Potrebbero piacerti anche

- ReporttDocumento7 pagineReporttaryan nicoleNessuna valutazione finora

- Problems 3 PRELIM TASK FINALDocumento4 pagineProblems 3 PRELIM TASK FINALJohn Francis RosasNessuna valutazione finora

- Chapter 18 Investment in AssociateDocumento5 pagineChapter 18 Investment in AssociateEllen MaskariñoNessuna valutazione finora

- Ap2904 Cash and Cash EquivalentsDocumento8 pagineAp2904 Cash and Cash EquivalentsMa Yra YmataNessuna valutazione finora

- Premium-Liability Bafacr4x OnlineglimpsenujpiaDocumento8 paginePremium-Liability Bafacr4x OnlineglimpsenujpiaAga Mathew MayugaNessuna valutazione finora

- Advacc2 MQ2Documento2 pagineAdvacc2 MQ2Karina Barretto Agnes0% (1)

- Buscom ReviewerDocumento16 pagineBuscom ReviewereysiNessuna valutazione finora

- MSC-Audited FS With Notes - 2014 - CaseDocumento12 pagineMSC-Audited FS With Notes - 2014 - CaseMikaela SalvadorNessuna valutazione finora

- Donor's TaxDocumento3 pagineDonor's TaxAimeeNessuna valutazione finora

- Watered Share (IA3)Documento3 pagineWatered Share (IA3)Cecile SongcoNessuna valutazione finora

- Comprehensive Far Part 3Documento21 pagineComprehensive Far Part 3LabLab ChattoNessuna valutazione finora

- Fedillaga Case13Documento19 pagineFedillaga Case13Luke Ysmael FedillagaNessuna valutazione finora

- ACCTGBKSDocumento4 pagineACCTGBKSRejed VillanuevaNessuna valutazione finora

- AFARDocumento15 pagineAFARBetchelyn Dagwayan BenignosNessuna valutazione finora

- Calculation For Liquidation Value at Closure Date Is Somewhat Like The Book Value CalculationDocumento3 pagineCalculation For Liquidation Value at Closure Date Is Somewhat Like The Book Value CalculationALYZA ANGELA ORNEDONessuna valutazione finora

- Capstone Theory & ProblemDocumento10 pagineCapstone Theory & ProblemAia SmithNessuna valutazione finora

- Audit of Inventories - Part 1Documento5 pagineAudit of Inventories - Part 1Mark Lawrence YusiNessuna valutazione finora

- VCM Module 7 - Tools Used in Asset-Based Valuation and Asset-Based Valuation MethodsDocumento58 pagineVCM Module 7 - Tools Used in Asset-Based Valuation and Asset-Based Valuation MethodsLaurie Mae ToledoNessuna valutazione finora

- Train Law PDFDocumento27 pagineTrain Law PDFLanieLampasaNessuna valutazione finora

- Assessment Activities Module 1: Intanible AssetsDocumento16 pagineAssessment Activities Module 1: Intanible Assetsaj dumpNessuna valutazione finora

- Review - Practical Accounting 1Documento2 pagineReview - Practical Accounting 1Kath LeynesNessuna valutazione finora

- Zakaria Ch4Documento15 pagineZakaria Ch4Zakaria Hasaneen0% (2)

- Retirement Method and Replacement MethodDocumento1 paginaRetirement Method and Replacement MethodQueenie ValleNessuna valutazione finora

- Auditing Problems SOLUTION v.1 - 2018Documento12 pagineAuditing Problems SOLUTION v.1 - 2018Ramainne RonquilloNessuna valutazione finora

- Chapter 8Documento18 pagineChapter 8Marie Sheaneth BalitangNessuna valutazione finora

- Dockers Inc Proof of CashDocumento1 paginaDockers Inc Proof of CashJoemar LegresoNessuna valutazione finora

- CBS Corporation Purchased 10Documento12 pagineCBS Corporation Purchased 10Stella SabaoanNessuna valutazione finora

- BA 118.1 SME Exercise Set 5Documento1 paginaBA 118.1 SME Exercise Set 5Ian De DiosNessuna valutazione finora

- Problem Set For AR (Ctto)Documento16 pagineProblem Set For AR (Ctto)Mariane Jean Guerrero100% (1)

- Audit ReviewDocumento9 pagineAudit ReviewephraimNessuna valutazione finora

- AP.2904 - Cash and Cash Equivalents - YTDocumento3 pagineAP.2904 - Cash and Cash Equivalents - YTRosevilla AbneNessuna valutazione finora

- I. 1. Acquisition Method: Non-Controlling Interest Consolidated StatementDocumento14 pagineI. 1. Acquisition Method: Non-Controlling Interest Consolidated StatementCookies And CreamNessuna valutazione finora

