Potrebbero piacerti anche

- Marketing Plan11Documento15 pagineMarketing Plan11Jae Lani Macaya Resultan91% (11)

- Union Budget 2019-20: July 5, 2019Documento19 pagineUnion Budget 2019-20: July 5, 2019majhiajitNessuna valutazione finora

- Budget 2021-2022: by Y. NikhileshwaraDocumento2 pagineBudget 2021-2022: by Y. NikhileshwaraNarayan AgrawalNessuna valutazione finora

- Fiscal Policy 2020 Introduction To Fiscal PolicyDocumento8 pagineFiscal Policy 2020 Introduction To Fiscal PolicyMamata SreenivasNessuna valutazione finora

- Fiscal Deficit InfoDocumento12 pagineFiscal Deficit InfoSanket AiyaNessuna valutazione finora

- Budget ResearchDocumento28 pagineBudget ResearchPramod KumarNessuna valutazione finora

- Indian Union Budget 2020Documento11 pagineIndian Union Budget 2020Md DhaniyalNessuna valutazione finora

- Single Biggest Challenge India Faces With Respect To Macro-EconomicsDocumento3 pagineSingle Biggest Challenge India Faces With Respect To Macro-EconomicsAnonymous K8h21n5dNessuna valutazione finora

- BudgetDocumento50 pagineBudgetPankajBhardwajNessuna valutazione finora

- GDP Growth Sustained: Total Expenditure Has Increased by Rs. 192669 Crore in 2016-17 (BE) From 2015-16 (RE)Documento4 pagineGDP Growth Sustained: Total Expenditure Has Increased by Rs. 192669 Crore in 2016-17 (BE) From 2015-16 (RE)Aryan DeepNessuna valutazione finora

- Driving Growth Union Budget 2023 24Documento25 pagineDriving Growth Union Budget 2023 24shwetaNessuna valutazione finora

- Economics Assignment ON: Submitted To: Sunrita ChaudhuriDocumento13 pagineEconomics Assignment ON: Submitted To: Sunrita ChaudhuriReshma MohanNessuna valutazione finora

- Fiscal Situation of PakistanDocumento9 pagineFiscal Situation of PakistanMahnoor ZebNessuna valutazione finora

- Budget 2019-2020Documento16 pagineBudget 2019-2020Sidhi SoodNessuna valutazione finora

- Indian Budget 2018: Rejig in Income Tax SlabsDocumento2 pagineIndian Budget 2018: Rejig in Income Tax Slabsnarendra_pNessuna valutazione finora

- Money and Credit: TH THDocumento8 pagineMoney and Credit: TH THsam dinNessuna valutazione finora

- Peoples Views On BudgetDocumento4 paginePeoples Views On BudgetAnkita AgarwalNessuna valutazione finora

- Budget 2011-12 - Analysis: Tax ProjectDocumento19 pagineBudget 2011-12 - Analysis: Tax ProjectSaurabh SadaniNessuna valutazione finora

- Budget 2011Documento2 pagineBudget 2011Tushar SharmaNessuna valutazione finora

- Budget 2009Documento7 pagineBudget 2009akashNessuna valutazione finora

- Impact of Covid-19 On Indian Economy: An Analysis of Fiscal ScenariosDocumento15 pagineImpact of Covid-19 On Indian Economy: An Analysis of Fiscal ScenariosANIRUDHNessuna valutazione finora

- ICAI JournalDocumento121 pagineICAI Journalamitkhera786Nessuna valutazione finora

- A Pragmatic, Multifaceted BudgetDocumento49 pagineA Pragmatic, Multifaceted Budgetmaddy_naik_07Nessuna valutazione finora

- Ana ProjectDocumento84 pagineAna Project622721987Nessuna valutazione finora

- BUDGET ImpactDocumento13 pagineBUDGET ImpactAnonymous 2UkkQDNessuna valutazione finora

- Preface English 2020Documento3 paginePreface English 2020M Tariqul Islam MishuNessuna valutazione finora

- Interim Budget 2019: Submitted By: Harshwardhan Prajapati Ic-2k14-18Documento10 pagineInterim Budget 2019: Submitted By: Harshwardhan Prajapati Ic-2k14-18Anshika Rai0% (1)

- Analysing Budget 2009-10Documento3 pagineAnalysing Budget 2009-10muhammadasifrashidNessuna valutazione finora

- Budget 2010 Review: India-An Economic OverviewDocumento6 pagineBudget 2010 Review: India-An Economic OverviewAIMS_2010Nessuna valutazione finora

- Major Schemes: New Scheme-Namely "Pradhan Mantri Kisan Samman Nidhi (Pm-Kisan) " To Extend ToDocumento42 pagineMajor Schemes: New Scheme-Namely "Pradhan Mantri Kisan Samman Nidhi (Pm-Kisan) " To Extend ToPrakharesh AwasthiNessuna valutazione finora

- Getting To The Core: Budget AnalysisDocumento37 pagineGetting To The Core: Budget AnalysisfaizanbhamlaNessuna valutazione finora

