Potrebbero piacerti anche

- Q3 23 Conference Call TranscriptDocumento9 pagineQ3 23 Conference Call TranscriptAjaxNessuna valutazione finora

- Greaves Concall TranscriptDocumento15 pagineGreaves Concall Transcriptnadekaramit9122Nessuna valutazione finora

- ConcallQ4FY21 Kellton Tech SolutionsLtd Transcript - 0Documento10 pagineConcallQ4FY21 Kellton Tech SolutionsLtd Transcript - 0Sahil DagarNessuna valutazione finora

- Con Call Transcript IDFCDocumento16 pagineCon Call Transcript IDFCsanjeev7777Nessuna valutazione finora

- Brand Concepts LimitedDocumento33 pagineBrand Concepts LimitedVishalNessuna valutazione finora

- Tata Elxsi FY20 Q4 Earnings Conference Call Summary - CEO Discusses Financial Performance and Impact of COVID-19Documento17 pagineTata Elxsi FY20 Q4 Earnings Conference Call Summary - CEO Discusses Financial Performance and Impact of COVID-19Ashutosh GuptaNessuna valutazione finora

- Transcript Schaeffler India Limited-Earnings Conference Call-19Apr-2023Documento19 pagineTranscript Schaeffler India Limited-Earnings Conference Call-19Apr-2023JBNessuna valutazione finora

- NIIT Technologies Limited: Investors Conference Call For Quarterly Results Ended Jun 2006 July 19, 2006Documento22 pagineNIIT Technologies Limited: Investors Conference Call For Quarterly Results Ended Jun 2006 July 19, 2006Jaya RamchandaniNessuna valutazione finora

- 11 112020 CupidDocumento13 pagine11 112020 Cupidravi.youNessuna valutazione finora

- Q2fy24 Concall ZomatoDocumento15 pagineQ2fy24 Concall ZomatoneesadhNessuna valutazione finora

- Transcript of Conference Call (Company Update)Documento25 pagineTranscript of Conference Call (Company Update)Shyam SunderNessuna valutazione finora

- Q1FY21Documento18 pagineQ1FY21Err DatabaseNessuna valutazione finora

- "YES Bank Q1FY21 Earnings Conference Call": July 28, 2020Documento13 pagine"YES Bank Q1FY21 Earnings Conference Call": July 28, 2020Prathamesh LadNessuna valutazione finora

- Sunteck Transcript Q1 FY 2023Documento10 pagineSunteck Transcript Q1 FY 2023KIPL BLACKSWANNessuna valutazione finora

- Edelweiss Kwality 15dec 2016Documento19 pagineEdelweiss Kwality 15dec 2016rajesh katareNessuna valutazione finora

- Transcript-Earning Call - Q1!07!08Documento22 pagineTranscript-Earning Call - Q1!07!08mayan3345Nessuna valutazione finora

- Dalmia Bharat Limited Quarter and Year Ended Earnings 31st March 2019 Conference CallDocumento17 pagineDalmia Bharat Limited Quarter and Year Ended Earnings 31st March 2019 Conference CallJagannath DNessuna valutazione finora

- ShowreportDocumento56 pagineShowreportDinesh sawantNessuna valutazione finora

- 3M SeekingAlphaDocumento4 pagine3M SeekingAlphachukkNessuna valutazione finora

- Q2FY22Documento25 pagineQ2FY22Err DatabaseNessuna valutazione finora

- Computer Age Management Services Limited Q2 Earnings Conference CallDocumento17 pagineComputer Age Management Services Limited Q2 Earnings Conference CallJagannath DNessuna valutazione finora

- IL&FS Transportation Earnings Call SummaryDocumento40 pagineIL&FS Transportation Earnings Call SummarycontactdpsNessuna valutazione finora

- PhillipCap JindalSaw 14aug 2023Documento13 paginePhillipCap JindalSaw 14aug 2023sahil.goelNessuna valutazione finora

