Potrebbero piacerti anche

- Represented by Group IDocumento22 pagineRepresented by Group IUsman FarooqNessuna valutazione finora

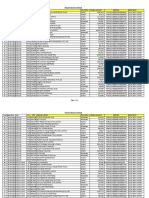

- Askari Bank Limited: S.No Date RCVD Colt Sr. NTN Exporter - Name City - Name Cheque Amount Iban No. Bank NameDocumento6 pagineAskari Bank Limited: S.No Date RCVD Colt Sr. NTN Exporter - Name City - Name Cheque Amount Iban No. Bank NameUsman FarooqNessuna valutazione finora

- Transparent Objects Allow You To See Clearly Through Them. Some Examples AreDocumento4 pagineTransparent Objects Allow You To See Clearly Through Them. Some Examples AreUsman FarooqNessuna valutazione finora

- Chapter 4 QuestionsDocumento4 pagineChapter 4 QuestionsUsman FarooqNessuna valutazione finora

- The Collapse of Mayan Civilization:: Middleton, 2012)Documento4 pagineThe Collapse of Mayan Civilization:: Middleton, 2012)Usman FarooqNessuna valutazione finora

- Additional Information WEEK 4 MNG91217 SP42017Documento3 pagineAdditional Information WEEK 4 MNG91217 SP42017Usman FarooqNessuna valutazione finora

- Askari Bank LTD: S.No. Date RCVD Colt Sr. NTN Exporter - Name City - Name Cheque Amount Iban No. Bank NameDocumento1 paginaAskari Bank LTD: S.No. Date RCVD Colt Sr. NTN Exporter - Name City - Name Cheque Amount Iban No. Bank NameUsman FarooqNessuna valutazione finora

- Week 5 Discussion Topic 3 Chapter 14Documento1 paginaWeek 5 Discussion Topic 3 Chapter 14Usman FarooqNessuna valutazione finora

- Calgary, Between The Soccer Practices and The Hours at Her Accounting JobDocumento24 pagineCalgary, Between The Soccer Practices and The Hours at Her Accounting JobUsman FarooqNessuna valutazione finora

- Writing Assignment Guidelines - AMH3540, Spring 2017Documento3 pagineWriting Assignment Guidelines - AMH3540, Spring 2017Usman FarooqNessuna valutazione finora

- 5 SensesDocumento11 pagine5 SensesUsman FarooqNessuna valutazione finora

- Homework XiDocumento4 pagineHomework XiUsman FarooqNessuna valutazione finora

- ,please Read: 1. " ," 2. in An Essay of Total, Respond To The Five "Case Questions" at The End of The PassageDocumento1 pagina,please Read: 1. " ," 2. in An Essay of Total, Respond To The Five "Case Questions" at The End of The PassageUsman FarooqNessuna valutazione finora

- Tax Collector Correspondence3740504158331Documento1 paginaTax Collector Correspondence3740504158331Usman FarooqNessuna valutazione finora

- Mbae PDFDocumento2 pagineMbae PDFUsman FarooqNessuna valutazione finora

- KenyaDocumento1 paginaKenyaUsman FarooqNessuna valutazione finora

- Timetable For Fall 2019: Monday Tuesday Wednesday Thursday Friday SaturdayDocumento2 pagineTimetable For Fall 2019: Monday Tuesday Wednesday Thursday Friday SaturdayUsman FarooqNessuna valutazione finora

- Master List of Companies Participating in Job Fair 2018 PDFDocumento144 pagineMaster List of Companies Participating in Job Fair 2018 PDFUsman FarooqNessuna valutazione finora

- 1 Forecasting-QuestionsDocumento4 pagine1 Forecasting-QuestionsUsman FarooqNessuna valutazione finora

- Country Analysis of Kenya For Detergents MarketDocumento1 paginaCountry Analysis of Kenya For Detergents MarketUsman FarooqNessuna valutazione finora

- HDI Lecture ContinuedDocumento4 pagineHDI Lecture ContinuedUsman FarooqNessuna valutazione finora

- Monday Tuesday Wednesday Thursday Friday Saturday: Timetable For Fall 2019Documento2 pagineMonday Tuesday Wednesday Thursday Friday Saturday: Timetable For Fall 2019Usman FarooqNessuna valutazione finora

- Interview Based Reflection Report: 1. LeadershipDocumento9 pagineInterview Based Reflection Report: 1. LeadershipUsman FarooqNessuna valutazione finora

- Inventory and Ordering DecisionsDocumento2 pagineInventory and Ordering DecisionsUsman FarooqNessuna valutazione finora

- Supply Chain DecisionsDocumento2 pagineSupply Chain DecisionsUsman FarooqNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Darshan Institute of Engineering & Technology Unit: 7Documento9 pagineDarshan Institute of Engineering & Technology Unit: 7AarshenaNessuna valutazione finora

