Potrebbero piacerti anche

- Mathematical Association of AmericaDocumento4 pagineMathematical Association of AmericaMonal BhoyarNessuna valutazione finora

- Multi-Asset Options: 4.1 Pricing ModelDocumento10 pagineMulti-Asset Options: 4.1 Pricing ModeldownloadfromscribdNessuna valutazione finora

- ExercisesDocumento11 pagineExercisestomrannosaurusNessuna valutazione finora

- Final PPT IE612 - Financial EngineeringDocumento16 pagineFinal PPT IE612 - Financial EngineeringHey BuddyNessuna valutazione finora

- Edition Don Chance and Robert Brooks Technical Note: Probability of Call Expiring In-The-Money, Ch. 5, P. 138Documento3 pagineEdition Don Chance and Robert Brooks Technical Note: Probability of Call Expiring In-The-Money, Ch. 5, P. 138sidhanthaNessuna valutazione finora

- The Black Scholes Model-2Documento58 pagineThe Black Scholes Model-2Gladys Gladys MakNessuna valutazione finora

- Mathematical Modelling and Financial Engineering in The Worlds Stock MarketsDocumento7 pagineMathematical Modelling and Financial Engineering in The Worlds Stock MarketsVijay ParmarNessuna valutazione finora

- Power-Law Decay in First-Order Relaxation ProcessesDocumento21 paginePower-Law Decay in First-Order Relaxation ProcessesrumiNessuna valutazione finora

- Studia Univ. "Babes - BOLYAI", MATHEMATICA, Volume, Number 3, September 2003Documento10 pagineStudia Univ. "Babes - BOLYAI", MATHEMATICA, Volume, Number 3, September 2003FernandoFierroGonzalezNessuna valutazione finora

- Vanderpol Oscillator DraftDocumento7 pagineVanderpol Oscillator DraftRicardo SimãoNessuna valutazione finora

- FinMath Lecture 7 Black-ScholesDocumento30 pagineFinMath Lecture 7 Black-ScholesavirgNessuna valutazione finora

- DerivativesDocumento26 pagineDerivativesKavyaNessuna valutazione finora

- Volatility Swap Under The SABR Model: Simon Bossoney March 26, 2013Documento10 pagineVolatility Swap Under The SABR Model: Simon Bossoney March 26, 2013Melissa AyquipaNessuna valutazione finora

- 1 Estimating Uncertainties and Propagation of Errors: Physics 326, Final ExamDocumento4 pagine1 Estimating Uncertainties and Propagation of Errors: Physics 326, Final ExamJack BotNessuna valutazione finora

- 6 Difference Equations: 6.1 Comparison To ODE and GeneralitiesDocumento13 pagine6 Difference Equations: 6.1 Comparison To ODE and GeneralitiesYanira EspinozaNessuna valutazione finora

- Application of Derivatives: 6.1 Overview 6.1.1Documento26 pagineApplication of Derivatives: 6.1 Overview 6.1.1Yashpal MishraNessuna valutazione finora

- Known Closed Forms For QuantsDocumento12 pagineKnown Closed Forms For Quantsapi-3729160100% (1)

- The Black-Scholes Model: Liuren WuDocumento17 pagineThe Black-Scholes Model: Liuren WuSoni SukendarNessuna valutazione finora

- 1 20 Ito Calculus and BoydDocumento10 pagine1 20 Ito Calculus and BoydshrutigarodiaNessuna valutazione finora

- ITO'S LEMMADocumento7 pagineITO'S LEMMAsambhu_nNessuna valutazione finora

- Lectura 2 Point Estimator BasicsDocumento11 pagineLectura 2 Point Estimator BasicsAlejandro MarinNessuna valutazione finora

- A Non-Linear Black-Scholes EquationDocumento8 pagineA Non-Linear Black-Scholes EquationHadiBiesNessuna valutazione finora

