Potrebbero piacerti anche

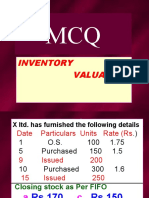

- MCQ Inventory Valuation LBSIMDocumento49 pagineMCQ Inventory Valuation LBSIMSumit SharmaNessuna valutazione finora

- Multiple Choice Questions: Marginal CostingDocumento6 pagineMultiple Choice Questions: Marginal CostingSatyam JainNessuna valutazione finora

- Financial Statement Analysis MCQs With AnswerDocumento5 pagineFinancial Statement Analysis MCQs With AnswerHamza Khan Yousafzai100% (1)

- Multiple Choice Questions: Paper-Bch 2.2: Corporate AccountingDocumento2 pagineMultiple Choice Questions: Paper-Bch 2.2: Corporate AccountingManan GuptaNessuna valutazione finora

- Accounting Concepts MCQsDocumento6 pagineAccounting Concepts MCQsUmar SulemanNessuna valutazione finora

- Cost Sem 5 ObjectiveDocumento16 pagineCost Sem 5 Objectivesimran Keswani0% (1)

- REDEMPTION OF SHARES & DEBENTURES MCQsDocumento7 pagineREDEMPTION OF SHARES & DEBENTURES MCQsChetan StoresNessuna valutazione finora

- It MCQDocumento31 pagineIt MCQbigbulleye6078Nessuna valutazione finora

- Financial Management MCQDocumento31 pagineFinancial Management MCQR.ARULNessuna valutazione finora

- MCQ-Financial Account-SEM VDocumento52 pagineMCQ-Financial Account-SEM VVishnuNadarNessuna valutazione finora

- MCQ Financial Management B Com Sem 5 PDFDocumento17 pagineMCQ Financial Management B Com Sem 5 PDFRadhika Bhargava100% (2)

- Cost Accounting McqsDocumento11 pagineCost Accounting McqsJanani Priya0% (1)

- Export Marketing - Sem Vi MCQ Module 1 - Product Planning & Pricing DecisionsDocumento4 pagineExport Marketing - Sem Vi MCQ Module 1 - Product Planning & Pricing DecisionsSaniya SiddiquiNessuna valutazione finora

- Amalgamation, Absorption & External Reconstruction: Chapter-IDocumento9 pagineAmalgamation, Absorption & External Reconstruction: Chapter-Iayushi aggarwalNessuna valutazione finora

- Funds Flow Statement MCQs Schedule of Changes in Financial Position Multiple Choice Questions and AnDocumento7 pagineFunds Flow Statement MCQs Schedule of Changes in Financial Position Multiple Choice Questions and Anshuhal Ahmed33% (3)

- MCQs Financial Accounting BSCSDocumento11 pagineMCQs Financial Accounting BSCSPervaiz Shahid100% (1)

- WCM Finance MCQDocumento28 pagineWCM Finance MCQMosam AliNessuna valutazione finora

- Xii Mcqs CH - 16 Cash FlowDocumento6 pagineXii Mcqs CH - 16 Cash FlowJoanna GarciaNessuna valutazione finora

- Final Account MCQs PDFDocumento22 pagineFinal Account MCQs PDFHaroon Akhtar0% (2)

- Sem5 MCQ MangACCDocumento8 pagineSem5 MCQ MangACCShirowa ManishNessuna valutazione finora

- COMMERCE MCQs WITH ANSWERS by Usman GhaniDocumento7 pagineCOMMERCE MCQs WITH ANSWERS by Usman GhaniMuhammad Irfan haiderNessuna valutazione finora

- Sem1 MCQ FinancialaccountDocumento14 pagineSem1 MCQ FinancialaccountVemu SaiNessuna valutazione finora

- Multiple Choice Questions: Answer: B. Wealth MaximisationDocumento20 pagineMultiple Choice Questions: Answer: B. Wealth MaximisationArchana Neppolian100% (1)