- Budget 2017Documento3 pagineBudget 2017Saba AminNessuna valutazione finora

- PKF Budget Precis 2021-22Documento46 paginePKF Budget Precis 2021-22Arslan HamzaNessuna valutazione finora

- Gaining Insights: Budget Analysis 2010Documento40 pagineGaining Insights: Budget Analysis 2010Shashank ShekharNessuna valutazione finora

- Budget Main PagesDocumento43 pagineBudget Main Pagesneha16septNessuna valutazione finora

- Key Highlights of Economic Survey 2020Documento5 pagineKey Highlights of Economic Survey 2020Shubham SehgalNessuna valutazione finora

- Fiscal DevelopmentDocumento18 pagineFiscal DevelopmentTushar Malik 8Nessuna valutazione finora

- Budget 2010-11: A Deft Balancing Act: Mumbai: Given The Political Constraints and The Fledgling Nature of TheDocumento4 pagineBudget 2010-11: A Deft Balancing Act: Mumbai: Given The Political Constraints and The Fledgling Nature of Thepremkumar7Nessuna valutazione finora

- Interim Union Budget 2019-20 - Budget Review-4 Feb 2019Documento11 pagineInterim Union Budget 2019-20 - Budget Review-4 Feb 2019Anuj SaxenaNessuna valutazione finora

- Federal Budget 2021-22: A Review of Key FactorsDocumento4 pagineFederal Budget 2021-22: A Review of Key FactorsInstitute of Policy StudiesNessuna valutazione finora

- Macroeconomic PolicyDocumento6 pagineMacroeconomic Policyrakibul hasanNessuna valutazione finora

- Budget 2024 25 Summary 1706888004Documento20 pagineBudget 2024 25 Summary 1706888004scientist xyzNessuna valutazione finora

- India - Economic Growth and Development: Market SizeDocumento3 pagineIndia - Economic Growth and Development: Market SizeVIRAJ MALOHTRANessuna valutazione finora

- India, A Bright Spot in Today's WorldDocumento3 pagineIndia, A Bright Spot in Today's WorldAditya KarNessuna valutazione finora

- Indian EconomyDocumento38 pagineIndian EconomyIQAC VMDCNessuna valutazione finora

- Market Strategy: February 2021Documento19 pagineMarket Strategy: February 2021Harshvardhan SurekaNessuna valutazione finora

- GBP - Economic Analysis - Project-GROUP 10Documento10 pagineGBP - Economic Analysis - Project-GROUP 10788 HaswanthNessuna valutazione finora

- Union Budget 2019-20Documento19 pagineUnion Budget 2019-20shweta meshramNessuna valutazione finora

- Pakistan Economic ReviewDocumento3 paginePakistan Economic Reviewanum khurshidNessuna valutazione finora

- India Union BudgetDocumento12 pagineIndia Union BudgetMd DhaniyalNessuna valutazione finora

- Current Affairs 03Documento4 pagineCurrent Affairs 03Shahab MurtazaNessuna valutazione finora

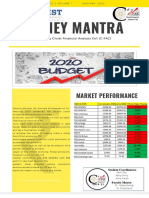

- Money Mantra: Market PerformanceDocumento4 pagineMoney Mantra: Market PerformanceAlbin SibyNessuna valutazione finora

- Economic Survey 2023Documento3 pagineEconomic Survey 2023GRAMMAR SKILLNessuna valutazione finora

- Assignment Fiscal Policy in The PhilippinesDocumento16 pagineAssignment Fiscal Policy in The PhilippinesOliver SantosNessuna valutazione finora

- 1 DrishtiDocumento23 pagine1 DrishtiNeeraj KumarNessuna valutazione finora

- Effects of Fiscal Policy On Indian FirmsDocumento14 pagineEffects of Fiscal Policy On Indian FirmsTewari UtkarshNessuna valutazione finora

- Overview of The Economy: Global Economic ReviewDocumento15 pagineOverview of The Economy: Global Economic ReviewSikandar Hayat100% (1)

- Bangladesh Quarterly Economic Update: June 2014Da EverandBangladesh Quarterly Economic Update: June 2014Nessuna valutazione finora

- Bangladesh Quarterly Economic Update: September 2014Da EverandBangladesh Quarterly Economic Update: September 2014Nessuna valutazione finora

- Overcoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyDa EverandOvercoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyNessuna valutazione finora

- Budget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018Da EverandBudget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018Nessuna valutazione finora

- Form 20-1Documento276 pagineForm 20-1ok2Nessuna valutazione finora

- Ipr Htry PDFDocumento28 pagineIpr Htry PDFok2Nessuna valutazione finora

- Sample Deal Discussions: Sell-Side Divestiture Discussion & AnalysisDocumento11 pagineSample Deal Discussions: Sell-Side Divestiture Discussion & AnalysisAnonymous 45z6m4eE7pNessuna valutazione finora