- q3 Fy23 Earnings Call TranscriptDocumento21 pagineq3 Fy23 Earnings Call TranscriptSohail AlamNessuna valutazione finora

- Cholamandalam Investment & Finance Company Limited Q1 FY-15 Earnings Conference CallDocumento16 pagineCholamandalam Investment & Finance Company Limited Q1 FY-15 Earnings Conference CallAnonymous lfw4mfCmNessuna valutazione finora

- Transcript Earning Call 08-09Q2Documento32 pagineTranscript Earning Call 08-09Q2shwetaforeNessuna valutazione finora

- 18 For 18Documento13 pagine18 For 18Jaldeep KarasaliyaNessuna valutazione finora

- Earnings Con Call-Q3 Fy 17 18Documento24 pagineEarnings Con Call-Q3 Fy 17 18Sourav DuttaNessuna valutazione finora

- Apcotex-Concall Transcript-Q4-FY 21-22Documento15 pagineApcotex-Concall Transcript-Q4-FY 21-22Vivek RamNessuna valutazione finora

- "GTPL Hathway Limited Annual FY 2019 & Q4 FY2019 Results Conference Call" April 16, 2019Documento17 pagine"GTPL Hathway Limited Annual FY 2019 & Q4 FY2019 Results Conference Call" April 16, 2019Sun TanNessuna valutazione finora

- Group01 - Construction IndustryDocumento18 pagineGroup01 - Construction IndustrySAHIL JAISWALNessuna valutazione finora

- Transcript MM Q2fy23 Earnings Call 11th Nov 2022 FinalDocumento19 pagineTranscript MM Q2fy23 Earnings Call 11th Nov 2022 FinalfafNessuna valutazione finora

- "Alkem Laboratories Limited Q3 FY2020 Earnings Conference Call" February 07, 2020Documento20 pagine"Alkem Laboratories Limited Q3 FY2020 Earnings Conference Call" February 07, 2020GurjeevNessuna valutazione finora

- Q4 FY2019 Earnings Call Transcript SummaryDocumento30 pagineQ4 FY2019 Earnings Call Transcript SummaryDeep GandhiNessuna valutazione finora

- CC June 16Documento13 pagineCC June 16tarun lahotiNessuna valutazione finora

- Q1 FY '24 Earnings Conference Call" Aug23Documento20 pagineQ1 FY '24 Earnings Conference Call" Aug23big shortNessuna valutazione finora

- Q4 FY'17 Transcript Ashok LwylandDocumento19 pagineQ4 FY'17 Transcript Ashok LwylandAbhishek SinhaNessuna valutazione finora

- Q1 2012 Earnings Call - Hero Honda Dt-21 Jul'11: OperatorDocumento20 pagineQ1 2012 Earnings Call - Hero Honda Dt-21 Jul'11: Operatorksangadi9Nessuna valutazione finora

- FY19 Call TranscriptDocumento21 pagineFY19 Call TranscriptDebashree NagarNessuna valutazione finora

- Racl Gear TechDocumento10 pagineRacl Gear Techravi.youNessuna valutazione finora

- "Jindal Steel & Power Q1 FY2024 Earnings Conference Call" August 11, 2023Documento11 pagine"Jindal Steel & Power Q1 FY2024 Earnings Conference Call" August 11, 2023Manish PatraNessuna valutazione finora

- Infibeam Avenues Limited Q3 FY2019 Earnings Conference CallDocumento16 pagineInfibeam Avenues Limited Q3 FY2019 Earnings Conference CallVikaas ChouhanNessuna valutazione finora

- "Cipla Q1FY14 Earnings Conference Call": August 09, 2013Documento18 pagine"Cipla Q1FY14 Earnings Conference Call": August 09, 2013GyaneshNessuna valutazione finora

- Arm Q2 FYE24 Results: Wednesday, 8 November 2023Documento18 pagineArm Q2 FYE24 Results: Wednesday, 8 November 2023taranulcuolcitNessuna valutazione finora

