNessuna valutazione finora

- Reviewer EconDocumento5 pagineReviewer EconairaNessuna valutazione finora

- BEFA Unit 2 BSBDocumento7 pagineBEFA Unit 2 BSBBodapati Sai bhargav2002Nessuna valutazione finora

- English For EconomicsDocumento5 pagineEnglish For EconomicsЛиза ЛозновенкоNessuna valutazione finora

- What Is MicroeconomicsDocumento6 pagineWhat Is MicroeconomicsjuliaNessuna valutazione finora

- Pbea Unit-IiiDocumento24 paginePbea Unit-IiiYugandhar YugandharNessuna valutazione finora

- Macroeconomics ReviewDocumento14 pagineMacroeconomics ReviewkingalysonNessuna valutazione finora

- Engg EcnomicsDocumento55 pagineEngg Ecnomicsராஜ் முகமது100% (1)

- Economics : SupplyDocumento55 pagineEconomics : SupplyFaisal Raza SyedNessuna valutazione finora

- What Is Elasticity? What Factors Effects The Elasticity of Demand ? ElasticityDocumento4 pagineWhat Is Elasticity? What Factors Effects The Elasticity of Demand ? Elasticityyaqoob008Nessuna valutazione finora

- WEEK 6 Supply and Demand Analysis ExpandedDocumento2 pagineWEEK 6 Supply and Demand Analysis ExpandedAlipio Desuyo LaDjarNessuna valutazione finora

- Mefa Unit 3Documento33 pagineMefa Unit 3prasanna anjaneyulu tanneruNessuna valutazione finora

- Mefa Unit-IiiDocumento35 pagineMefa Unit-IiiGANDLA GOWTHAMI CSENessuna valutazione finora

- Ce40 CPR1Documento8 pagineCe40 CPR1Erwin Jed RachoNessuna valutazione finora

- Chapter 1Documento15 pagineChapter 1James SitohangNessuna valutazione finora

- Lesson Notes For S4 and S5Documento16 pagineLesson Notes For S4 and S5Zain NoorNessuna valutazione finora

- Demand and SupplyDocumento99 pagineDemand and SupplySOOMA OSMANNessuna valutazione finora

- 1629204622-1. Basic of MicroeconomicDocumento5 pagine1629204622-1. Basic of MicroeconomicTigerNessuna valutazione finora

- Question Bank - Eem UNIT-1: Q1. What Is Demand? Explain Law of Demand Meaning of DemandDocumento20 pagineQuestion Bank - Eem UNIT-1: Q1. What Is Demand? Explain Law of Demand Meaning of Demandjimaerospace05Nessuna valutazione finora

- Chap 03Documento16 pagineChap 03Syed Hamdan100% (1)

- Supply Curve Ppt-1Documento18 pagineSupply Curve Ppt-1mansi mehtaNessuna valutazione finora

- Midterm Exam Reviewer - EconDocumento3 pagineMidterm Exam Reviewer - EconHatdog KaNessuna valutazione finora

- Ecs Exam PackDocumento137 pagineEcs Exam PackWah NgcoboNessuna valutazione finora

- Managerial Economics - Lecture 1Documento33 pagineManagerial Economics - Lecture 1Yasser RamadanNessuna valutazione finora

- Module 7 Market StructureDocumento82 pagineModule 7 Market StructureShobharaj HegadeNessuna valutazione finora

- Applied Economics Lecture Long BondpaperDocumento10 pagineApplied Economics Lecture Long BondpaperMylene Ronquillo FernandezNessuna valutazione finora

- Characteristics of MicroeconomicsDocumento11 pagineCharacteristics of MicroeconomicsMaria JessaNessuna valutazione finora

- And Deals With Their Business Transaction. Mysore Market EtcDocumento7 pagineAnd Deals With Their Business Transaction. Mysore Market Etcarchana_anuragiNessuna valutazione finora

- Unit 1 Introduction To Economics What Is An Economy?Documento8 pagineUnit 1 Introduction To Economics What Is An Economy?khushnuma20Nessuna valutazione finora