- Audprob Final Exam 1Documento26 pagineAudprob Final Exam 1Joody CatacutanNessuna valutazione finora

- Assignment 6Documento2 pagineAssignment 6Janeth NavalesNessuna valutazione finora

- LawDocumento43 pagineLawMARIANessuna valutazione finora

- 5 6188442313212035099Documento19 pagine5 6188442313212035099JamieNessuna valutazione finora

- Grace Corporation Confirmation of Bank Balances DECEMBER 31, 20X1Documento2 pagineGrace Corporation Confirmation of Bank Balances DECEMBER 31, 20X1Joshua ComerosNessuna valutazione finora

- Cost-Volume-Profit AnalysisDocumento6 pagineCost-Volume-Profit AnalysisCher NaNessuna valutazione finora

- ACCO 30043: Quiz Number 1 (Introduction To Assurance and Audit Services)Documento16 pagineACCO 30043: Quiz Number 1 (Introduction To Assurance and Audit Services)pat lanceNessuna valutazione finora

- Auditing TheoDocumento27 pagineAuditing TheoSherri BonquinNessuna valutazione finora

- For A Vanishing DeductionDocumento2 pagineFor A Vanishing DeductionJunho ChaNessuna valutazione finora

- Equity Securities (Continuation)Documento1 paginaEquity Securities (Continuation)Melvin MendozaNessuna valutazione finora

- Accounting ReportDocumento19 pagineAccounting ReportEdward Glenn BaguiNessuna valutazione finora

- M1 Introduction To Transfer Taxaion Students PDFDocumento20 pagineM1 Introduction To Transfer Taxaion Students PDFTokis SabaNessuna valutazione finora

- Assessment Current LiabilitiesDocumento6 pagineAssessment Current LiabilitiesEdward Glenn BaguiNessuna valutazione finora

- LEC104-C: Debt Restructuring Problem 1: Asset Swap (IFRS Vs US GAAP)Documento1 paginaLEC104-C: Debt Restructuring Problem 1: Asset Swap (IFRS Vs US GAAP)Miles SantosNessuna valutazione finora

- QUIZ in AUDIT OF SHAREHOLDERS EQUITYDocumento2 pagineQUIZ in AUDIT OF SHAREHOLDERS EQUITYLugh Tuatha DeNessuna valutazione finora

- Audit of Inventory 2021 - ExamDocumento9 pagineAudit of Inventory 2021 - ExammoreNessuna valutazione finora

- INVESTMENTS W Matrix PFRS 9 PDFDocumento7 pagineINVESTMENTS W Matrix PFRS 9 PDFAra DucusinNessuna valutazione finora

- Activity 1 MAS1 AnswersDocumento2 pagineActivity 1 MAS1 Answersangel mae cuevasNessuna valutazione finora

- Semi Final Exam AE23Documento6 pagineSemi Final Exam AE23HotcheeseramyeonNessuna valutazione finora

- APC Ch11sol.2011Documento6 pagineAPC Ch11sol.2011Reymilyn Sanchez100% (2)

- Notes On BP22 Atty. DomingoDocumento2 pagineNotes On BP22 Atty. Domingothalia alfaroNessuna valutazione finora

- Donor's Tax - BirDocumento7 pagineDonor's Tax - BirHannah Brynne UrreraNessuna valutazione finora

- When and Where To FileDocumento3 pagineWhen and Where To FileJessRowelJulianNessuna valutazione finora

- Effective January 1, 2018 and Onwards (Republic Act (RA) No. 10963/TRAIN)Documento3 pagineEffective January 1, 2018 and Onwards (Republic Act (RA) No. 10963/TRAIN)Deneb DoydoraNessuna valutazione finora

- Documentary Stamp Tax, Capital Gains Tax, and Donor's TaxDocumento3 pagineDocumentary Stamp Tax, Capital Gains Tax, and Donor's TaxJoyNessuna valutazione finora

- BIR Form 1800 - Donor's Tax ReturnDocumento2 pagineBIR Form 1800 - Donor's Tax ReturnangelgirlfabNessuna valutazione finora

- Bir Donors Tax QueriesDocumento2 pagineBir Donors Tax QueriesdteroseNessuna valutazione finora

- Estate Tax Is A Tax On The Right of The Deceased Person To Transmit His/her Estate To His/her Lawful Heirs andDocumento4 pagineEstate Tax Is A Tax On The Right of The Deceased Person To Transmit His/her Estate To His/her Lawful Heirs andRey PerosaNessuna valutazione finora

- 1st Quiz-Partnership-rawDocumento3 pagine1st Quiz-Partnership-rawRey PerosaNessuna valutazione finora