- Strategic Cost ManagementDocumento5 pagineStrategic Cost ManagementBharat BhojwaniNessuna valutazione finora

- Auditing Sem VI MCQsDocumento10 pagineAuditing Sem VI MCQsMayur PadaveNessuna valutazione finora

- MCQ - Law 1 PDFDocumento160 pagineMCQ - Law 1 PDFBharathNessuna valutazione finora

- Ratio Analysis McqsDocumento10 pagineRatio Analysis McqsNirmal PrasadNessuna valutazione finora

- Sample MCQ 3Documento8 pagineSample MCQ 3varunendra pandeyNessuna valutazione finora

- Summarize MCQsDocumento32 pagineSummarize MCQssohail merchant50% (2)

- MCQ Module 1Documento4 pagineMCQ Module 1mohanraokp2279Nessuna valutazione finora

- Xii Mcqs CH - 11 Redemption of DebenturesDocumento4 pagineXii Mcqs CH - 11 Redemption of DebenturesJoanna GarciaNessuna valutazione finora

- MCQ 2 EpmDocumento3 pagineMCQ 2 EpmCharu LataNessuna valutazione finora

- Cost Accounting BBA MCQsDocumento19 pagineCost Accounting BBA MCQsPhanikumar Katuri100% (1)

- MCQ JournalDocumento4 pagineMCQ JournalKanika BajajNessuna valutazione finora

- MCQ Problems On Marginal Costing: Q.1 (D) (V) AnsDocumento1 paginaMCQ Problems On Marginal Costing: Q.1 (D) (V) AnsHasim SaiyedNessuna valutazione finora

- Insurance Claim AccountDocumento12 pagineInsurance Claim AccountKadam Kartikesh50% (2)

- Xii Mcqs CH - 10 Issue of DebenturesDocumento4 pagineXii Mcqs CH - 10 Issue of DebenturesJoanna GarciaNessuna valutazione finora

- MCQ On Buy Back of Shares - Multiple Choice Questions and AnswerDocumento2 pagineMCQ On Buy Back of Shares - Multiple Choice Questions and AnswerDhawal RajNessuna valutazione finora

- Financial Statements and Financial Statement Analysis McqsDocumento10 pagineFinancial Statements and Financial Statement Analysis McqsNirmal PrasadNessuna valutazione finora

- Audit Mcqs 150 MergedDocumento188 pagineAudit Mcqs 150 MergedKadam KartikeshNessuna valutazione finora

- LeasingDocumento6 pagineLeasingSamar MalikNessuna valutazione finora

- Consumer Protection Act McqsDocumento2 pagineConsumer Protection Act McqsDeeparsh SinghalNessuna valutazione finora

- MCQ - Computerised Accounting - Fy B Com Sem II - CH IDocumento7 pagineMCQ - Computerised Accounting - Fy B Com Sem II - CH IrtNessuna valutazione finora

- Cost Accounting.3 PDFDocumento38 pagineCost Accounting.3 PDFCLAUDINE MUGABEKAZINessuna valutazione finora

- Isssue of Shares and Debentures MCQDocumento42 pagineIsssue of Shares and Debentures MCQlolNessuna valutazione finora

- Exit Model (Fundamental of Accounting)Documento6 pagineExit Model (Fundamental of Accounting)aronNessuna valutazione finora

- CRV Goodwill MCQDocumento9 pagineCRV Goodwill MCQMital ParmarNessuna valutazione finora

- Costing MCQ 1 PDFDocumento19 pagineCosting MCQ 1 PDFCostas Pinto100% (1)

- Account MCQ PDFDocumento93 pagineAccount MCQ PDFsunil kalura100% (1)

- 150 Mcqs Cost Accounting-1Documento23 pagine150 Mcqs Cost Accounting-1Syed LiaqatNessuna valutazione finora

- Cma Inter MCQ Booklet Financial Accounting Paper 5Documento175 pagineCma Inter MCQ Booklet Financial Accounting Paper 5DGGI BPL Group1Nessuna valutazione finora