- Science Fiction FilmsDocumento5 pagineScience Fiction Filmsapi-483055750Nessuna valutazione finora

- Girl: Dad, I Need A Few Supplies For School, and I Was Wondering If - . .Documento3 pagineGirl: Dad, I Need A Few Supplies For School, and I Was Wondering If - . .AKSHATNessuna valutazione finora

- Automated Long-Distance HADR ConfigurationsDocumento73 pagineAutomated Long-Distance HADR ConfigurationsKan DuNessuna valutazione finora

- Development of A Single Axis Tilting QuadcopterDocumento4 pagineDevelopment of A Single Axis Tilting QuadcopterbasavasagarNessuna valutazione finora

- AVEVA Work Permit ManagerDocumento2 pagineAVEVA Work Permit ManagerMohamed Refaat100% (1)

- Strengthsfinder Sept GBMDocumento32 pagineStrengthsfinder Sept GBMapi-236473176Nessuna valutazione finora

- Role LibrariesDocumento57 pagineRole LibrariesGiovanni AnggastaNessuna valutazione finora

- Bad SenarioDocumento19 pagineBad SenarioHussain ElboshyNessuna valutazione finora

- Exposicion Verbos y AdverbiosDocumento37 pagineExposicion Verbos y AdverbiosmonicaNessuna valutazione finora

- Financial Vs Health and Safety Vs Reputation Vs Opportunity CostsDocumento11 pagineFinancial Vs Health and Safety Vs Reputation Vs Opportunity Costschanlego123Nessuna valutazione finora

- Detailed Lesson Plan in PED 12Documento10 pagineDetailed Lesson Plan in PED 12alcomfeloNessuna valutazione finora

- Dubai TalesDocumento16 pagineDubai Talesbooksarabia100% (2)

- Gian Lorenzo BerniniDocumento12 pagineGian Lorenzo BerniniGiulia Galli LavigneNessuna valutazione finora

- Feb 1 - ScottDocumento17 pagineFeb 1 - ScottNyannnNessuna valutazione finora

- Virtual Verde Release Plan Emails: Email 1Documento4 pagineVirtual Verde Release Plan Emails: Email 1Violet StarNessuna valutazione finora

- Imam Zainul Abideen (RA) 'S Service To The Poor and DestituteDocumento3 pagineImam Zainul Abideen (RA) 'S Service To The Poor and DestituteShoyab11Nessuna valutazione finora

- Shostakovich: Symphony No. 13Documento16 pagineShostakovich: Symphony No. 13Bol DigNessuna valutazione finora

- Chargezoom Achieves PCI-DSS ComplianceDocumento2 pagineChargezoom Achieves PCI-DSS CompliancePR.comNessuna valutazione finora

- What Does The Scripture Say - ' - Studies in The Function of Scripture in Early Judaism and Christianity, Volume 1 - The Synoptic GospelsDocumento149 pagineWhat Does The Scripture Say - ' - Studies in The Function of Scripture in Early Judaism and Christianity, Volume 1 - The Synoptic GospelsCometa Halley100% (1)

- LDS Conference Report 1930 Semi AnnualDocumento148 pagineLDS Conference Report 1930 Semi AnnualrjjburrowsNessuna valutazione finora

- Lost Secrets of Baseball HittingDocumento7 pagineLost Secrets of Baseball HittingCoach JPNessuna valutazione finora

- Cloze Tests 2Documento8 pagineCloze Tests 2Tatjana StijepovicNessuna valutazione finora

- PctcostepoDocumento4 paginePctcostepoRyan Frikkin MurgaNessuna valutazione finora

- Reading Listening 2Documento5 pagineReading Listening 2Lisbet GomezNessuna valutazione finora

- Music Education (Kodaly Method)Documento4 pagineMusic Education (Kodaly Method)Nadine van Dyk100% (2)

- EP105Use of English ArantxaReynosoDocumento6 pagineEP105Use of English ArantxaReynosoArantxaSteffiNessuna valutazione finora

- Definition Environmental Comfort in IdDocumento43 pagineDefinition Environmental Comfort in Idharis hambaliNessuna valutazione finora

- MC2 Sewing Patterns: Dressmaking Learning ModuleDocumento91 pagineMC2 Sewing Patterns: Dressmaking Learning ModuleMargie JariñoNessuna valutazione finora

- The Acceptability of Indian Mango Leaves Powdered As A Tea: (Mangifera Indica Linn.)Documento22 pagineThe Acceptability of Indian Mango Leaves Powdered As A Tea: (Mangifera Indica Linn.)Marissa M. DoriaNessuna valutazione finora