- Name: - Course & Year Level: - Date: - Part I: Multiple Choices. Direction: Encircle The Correct Answer. Strictly No Erasure AllowedDocumento2 pagineName: - Course & Year Level: - Date: - Part I: Multiple Choices. Direction: Encircle The Correct Answer. Strictly No Erasure AllowedRey Perosa83% (6)

- Quiz On Taxation-Donor's TaxDocumento2 pagineQuiz On Taxation-Donor's TaxRey PerosaNessuna valutazione finora

- Estate Tax Is A Tax On The Right of The Deceased Person To Transmit His/her Estate To His/her Lawful Heirs andDocumento4 pagineEstate Tax Is A Tax On The Right of The Deceased Person To Transmit His/her Estate To His/her Lawful Heirs andRey PerosaNessuna valutazione finora

- Question #1: Taxation - Donors Tax (Average)Documento8 pagineQuestion #1: Taxation - Donors Tax (Average)Rey PerosaNessuna valutazione finora

- Donor Tax Examples-For DiscussionDocumento2 pagineDonor Tax Examples-For DiscussionRey PerosaNessuna valutazione finora

- Time of SupplyDocumento31 pagineTime of SupplyNalin KNessuna valutazione finora

- Siquaf Trade Paparan PDFDocumento31 pagineSiquaf Trade Paparan PDFsiquaf15Nessuna valutazione finora

- Submitted By: Anmol Hindwani (Pgsf1907) : Bank Performance AnalysisDocumento20 pagineSubmitted By: Anmol Hindwani (Pgsf1907) : Bank Performance AnalysisSurbhî GuptaNessuna valutazione finora

- Application New 2023Documento8 pagineApplication New 2023SFS LOANSNessuna valutazione finora

- Chapter 3 National Income Test BankDocumento45 pagineChapter 3 National Income Test BankmchlbahaaNessuna valutazione finora

- Rubi Verma Mutual Fund and Ulip ReportDocumento92 pagineRubi Verma Mutual Fund and Ulip ReportSadhanaNessuna valutazione finora

- Ugba 101b Test 2 2008Documento12 pagineUgba 101b Test 2 2008Minji KimNessuna valutazione finora

- Beneficiary's (Bailor) Deposit Disbursement Payment Discharge of Contract CloseDocumento5 pagineBeneficiary's (Bailor) Deposit Disbursement Payment Discharge of Contract Closein1or93% (14)

- Task - Payment and Invoice - RONAINDA ARITONANG - 2005081039 - AK4BDocumento12 pagineTask - Payment and Invoice - RONAINDA ARITONANG - 2005081039 - AK4BRonainda AritonangNessuna valutazione finora

- Futures - Meaning, Types, Mechanism, SEBI GuidelinesDocumento49 pagineFutures - Meaning, Types, Mechanism, SEBI GuidelinesKARISHMAAT67% (6)

- CHAPTER 18: Mutual Funds: Types and FeaturesDocumento18 pagineCHAPTER 18: Mutual Funds: Types and Featureslily northNessuna valutazione finora

- What Is EMD in Contract Work - Google SearchDocumento3 pagineWhat Is EMD in Contract Work - Google SearchRanjanNessuna valutazione finora

- True / False Questions: Liquidity RiskDocumento25 pagineTrue / False Questions: Liquidity Risklatifa hnNessuna valutazione finora

- Export Price List 2011-2012 SystemairDocumento312 pagineExport Price List 2011-2012 SystemairCharly ColumbNessuna valutazione finora

- Yes BankDocumento9 pagineYes Bankरायटर लेखनवालाNessuna valutazione finora

- Unit 1Documento92 pagineUnit 1Amrit KaurNessuna valutazione finora

- FXOM Definitions EN PDFDocumento10 pagineFXOM Definitions EN PDFDenni SeptianNessuna valutazione finora

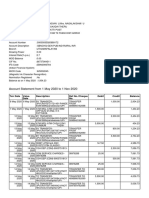

- Account Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento9 pagineAccount Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChellapandiNessuna valutazione finora

- A Report Submitted To Amity International Business School (AIBS)Documento33 pagineA Report Submitted To Amity International Business School (AIBS)IshikaNessuna valutazione finora

- BIR RULING NO. 100-17: SGV & CoDocumento10 pagineBIR RULING NO. 100-17: SGV & CoThe GiverNessuna valutazione finora

- Compensation Income - Fringe Benefit TaxDocumento41 pagineCompensation Income - Fringe Benefit Taxdelacruzrojohn600Nessuna valutazione finora

- MG Freesites LTD.: Za Kasarnou 1, 831 03 Bratislava, SlovakiaDocumento1 paginaMG Freesites LTD.: Za Kasarnou 1, 831 03 Bratislava, Slovakiakundan singhNessuna valutazione finora