- Powerpoint FinallllllllllpdfDocumento32 paginePowerpoint FinallllllllllpdfPrincess Morales TyNessuna valutazione finora

- Modification of Black-Scholes Model: 7.1 DividendDocumento9 pagineModification of Black-Scholes Model: 7.1 Dividendcharles luisNessuna valutazione finora

- How To Make Dupire's Local Volatility Work With Jumps: 1 Failure of Dupire's Formula in Non-Diffusion SettingDocumento7 pagineHow To Make Dupire's Local Volatility Work With Jumps: 1 Failure of Dupire's Formula in Non-Diffusion SettingtjjnycNessuna valutazione finora

- The Analysis of Black-Scholes Option Pricing: Wen-Li Tang, Liang-Rong SongDocumento5 pagineThe Analysis of Black-Scholes Option Pricing: Wen-Li Tang, Liang-Rong SongDinesh KumarNessuna valutazione finora

- Black Scholes DerivationDocumento19 pagineBlack Scholes DerivationBrandon LockNessuna valutazione finora

- 5021 Solutions 10Documento7 pagine5021 Solutions 10belenhostNessuna valutazione finora

- MathEcon17 FinalExam SolutionDocumento13 pagineMathEcon17 FinalExam SolutionCours HECNessuna valutazione finora

- Weatherwax Wilmott SolutionsDocumento224 pagineWeatherwax Wilmott Solutionsalanpicard2303Nessuna valutazione finora

- Chi SquareDocumento6 pagineChi Squarehammoudeh13Nessuna valutazione finora

- Elementary Differential Equations: Notice: This Material Must Not Be Used As A Substitute For Attending The LecturesDocumento34 pagineElementary Differential Equations: Notice: This Material Must Not Be Used As A Substitute For Attending The LecturesDelvina HartrianaNessuna valutazione finora

- Asymptotic Expansions of The Lognormal Implied Volatility: A Model Free ApproachDocumento18 pagineAsymptotic Expansions of The Lognormal Implied Volatility: A Model Free ApproachAidan HolwerdaNessuna valutazione finora

- Assignment 5 Mathematical FinanceDocumento3 pagineAssignment 5 Mathematical FinanceYuengNessuna valutazione finora

- Analytic Solution of Nonlinear Black-Scholes EquationDocumento10 pagineAnalytic Solution of Nonlinear Black-Scholes Equationjawad HussainNessuna valutazione finora

- Solution of Wave EquationDocumento7 pagineSolution of Wave Equationjeetendra222523Nessuna valutazione finora

- Math Finance Chap - 6 - Stochastic Volatility Slides 26-03-10Documento15 pagineMath Finance Chap - 6 - Stochastic Volatility Slides 26-03-10seth_tolevNessuna valutazione finora

- FIN4110 Options and Futures S2, 2023 Topic 7Documento69 pagineFIN4110 Options and Futures S2, 2023 Topic 7Shuen WuNessuna valutazione finora

- QuantoDocumento21 pagineQuantoRanjit KumarNessuna valutazione finora

- Topics in Financial Mathematics: VAN VramidiDocumento35 pagineTopics in Financial Mathematics: VAN Vramidipsrvarma3755Nessuna valutazione finora

- MCS Framework FEegsDocumento10 pagineMCS Framework FEegsbarisari2Nessuna valutazione finora

- Curve sketching and analysisDocumento3 pagineCurve sketching and analysisZach FergerNessuna valutazione finora

- 18-Application of Derivative-02 - Solved ExampleDocumento18 pagine18-Application of Derivative-02 - Solved ExampleRaju SinghNessuna valutazione finora

- FE - Ch01 Wiener ProcessDocumento15 pagineFE - Ch01 Wiener ProcessMario ZamoraNessuna valutazione finora

- CH 2Documento5 pagineCH 2z_k_j_vNessuna valutazione finora

- Corr Risk With Spread OptionDocumento61 pagineCorr Risk With Spread Optionm325075Nessuna valutazione finora