- 3I SeekingAlphaDocumento5 pagine3I SeekingAlphachukkNessuna valutazione finora

- Adlabs Entertainment Q1 FY16 Earnings Call TranscriptDocumento16 pagineAdlabs Entertainment Q1 FY16 Earnings Call TranscriptAdhirajNessuna valutazione finora

- Press ConferenceDocumento11 paginePress ConferenceAK GNessuna valutazione finora

- TCS Transcript Call Q1 12Documento25 pagineTCS Transcript Call Q1 12swathi_ipeNessuna valutazione finora

- Sanjiv KapurDocumento8 pagineSanjiv KapurNadeem ManzoorNessuna valutazione finora

- Commercial Engineers and Bodybuilders Company LimitedDocumento16 pagineCommercial Engineers and Bodybuilders Company LimitedsusegaadNessuna valutazione finora

- SONA BLW Precision Forgings Ltd. (Sona Comstar) : Q1 FY22 Earnings Conference Call TranscriptDocumento24 pagineSONA BLW Precision Forgings Ltd. (Sona Comstar) : Q1 FY22 Earnings Conference Call TranscriptVishal PrasadNessuna valutazione finora

- Q3FY22Documento23 pagineQ3FY22Err DatabaseNessuna valutazione finora

- Board of Directors and LeadershipDocumento108 pagineBoard of Directors and LeadershipSiva KumarNessuna valutazione finora

- Q2fy24 Concall MapmyindiaDocumento18 pagineQ2fy24 Concall MapmyindianeesadhNessuna valutazione finora

- Sobha Limited Q1 FY2020 Post Results Conference CallDocumento18 pagineSobha Limited Q1 FY2020 Post Results Conference Calltarun lahotiNessuna valutazione finora

- Transcript TPL Q1 20-21Documento21 pagineTranscript TPL Q1 20-21Rahul ShastriNessuna valutazione finora

- Jagran Prakashan Transcript Q4FY20Documento23 pagineJagran Prakashan Transcript Q4FY20Sam vermNessuna valutazione finora

- Scrip Code: 543272 Symbol: EASEMYTRIP Sub: Earning Call TranscriptDocumento13 pagineScrip Code: 543272 Symbol: EASEMYTRIP Sub: Earning Call TranscriptmadristasareoneNessuna valutazione finora

- A Mobile Bike Repair Service Business Plan: To Start with Little to No MoneyDa EverandA Mobile Bike Repair Service Business Plan: To Start with Little to No MoneyNessuna valutazione finora

- Outbound Hiring: How Innovative Companies are Winning the Global War for TalentDa EverandOutbound Hiring: How Innovative Companies are Winning the Global War for TalentNessuna valutazione finora

- Adani Enter AR 2019 PDFDocumento325 pagineAdani Enter AR 2019 PDFPoonam AggarwalNessuna valutazione finora

- Tata Chemicals: Flight of RebirthDocumento52 pagineTata Chemicals: Flight of RebirthPoonam AggarwalNessuna valutazione finora

- Torrent Power 20190319 Mosl Ic Pg034Documento34 pagineTorrent Power 20190319 Mosl Ic Pg034Poonam AggarwalNessuna valutazione finora

- Top Funds Have Increased Stake in This Real Estate Company!Documento45 pagineTop Funds Have Increased Stake in This Real Estate Company!Poonam AggarwalNessuna valutazione finora

- A GL Presentation Aug 18Documento23 pagineA GL Presentation Aug 18Poonam AggarwalNessuna valutazione finora

- Torrent Power 20190319 Mosl Ic Pg034Documento34 pagineTorrent Power 20190319 Mosl Ic Pg034Poonam AggarwalNessuna valutazione finora

- CMP: INR2,022 TP: INR2,636 (+30%) Stellar Growth, RM Exerts Pressure On MarginDocumento10 pagineCMP: INR2,022 TP: INR2,636 (+30%) Stellar Growth, RM Exerts Pressure On MarginPoonam AggarwalNessuna valutazione finora