- FINA1904 - ALL Weitzel - Spring 2019Documento11 pagineFINA1904 - ALL Weitzel - Spring 2019JamesNessuna valutazione finora

- Fundamentals of Capital StructureDocumento42 pagineFundamentals of Capital StructureSona Singh pgpmx 2017 batch-2Nessuna valutazione finora

- Unit - 3Documento25 pagineUnit - 3ShriHemaRajaNessuna valutazione finora

- WSS 9 Case Studies Blended FinanceDocumento36 pagineWSS 9 Case Studies Blended FinanceAbdullahi Mohamed HusseinNessuna valutazione finora

- Cash Flow StatementDocumento11 pagineCash Flow StatementJonathanKelly Bitonga BargasoNessuna valutazione finora

- 2018 Working Capital Management: Test Code: R38 WCAM Q-BankDocumento6 pagine2018 Working Capital Management: Test Code: R38 WCAM Q-BankMarwa Abd-ElmeguidNessuna valutazione finora

- Macro Exam 2018Documento4 pagineMacro Exam 2018Vignesh BalachandarNessuna valutazione finora

- Punjab & Sind Bank: Jump To Navigationjump To SearchDocumento5 paginePunjab & Sind Bank: Jump To Navigationjump To SearchSakshi BakliwalNessuna valutazione finora

- The Small-Business Guide to Government Contracts: How to Comply with the Key Rules and Regulations . . . and Avoid Terminated Agreements, Fines, or WorseDa EverandThe Small-Business Guide to Government Contracts: How to Comply with the Key Rules and Regulations . . . and Avoid Terminated Agreements, Fines, or WorseNessuna valutazione finora

- How to Win Your Case In Traffic Court Without a LawyerDa EverandHow to Win Your Case In Traffic Court Without a LawyerValutazione: 4 su 5 stelle4/5 (5)

- The Perfect Stage Crew: The Complete Technical Guide for High School, College, and Community TheaterDa EverandThe Perfect Stage Crew: The Complete Technical Guide for High School, College, and Community TheaterNessuna valutazione finora

- Contract Law for Serious Entrepreneurs: Know What the Attorneys KnowDa EverandContract Law for Serious Entrepreneurs: Know What the Attorneys KnowValutazione: 1 su 5 stelle1/5 (1)

- Law of Contract Made Simple for LaymenDa EverandLaw of Contract Made Simple for LaymenValutazione: 4.5 su 5 stelle4.5/5 (9)

- Sales & Marketing Agreements and ContractsDa EverandSales & Marketing Agreements and ContractsNessuna valutazione finora

- Legal Guide to Social Media, Second Edition: Rights and Risks for Businesses, Entrepreneurs, and InfluencersDa EverandLegal Guide to Social Media, Second Edition: Rights and Risks for Businesses, Entrepreneurs, and InfluencersValutazione: 5 su 5 stelle5/5 (1)

- A Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsDa EverandA Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsNessuna valutazione finora

- The Certified Master Contract AdministratorDa EverandThe Certified Master Contract AdministratorValutazione: 5 su 5 stelle5/5 (1)

- Legal Forms for Everyone: Leases, Home Sales, Avoiding Probate, Living Wills, Trusts, Divorce, Copyrights, and Much MoreDa EverandLegal Forms for Everyone: Leases, Home Sales, Avoiding Probate, Living Wills, Trusts, Divorce, Copyrights, and Much MoreValutazione: 3.5 su 5 stelle3.5/5 (2)

- Profitable Photography in Digital Age: Strategies for SuccessDa EverandProfitable Photography in Digital Age: Strategies for SuccessNessuna valutazione finora

- Learn the Essentials of Business Law in 15 DaysDa EverandLearn the Essentials of Business Law in 15 DaysValutazione: 4 su 5 stelle4/5 (13)

- Fundamentals of Theatrical Design: A Guide to the Basics of Scenic, Costume, and Lighting DesignDa EverandFundamentals of Theatrical Design: A Guide to the Basics of Scenic, Costume, and Lighting DesignValutazione: 3.5 su 5 stelle3.5/5 (3)

- Contracts: The Essential Business Desk ReferenceDa EverandContracts: The Essential Business Desk ReferenceValutazione: 4 su 5 stelle4/5 (15)

- Digital Technical Theater Simplified: High Tech Lighting, Audio, Video and More on a Low BudgetDa EverandDigital Technical Theater Simplified: High Tech Lighting, Audio, Video and More on a Low BudgetNessuna valutazione finora

- How to Win Your Case in Small Claims Court Without a LawyerDa EverandHow to Win Your Case in Small Claims Court Without a LawyerValutazione: 5 su 5 stelle5/5 (1)