- Monte Carlo TechniquesDocumento10 pagineMonte Carlo TechniquesMobeen AhmadNessuna valutazione finora

- Black Scholes PDEDocumento7 pagineBlack Scholes PDEmeleeisleNessuna valutazione finora

- Chapter 7 Applications of DifferentiationDocumento14 pagineChapter 7 Applications of Differentiationapi-3728615Nessuna valutazione finora

- TurnerDocumento14 pagineTurnerRENJiiiNessuna valutazione finora

- Tree SchemeDocumento26 pagineTree SchemehollowkenshinNessuna valutazione finora

- The Black-Scholes Formula ExplainedDocumento14 pagineThe Black-Scholes Formula ExplainedAhsan JavedNessuna valutazione finora

- Weather Wax Wilmott SolutionsDocumento217 pagineWeather Wax Wilmott SolutionsPaul K.Nessuna valutazione finora

- Chapter 02Documento10 pagineChapter 02seanwu95Nessuna valutazione finora

- Numerical Solution of Stochastic Differential Equations in FinanceDocumento22 pagineNumerical Solution of Stochastic Differential Equations in FinanceMarion KarloNessuna valutazione finora

- Green's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)Da EverandGreen's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)Nessuna valutazione finora

- Mathematics 1St First Order Linear Differential Equations 2Nd Second Order Linear Differential Equations Laplace Fourier Bessel MathematicsDa EverandMathematics 1St First Order Linear Differential Equations 2Nd Second Order Linear Differential Equations Laplace Fourier Bessel MathematicsNessuna valutazione finora

- Asia's Wealth Gap Is Among The Largest in The World - What Can Leaders Do To Fix ItDocumento13 pagineAsia's Wealth Gap Is Among The Largest in The World - What Can Leaders Do To Fix Itnby949Nessuna valutazione finora

- Mahatma Gandhi's PhilosophyDocumento5 pagineMahatma Gandhi's Philosophynby949Nessuna valutazione finora

- Mathematics Through Paper FoldingDocumento31 pagineMathematics Through Paper FoldingDcStrokerehabNessuna valutazione finora

- 00 - Work With Images in Adobe ReaderDocumento3 pagine00 - Work With Images in Adobe Readernby949Nessuna valutazione finora

- About Us - Startup GenomeDocumento2 pagineAbout Us - Startup Genomenby949Nessuna valutazione finora

- What I Learned by Teaching Real AnalysisDocumento3 pagineWhat I Learned by Teaching Real AnalysisB.y. NgNessuna valutazione finora

- Chelation Therapy For Heart Disease - Does It Work - Mayo ClinicDocumento2 pagineChelation Therapy For Heart Disease - Does It Work - Mayo Clinicnby949Nessuna valutazione finora

- Sample Recommendation LettersDocumento16 pagineSample Recommendation Letterskuttybecse67% (3)

- Practical Tips For Teaching Large Classes: A Teacher's GuideDocumento66 paginePractical Tips For Teaching Large Classes: A Teacher's GuideVeroNessuna valutazione finora

- Professional Development Module On Active Learning: PurposeDocumento8 pagineProfessional Development Module On Active Learning: Purposenby949100% (1)

- AKEPT DrBiggsnTang 23022010 1Documento18 pagineAKEPT DrBiggsnTang 23022010 1nby949Nessuna valutazione finora

- Three Adult Learning TheoriesDocumento8 pagineThree Adult Learning TheoriesIvan Zy LimNessuna valutazione finora

- CH 1 Test BankDocumento17 pagineCH 1 Test BankShiko TharwatNessuna valutazione finora

- The Cost of Capital ExplainedDocumento56 pagineThe Cost of Capital ExplainedAndayani SalisNessuna valutazione finora

- Sample of Corporation PapersDocumento102 pagineSample of Corporation PaperstopguncreditrepairllcNessuna valutazione finora