- Multiple Choices - Fin081Documento2 pagineMultiple Choices - Fin081RovicNessuna valutazione finora

- Polytechnic University of The Philippines College of AccountancyDocumento11 paginePolytechnic University of The Philippines College of AccountancyRonel CacheroNessuna valutazione finora

- AFAR Review Midterm ExamDocumento10 pagineAFAR Review Midterm ExamZyrah Mae SaezNessuna valutazione finora

- FAR Theory Quiz 2Documento9 pagineFAR Theory Quiz 2Ednalyn CruzNessuna valutazione finora

- SQE 2010 (2nd Yr)Documento12 pagineSQE 2010 (2nd Yr)Leslie DiamondNessuna valutazione finora

- Final Exammm 3Documento10 pagineFinal Exammm 3Marianne Adalid MadrigalNessuna valutazione finora

- Final ExamDocumento20 pagineFinal ExamRianell Andrea AsumbradoNessuna valutazione finora

- Final Exam 2021Documento20 pagineFinal Exam 2021Rianell Andrea AsumbradoNessuna valutazione finora

- Multiple Choice: - ConceptualDocumento4 pagineMultiple Choice: - ConceptualCarlo ParasNessuna valutazione finora

- MCQDocumento8 pagineMCQSurya ShekharNessuna valutazione finora

- MCQ NpoDocumento6 pagineMCQ NpoSurya ShekharNessuna valutazione finora

- MCQ Financial Accounting II PDFDocumento23 pagineMCQ Financial Accounting II PDFSurya ShekharNessuna valutazione finora

- Declaration - DIR 4Documento17 pagineDeclaration - DIR 4Ram IyerNessuna valutazione finora

- 14 Audit CommitteeDocumento3 pagine14 Audit CommitteeSurya ShekharNessuna valutazione finora

- 22 The Main Characteristic of PPP IsDocumento3 pagine22 The Main Characteristic of PPP IsSurya ShekharNessuna valutazione finora

- 14 Audit CommitteeDocumento3 pagine14 Audit CommitteeSurya ShekharNessuna valutazione finora

- 5 Standards On AuditingDocumento3 pagine5 Standards On AuditingSurya ShekharNessuna valutazione finora

- 9 Cost Records and Cost Audit ApplicabilityDocumento2 pagine9 Cost Records and Cost Audit ApplicabilitySurya ShekharNessuna valutazione finora

- 22 Audit of PPP ModelDocumento64 pagine22 Audit of PPP ModelSurya Shekhar100% (1)

- 22 Audit of PPP ModelDocumento64 pagine22 Audit of PPP ModelSurya Shekhar100% (1)

- 7e - Chapter 10Documento39 pagine7e - Chapter 10WaltherNessuna valutazione finora

- GCG MC No. 2012-07 - Code of Corp Governance PDFDocumento31 pagineGCG MC No. 2012-07 - Code of Corp Governance PDFakalamoNessuna valutazione finora

- Ready, Steady,: ForexDocumento25 pagineReady, Steady,: ForexSrini VasanNessuna valutazione finora

- Laporan Rekening Koran (Account Statement Report) : Balance Remark Debit Reference No Credit Posting DateDocumento6 pagineLaporan Rekening Koran (Account Statement Report) : Balance Remark Debit Reference No Credit Posting Datedok wahab siddikNessuna valutazione finora

- Sweetheart Loan - Florendo Vs CADocumento2 pagineSweetheart Loan - Florendo Vs CAErmeline TampusNessuna valutazione finora

- VAT Guidance For Retailers: 375,000 / 12 MonthsDocumento1 paginaVAT Guidance For Retailers: 375,000 / 12 MonthsMuhammad Suhaib FaryadNessuna valutazione finora

- Everest Group Names HCL As A Leader For IT Outsourcing in Global Capital Markets (Company Update)Documento3 pagineEverest Group Names HCL As A Leader For IT Outsourcing in Global Capital Markets (Company Update)Shyam SunderNessuna valutazione finora