- Form 20-F - 2018Documento185 pagineForm 20-F - 2018ok2Nessuna valutazione finora

- Investor PresentationDocumento28 pagineInvestor Presentationok2Nessuna valutazione finora

- The Wooden BowlDocumento3 pagineThe Wooden BowlClaudia Elisa Vargas BravoNessuna valutazione finora

- MhfdsbsvslnsafvjqjaoaodldananDocumento160 pagineMhfdsbsvslnsafvjqjaoaodldananLucijanNessuna valutazione finora

- Napoleon BonaparteDocumento1 paginaNapoleon Bonaparteyukihara_mutsukiNessuna valutazione finora

- DPS Quarterly Exam Grade 9Documento3 pagineDPS Quarterly Exam Grade 9Michael EstrellaNessuna valutazione finora

- Wrongful ForeclosureDocumento8 pagineWrongful Foreclosurefaceoneoneoneone100% (2)

- Module 4 1st Quarter EntrepreneurshipDocumento14 pagineModule 4 1st Quarter EntrepreneurshipnattoykoNessuna valutazione finora

- Bible Trivia Questions - Bible Challenges For KidsDocumento4 pagineBible Trivia Questions - Bible Challenges For KidsVinessa Johnson100% (1)

- Class Program: HUMSS 11-MarxDocumento2 pagineClass Program: HUMSS 11-MarxElmer PiadNessuna valutazione finora

- Homicide Act 1957 Section 1 - Abolition of "Constructive Malice"Documento5 pagineHomicide Act 1957 Section 1 - Abolition of "Constructive Malice"Fowzia KaraniNessuna valutazione finora

- SHDP TizonDocumento29 pagineSHDP TizonRonnel Alegria RamadaNessuna valutazione finora

- 1ST Term J3 Business StudiesDocumento19 pagine1ST Term J3 Business Studiesoluwaseun francisNessuna valutazione finora

- SWOT Analysis and Competion of Mangola Soft DrinkDocumento2 pagineSWOT Analysis and Competion of Mangola Soft DrinkMd. Saiful HoqueNessuna valutazione finora

- A Brief Introduction of The OperaDocumento3 pagineA Brief Introduction of The OperaYawen DengNessuna valutazione finora

- Santos vs. Reyes: VOL. 368, OCTOBER 25, 2001 261Documento13 pagineSantos vs. Reyes: VOL. 368, OCTOBER 25, 2001 261Aaron CariñoNessuna valutazione finora

- Project On Hospitality Industry: Customer Relationship ManagementDocumento36 pagineProject On Hospitality Industry: Customer Relationship ManagementShraddha TiwariNessuna valutazione finora

- The Mental Health Act 2018 Tested by High Court of UgandaDocumento7 pagineThe Mental Health Act 2018 Tested by High Court of UgandaLDC Online ResourcesNessuna valutazione finora

- Ez 14Documento2 pagineEz 14yes yesnoNessuna valutazione finora

- Profile Story On Survivor Contestant Trish DunnDocumento6 pagineProfile Story On Survivor Contestant Trish DunnMeganGraceLandauNessuna valutazione finora

- Witherby Connect User ManualDocumento14 pagineWitherby Connect User ManualAshish NayyarNessuna valutazione finora

- Truck Driver Contract AgreementDocumento17 pagineTruck Driver Contract AgreementMaacahNessuna valutazione finora

- 78 Complaint Annulment of Documents PDFDocumento3 pagine78 Complaint Annulment of Documents PDFjd fang-asanNessuna valutazione finora

- Educ 203 CHAPTER 6 Lesson 1Documento13 pagineEduc 203 CHAPTER 6 Lesson 1charmen rogando100% (4)

- Teaching Resume-Anna BedillionDocumento3 pagineTeaching Resume-Anna BedillionAnna Adams ProctorNessuna valutazione finora

- Welcome To The Falcons School For GirlsDocumento6 pagineWelcome To The Falcons School For GirlsSowmiyiaNessuna valutazione finora

- The Absent Presence of Progressive Rock in The British Music Press 1968 1974 PDFDocumento33 pagineThe Absent Presence of Progressive Rock in The British Music Press 1968 1974 PDFwago_itNessuna valutazione finora

- Macpherson - Advanced Written EnglishDocumento102 pagineMacpherson - Advanced Written Englishmarsza23100% (1)

- Module 4 - Starting Your BusinessDocumento8 pagineModule 4 - Starting Your BusinessJHERICA SURELLNessuna valutazione finora

- JONES - Blues People - Negro Music in White AmericaDocumento46 pagineJONES - Blues People - Negro Music in White AmericaNatalia ZambaglioniNessuna valutazione finora

- (Oxford Readers) Michael Rosen - Catriona McKinnon - Jonathan Wolff - Political Thought-Oxford University Press (1999) - 15-18Documento4 pagine(Oxford Readers) Michael Rosen - Catriona McKinnon - Jonathan Wolff - Political Thought-Oxford University Press (1999) - 15-18jyahmedNessuna valutazione finora