- GSE Renewables India PVT LTD PDFDocumento24 pagineGSE Renewables India PVT LTD PDFrakeshNessuna valutazione finora

- Corporate Finance OverviewDocumento12 pagineCorporate Finance Overviewadi809hereNessuna valutazione finora

- Bulgaria's Commerce ActDocumento219 pagineBulgaria's Commerce Actswenswen100% (1)

- Tawara Yacht Brokers: Draft Report By: Mai Ahmed BarakatDocumento3 pagineTawara Yacht Brokers: Draft Report By: Mai Ahmed BarakatMay swiftNessuna valutazione finora

- Usefulness of AccountingDocumento17 pagineUsefulness of AccountingMochamadMaarifNessuna valutazione finora

- Forex QuotationsDocumento13 pagineForex QuotationsKamalSoniNessuna valutazione finora

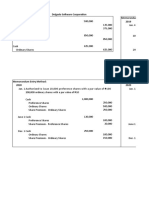

- Memorandum and Journal Entry Methods for Share Capital TransactionsDocumento3 pagineMemorandum and Journal Entry Methods for Share Capital TransactionsFeiya Liu100% (1)

- 2006 CDN Real Estate Industry 020806 REV2Documento268 pagine2006 CDN Real Estate Industry 020806 REV2pankaj_pandey_21Nessuna valutazione finora

- National Pension System (NPS) Subscriber Registration FormDocumento2 pagineNational Pension System (NPS) Subscriber Registration Formkumarvaibhav301745Nessuna valutazione finora

- Earnest Money, Security Deosit and Retention MoneyDocumento8 pagineEarnest Money, Security Deosit and Retention MoneyRushabh Ajmera100% (3)

- Quant Dynamic Fund DetailsDocumento2 pagineQuant Dynamic Fund DetailsAbhishek KumarNessuna valutazione finora

- Types of Market TransactionsDocumento4 pagineTypes of Market Transactionsvinayjain221100% (2)

- Core Lbo ModelDocumento25 pagineCore Lbo Modelsalman_schonNessuna valutazione finora

- Law Project - The Negotiable Instrument Act - RevisedV1Documento48 pagineLaw Project - The Negotiable Instrument Act - RevisedV1Teena Varma100% (3)

- Space MatrixDocumento9 pagineSpace MatrixKrisca DepalubosNessuna valutazione finora

- Starbucks Analylsis 2Documento26 pagineStarbucks Analylsis 2api-321188189Nessuna valutazione finora

- BCG MatrixDocumento14 pagineBCG Matrixamits797Nessuna valutazione finora

- Mutual FundDocumento68 pagineMutual Fundgyanprakashdeb302100% (1)

- Bastida v. Menzi and Co.Documento2 pagineBastida v. Menzi and Co.Crisanta Leonor ChianpianNessuna valutazione finora

- Financial Analysis of National FoodDocumento24 pagineFinancial Analysis of National FoodArslan NawazNessuna valutazione finora

- Standard Balance Sheet PT Cahaya AdamDocumento1 paginaStandard Balance Sheet PT Cahaya AdamAdam Al MukhaffiNessuna valutazione finora

- Drafting, Registration, Stamping HandbookDocumento89 pagineDrafting, Registration, Stamping HandbookramdeenNessuna valutazione finora

- Corpo ReviewerDocumento62 pagineCorpo ReviewerLorelie Sakiwat VargasNessuna valutazione finora

- Greater Rochester 40 Under 40 African American LeadersDocumento48 pagineGreater Rochester 40 Under 40 African American LeadersMessenger Post MediaNessuna valutazione finora

- 1-The Following Table Shows The Sex of The Respondents Sex Respondents PercentageDocumento36 pagine1-The Following Table Shows The Sex of The Respondents Sex Respondents Percentageletter2lalNessuna valutazione finora

- Dep KeyDocumento2 pagineDep Keyanilkg53Nessuna valutazione finora