- Direct Deposit Authorization Form - Controlled PDFDocumento2 pagineDirect Deposit Authorization Form - Controlled PDFNatilee CampbellNessuna valutazione finora

- Monthly GK Digest June PDFDocumento26 pagineMonthly GK Digest June PDFakshaykumarNessuna valutazione finora

- Week 4 Solutions To ExercisesDocumento5 pagineWeek 4 Solutions To ExercisesBerend van RoozendaalNessuna valutazione finora

- Instant Download Ebook PDF Financial Accounting 4th Edition by J David Spiceland PDF ScribdDocumento23 pagineInstant Download Ebook PDF Financial Accounting 4th Edition by J David Spiceland PDF Scribdmarian.hillis984100% (38)

- Newyork Review of Books 8 October 2015Documento60 pagineNewyork Review of Books 8 October 2015Hugo Coelho100% (1)

- 28 U.S. Code 3002 - Definitions - U.S. Code - US Law - LII - Legal Information InstituteDocumento4 pagine28 U.S. Code 3002 - Definitions - U.S. Code - US Law - LII - Legal Information InstituteMatías PierottiNessuna valutazione finora

- CH 2 - T.BDocumento25 pagineCH 2 - T.BSAMOIERNessuna valutazione finora

- Chem Med CaseDocumento6 pagineChem Med CaseChris100% (1)

- Final Project Report of Summer Internship (VK)Documento56 pagineFinal Project Report of Summer Internship (VK)Vikas Kumar PatelNessuna valutazione finora

- Agreed Upn Procedures Report 3 PDFDocumento4 pagineAgreed Upn Procedures Report 3 PDFirfanNessuna valutazione finora

- Hyundai Pricelist CSDDocumento2 pagineHyundai Pricelist CSDNandish KumarNessuna valutazione finora

- Contingency Planning & Simulation Exercises Practical ApplicationsDocumento11 pagineContingency Planning & Simulation Exercises Practical ApplicationsMustafa Shafiq RazalliNessuna valutazione finora

- Evaluation On The Effectiveness of The CDocumento104 pagineEvaluation On The Effectiveness of The CAilene Quinto0% (1)

- Value Based Questions in Economics Class XIIDocumento8 pagineValue Based Questions in Economics Class XIIkkumar009Nessuna valutazione finora

- Summative Test in Math (Part Ii) Quarter 1Documento1 paginaSummative Test in Math (Part Ii) Quarter 1JAY MIRANDANessuna valutazione finora

- Determinants of Profitability of Non Bank Financial Institutions' in A Developing Country: Evidence From BangladeshDocumento12 pagineDeterminants of Profitability of Non Bank Financial Institutions' in A Developing Country: Evidence From BangladeshNahid Md. AlamNessuna valutazione finora

- Accounting ProjectDocumento2 pagineAccounting ProjectAngel Grefaldo VillegasNessuna valutazione finora

- Forensic Audit Report Press StatementDocumento3 pagineForensic Audit Report Press StatementNation OnlineNessuna valutazione finora

- Ledger - Problems and SolutionsDocumento1 paginaLedger - Problems and SolutionsDjamal SalimNessuna valutazione finora

- The White Paper-Equity And: Excellence - Implications For GpsDocumento24 pagineThe White Paper-Equity And: Excellence - Implications For GpsTim SandleNessuna valutazione finora

- Management Report On Reckitt Benckiser Bangladesh LTDDocumento13 pagineManagement Report On Reckitt Benckiser Bangladesh LTDOld PagesNessuna valutazione finora

- Islamic Capital Markets: The Role of Sukuk: Executive SummaryDocumento4 pagineIslamic Capital Markets: The Role of Sukuk: Executive SummaryiisjafferNessuna valutazione finora

- Hotel ProjectDocumento38 pagineHotel ProjectMelat MakonnenNessuna valutazione finora