Potrebbero piacerti anche

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Title:Walt Disney Company Case Study: Zoe (范氏黃英) 1 and 2 year of Department of International BusinessDocumento115 pagineTitle:Walt Disney Company Case Study: Zoe (范氏黃英) 1 and 2 year of Department of International BusinessPam PalonponNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Walt DisneyDocumento2 pagineWalt DisneyPam Palonpon100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Walt DisneyDocumento2 pagineWalt DisneyPam PalonponNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- PALONPON Pamela Joy G. - VP For Membership - SEC 3Documento3 paginePALONPON Pamela Joy G. - VP For Membership - SEC 3Pam PalonponNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Documento5 pagineStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- 115 Chapter 15 RaibornDocumento24 pagine115 Chapter 15 RaibornVictoria CadizNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- SChedule VIDocumento88 pagineSChedule VIbhushan2011Nessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- ACC 178 SAS Module 25Documento14 pagineACC 178 SAS Module 25maria isayNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Corporations: Earnings & Profits and Dividend DistributionsDocumento54 pagineCorporations: Earnings & Profits and Dividend DistributionseasyNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

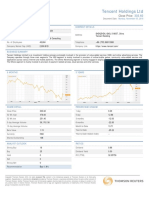

- Tencent Holdings LTD: Close PriceDocumento2 pagineTencent Holdings LTD: Close PricetrungNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Stock Trading ChallengeDocumento9 pagineStock Trading ChallengeMiguel MartinezNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Top 300 PEIDocumento8 pagineTop 300 PEIJerome OngNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Test Bank For Introduction To Governmental and Not For Profit Accounting 7th Edition by Ives DownloadDocumento19 pagineTest Bank For Introduction To Governmental and Not For Profit Accounting 7th Edition by Ives DownloadTeresaMoorecsrby100% (43)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- MANACC Chapter19Documento3 pagineMANACC Chapter19You DontknowmeNessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- MSR 40000 Gid 20009265 403 20220627 1 008Documento5 pagineMSR 40000 Gid 20009265 403 20220627 1 008Burn4 YouNessuna valutazione finora

- Korteweg FBE 432: Corporate Financial Strategy Spring 2017Documento6 pagineKorteweg FBE 432: Corporate Financial Strategy Spring 2017PeterNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Name Suhail Abdul Rashid TankeDocumento9 pagineName Suhail Abdul Rashid TankeIram ParkarNessuna valutazione finora

- AdvancedDocumento8 pagineAdvancedElaine YapNessuna valutazione finora

- MODULE 3 CVP ANALYSIS - GROUP 2 AE6 Strategic Business AnalysisDocumento5 pagineMODULE 3 CVP ANALYSIS - GROUP 2 AE6 Strategic Business AnalysisJaime PalizardoNessuna valutazione finora

- Fin401, Corporate Finance PDFDocumento3 pagineFin401, Corporate Finance PDFKRZ. Arpon Root HackerNessuna valutazione finora

- Financial Statements Unsolved PDFDocumento4 pagineFinancial Statements Unsolved PDFMark Dave SambranoNessuna valutazione finora

- Accounting 2Documento3 pagineAccounting 2Minas SydNessuna valutazione finora

- Square Pharma Annual Report 2020 2021Documento4 pagineSquare Pharma Annual Report 2020 2021Mehedi HassanNessuna valutazione finora

- Corporate Financing Decisions and Efficient Capital MarketsDocumento53 pagineCorporate Financing Decisions and Efficient Capital MarketsalexanderNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Nism 8 - Equity Derivatives - Test-1 - Last Day RevisionDocumento54 pagineNism 8 - Equity Derivatives - Test-1 - Last Day RevisionAbhijeet Kumar100% (1)

- TEST Paper 1 Full TestDocumento9 pagineTEST Paper 1 Full Testjohny SahaNessuna valutazione finora

- Invesrment in Debt InstrumentsDocumento2 pagineInvesrment in Debt InstrumentsElla MontefalcoNessuna valutazione finora

- Hilton Black Stone CaseDocumento13 pagineHilton Black Stone CaseAman Baweja100% (1)

- FI Asset Configuration - S4 Hana Enterprise Mangement PDFDocumento83 pagineFI Asset Configuration - S4 Hana Enterprise Mangement PDFbrcraoNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- 2010 LCCI Level 3 Series 2 Question Paper (Code 3012)Documento8 pagine2010 LCCI Level 3 Series 2 Question Paper (Code 3012)mappymappymappyNessuna valutazione finora

- Chuck Akre Value Investing Conference TalkDocumento21 pagineChuck Akre Value Investing Conference TalkMarc F. DemshockNessuna valutazione finora

- Inkp Annual Report 2016Documento226 pagineInkp Annual Report 2016anon_854349151Nessuna valutazione finora

- Consumers Product Analysis PresentationDocumento6 pagineConsumers Product Analysis PresentationUmar HarizNessuna valutazione finora

- Tarea 2 Bis Caso Hemingway CorporationDocumento10 pagineTarea 2 Bis Caso Hemingway CorporationChesse HerNessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)