- ASTROLOGYDocumento10 pagineASTROLOGYPoonam AggarwalNessuna valutazione finora

- Future ConsumerDocumento32 pagineFuture ConsumerPoonam AggarwalNessuna valutazione finora

- Jyotish-Sar - Hindi PDFDocumento252 pagineJyotish-Sar - Hindi PDFPoonam AggarwalNessuna valutazione finora

- Adani Gas LTD: Investor PresentationDocumento32 pagineAdani Gas LTD: Investor PresentationVedantNessuna valutazione finora

- SHAREDocumento2 pagineSHAREPoonam AggarwalNessuna valutazione finora

- AEL Q1FY20 Performance HighlightsDocumento10 pagineAEL Q1FY20 Performance HighlightsPoonam AggarwalNessuna valutazione finora

- ADANIDocumento1 paginaADANIPoonam AggarwalNessuna valutazione finora

- ATL Investor Presentation April 2019Documento54 pagineATL Investor Presentation April 2019Poonam AggarwalNessuna valutazione finora

- Adani Composites Brochure2019Documento11 pagineAdani Composites Brochure2019Poonam AggarwalNessuna valutazione finora

- ATL Investor Presentation April 2019Documento54 pagineATL Investor Presentation April 2019Poonam AggarwalNessuna valutazione finora

- Q4 FY 19 - Performance HighlightsDocumento9 pagineQ4 FY 19 - Performance HighlightsPoonam AggarwalNessuna valutazione finora

- Adani Gas Annual Report 2019Documento213 pagineAdani Gas Annual Report 2019Poonam AggarwalNessuna valutazione finora

- AEL Q4FY19 Performance HighlightsDocumento10 pagineAEL Q4FY19 Performance HighlightsPoonam AggarwalNessuna valutazione finora

- ADANI GREEN ENERGY LIMITED INVESTOR PRESENTATION HIGHLIGHTS KEY GROWTH DRIVERSDocumento33 pagineADANI GREEN ENERGY LIMITED INVESTOR PRESENTATION HIGHLIGHTS KEY GROWTH DRIVERSPoonam Aggarwal100% (1)

- Q4 FY 19 - Performance HighlightsDocumento9 pagineQ4 FY 19 - Performance HighlightsPoonam AggarwalNessuna valutazione finora

- Adani Enterprises Investor Presentation Growth With Goodness April 2019Documento54 pagineAdani Enterprises Investor Presentation Growth With Goodness April 2019Poonam AggarwalNessuna valutazione finora

- Adani Enterprises Limited Annual Report 2018-19Documento325 pagineAdani Enterprises Limited Annual Report 2018-19Poonam AggarwalNessuna valutazione finora

- Building a Secure Nation through Defence and AerospaceDocumento20 pagineBuilding a Secure Nation through Defence and AerospaceAnkit BulsaraNessuna valutazione finora

- Google AdSense Online Terms of Service SummaryDocumento6 pagineGoogle AdSense Online Terms of Service SummaryPoonam AggarwalNessuna valutazione finora

- Adani Group May - 2019Documento15 pagineAdani Group May - 2019Poonam AggarwalNessuna valutazione finora

- New Microsoft Office Word DocumentDocumento7 pagineNew Microsoft Office Word DocumentPoonam AggarwalNessuna valutazione finora

- Diary 2018-19 by Harish Mota HippoDocumento4 pagineDiary 2018-19 by Harish Mota HippoPoonam AggarwalNessuna valutazione finora

- Working Capital Management at Abhinandan EngineersDocumento60 pagineWorking Capital Management at Abhinandan EngineersSushil HongekarNessuna valutazione finora

- JDE Enterprise Profitability SolutionDocumento244 pagineJDE Enterprise Profitability SolutionSanjay GuptaNessuna valutazione finora

- Analysis of Ambuja Cements LimitedDocumento1 paginaAnalysis of Ambuja Cements LimitedJayant Lakhotia0% (1)