- Book 3Documento6 pagineBook 3Vinh TrầnNessuna valutazione finora

- Economics For Managers (EFM) (4519905)Documento20 pagineEconomics For Managers (EFM) (4519905)shivam networkNessuna valutazione finora

- SuggestionDocumento8 pagineSuggestionanupareek1301Nessuna valutazione finora

- NotesDocumento17 pagineNotesKripaya ShakyaNessuna valutazione finora

- SLG SS5 1.1 Demand Part 1Documento9 pagineSLG SS5 1.1 Demand Part 1rbm121415chyNessuna valutazione finora

- Chapter 3 Notes Principles of MicroeconomicsDocumento3 pagineChapter 3 Notes Principles of MicroeconomicsDerek Ng100% (3)

- 07 BibliographyDocumento5 pagine07 BibliographyMaha RajaNessuna valutazione finora

- Chapter 4 Question Review 11th EdDocumento9 pagineChapter 4 Question Review 11th EdEmiraslan MhrrovNessuna valutazione finora

- Full-Text HTML XML Download As PDFDocumento17 pagineFull-Text HTML XML Download As PDFMARICAR TADURANNessuna valutazione finora

- Chapter 14Documento19 pagineChapter 14Yuxuan Song100% (1)

- Pantene Case StudyDocumento21 paginePantene Case StudyMuhammad AreebNessuna valutazione finora

- Monitoring The Smart Money by Using On Balance Volume PDFDocumento5 pagineMonitoring The Smart Money by Using On Balance Volume PDFFasc CruzNessuna valutazione finora

- Ind AS 115Documento21 pagineInd AS 115Vrinda KNessuna valutazione finora

- Masr2205 - Cost Definition, Concepts, Classification & AnalysisDocumento11 pagineMasr2205 - Cost Definition, Concepts, Classification & AnalysisDaniela AubreyNessuna valutazione finora

- OneChicago Fact SheetDocumento1 paginaOneChicago Fact SheetJosh AlexanderNessuna valutazione finora

- NSCC International Business Internship - FlyerDocumento2 pagineNSCC International Business Internship - FlyerNSCC International BusinessNessuna valutazione finora

- Presentation On Traditional Marketing and Value Retention MarketingDocumento18 paginePresentation On Traditional Marketing and Value Retention Marketingscorpionking14Nessuna valutazione finora

- BabygarmentsDocumento20 pagineBabygarmentsMSM HUBNessuna valutazione finora

- CB Starbucks Grp6Documento9 pagineCB Starbucks Grp6Tushar ShettyNessuna valutazione finora

- Customer Journey PDFDocumento15 pagineCustomer Journey PDFMohammad Darwis IbrahimNessuna valutazione finora

- Consumer SegmentationDocumento4 pagineConsumer SegmentationPravish Lionel DcostaNessuna valutazione finora

- AIMSJ Vol 9 No 1 2006 P 45-66Documento22 pagineAIMSJ Vol 9 No 1 2006 P 45-66Le Xuan LapNessuna valutazione finora

- CHAPTER 2 - Partnership OperationsDocumento10 pagineCHAPTER 2 - Partnership OperationsRominna Dela RuedaNessuna valutazione finora

- PRC - 05 ITB Mock JAN-23Documento7 paginePRC - 05 ITB Mock JAN-23Aayesha Noor0% (1)

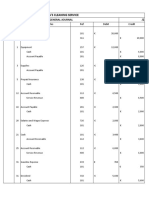

- Anya's Cleaning ServiceDocumento22 pagineAnya's Cleaning ServiceArya HerdiansyahNessuna valutazione finora

- Economics: Elasticity and Its ApplicationDocumento49 pagineEconomics: Elasticity and Its ApplicationAsif Bin LatifNessuna valutazione finora

- Bank of Rajasthan MergerDocumento75 pagineBank of Rajasthan MergerArunKumar100% (1)

- Mark Scheme January 2009: GCE O Level Accounting (7011)Documento22 pagineMark Scheme January 2009: GCE O Level Accounting (7011)karmenlopezholaNessuna valutazione finora