- Merger & AcquisitionDocumento15 pagineMerger & AcquisitionmadegNessuna valutazione finora

- Business Contacts Bulletin - May Sri LankaDocumento19 pagineBusiness Contacts Bulletin - May Sri LankaDurban Chamber of Commerce and IndustryNessuna valutazione finora

- Manufacturing Shampoo Project ProfileDocumento2 pagineManufacturing Shampoo Project Profilevineetaggarwal50% (2)

- Literature ReviewDocumento3 pagineLiterature Reviewrammi1318100% (1)

- Comparison Table of Luxembourg Investment VehiclesDocumento11 pagineComparison Table of Luxembourg Investment Vehiclesoliviersciales100% (1)

- SIRA1H11Documento8 pagineSIRA1H11Inde Pendent LkNessuna valutazione finora

- Top - 100 Outsourcing Location Ranking - 2013 Tholons PDFDocumento11 pagineTop - 100 Outsourcing Location Ranking - 2013 Tholons PDFvendetta82pgNessuna valutazione finora

- Acquisition Goodwill CalculationsDocumento21 pagineAcquisition Goodwill CalculationsJack Herer100% (1)

- Inflation Impact On EconmyDocumento4 pagineInflation Impact On EconmyRashid HussainNessuna valutazione finora

- Trondheim - Doc 19 TranscriptDocumento71 pagineTrondheim - Doc 19 Transcriptwalt373Nessuna valutazione finora

- A Project Report On Stress Management at Icici-PrudentialDocumento113 pagineA Project Report On Stress Management at Icici-PrudentialBabasab Patil (Karrisatte)0% (2)

- Trust DeedDocumento8 pagineTrust Deededdy_edwin23Nessuna valutazione finora

- 356SDocumento256 pagine356SMian UsmanNessuna valutazione finora

- Lbo Model Short FormDocumento6 pagineLbo Model Short FormHeu Sai HoeNessuna valutazione finora

- Au Small Finance BankDocumento27 pagineAu Small Finance BankRuhi Rana100% (2)

- Set-22 Mba I Semester Assign QuestionsDocumento10 pagineSet-22 Mba I Semester Assign Questionsஇந்துமதி வெங்கடரமணன்Nessuna valutazione finora

- Year Overview 2012 FinalDocumento65 pagineYear Overview 2012 FinalArjenvanLinNessuna valutazione finora

- Petron Corporation: Profile of the Leading Oil Refiner and Fuel Provider in the PhilippinesDocumento26 paginePetron Corporation: Profile of the Leading Oil Refiner and Fuel Provider in the PhilippinesAl CayosaNessuna valutazione finora

- FORM16: Signature Not VerifiedDocumento5 pagineFORM16: Signature Not Verifiedmath_mallikarjun_sapNessuna valutazione finora

- RBI Report On Financial Inclusion DeepeningDocumento265 pagineRBI Report On Financial Inclusion DeepeningSriramkartik KVNessuna valutazione finora

- Stock Articles of IncorporationDocumento5 pagineStock Articles of IncorporationRuffa TagalagNessuna valutazione finora

- National Income Accounting For Plus TwoDocumento66 pagineNational Income Accounting For Plus TwogmvNessuna valutazione finora

- Chapter 22Documento40 pagineChapter 22bayu0% (1)

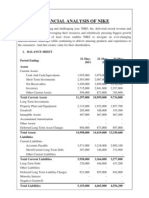

- Financial Analysis of NikeDocumento5 pagineFinancial Analysis of NikenimmymathewpkkthlNessuna valutazione finora

- PROJECTDocumento62 paginePROJECTaishwarya haleNessuna valutazione finora

- EECO - Problem Set - Annuities and PerpetuitiesDocumento10 pagineEECO - Problem Set - Annuities and PerpetuitiesWebb PalangNessuna valutazione finora

- Republic Act No. 7652Documento2 pagineRepublic Act No. 7652Ju BalajadiaNessuna valutazione finora