Potrebbero piacerti anche

- AKL - Chapter 11Documento22 pagineAKL - Chapter 11yesNessuna valutazione finora

- Consolidation Theories, Push-Down Accounting, and Corporate Joint VenturesDocumento27 pagineConsolidation Theories, Push-Down Accounting, and Corporate Joint VenturesvionaNessuna valutazione finora

- Advanced Accounting II Chapter 11Documento21 pagineAdvanced Accounting II Chapter 11Jwenty SihombingNessuna valutazione finora

- Consolidations SummaryDocumento9 pagineConsolidations Summaryu22541617Nessuna valutazione finora

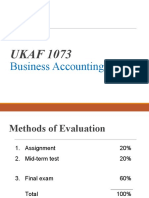

- UKAF 1073: Business Accounting IIDocumento61 pagineUKAF 1073: Business Accounting IIalibabaNessuna valutazione finora

- Bus 312Documento8 pagineBus 312Goop BoopNessuna valutazione finora

- Consolidated Financial Statements (Part 3)Documento96 pagineConsolidated Financial Statements (Part 3)Justine Kate Ferrer BascoNessuna valutazione finora

- Eiteman PPT CH01Documento37 pagineEiteman PPT CH01Divya BansalNessuna valutazione finora

- FinancialDocumento12 pagineFinancialPhuong ThanhNessuna valutazione finora

- Capital StructureDocumento18 pagineCapital StructureAll TrendsNessuna valutazione finora

- Valuation of SharesDocumento45 pagineValuation of Shares7laxmanNessuna valutazione finora

- Dividend Policy and DecisionsDocumento2 pagineDividend Policy and Decisionsshubham malhotraNessuna valutazione finora

- Consolidation TheoriesDocumento5 pagineConsolidation TheoriesAyan RoyNessuna valutazione finora

- BAT4M Grade 12 University College Accounting Chapter 13 TestDocumento5 pagineBAT4M Grade 12 University College Accounting Chapter 13 TestBingyi Angela ZhouNessuna valutazione finora

- Equity Capital Common and Preffered StockDocumento23 pagineEquity Capital Common and Preffered StockNicole LasiNessuna valutazione finora

- Dividends and Dividend PolicyDocumento30 pagineDividends and Dividend PolicyAbdela Aman MtechNessuna valutazione finora

- Materi 9 resiko-WPS OfficeDocumento8 pagineMateri 9 resiko-WPS OfficeCikampek AtuhNessuna valutazione finora

- Dividend Policy: Cash Dividends-Payments Made To Dividend Policy-Decisions About When and HowDocumento25 pagineDividend Policy: Cash Dividends-Payments Made To Dividend Policy-Decisions About When and HowGene Villena AbarquezNessuna valutazione finora

- Financing:: 1. Role of Shareholders As StakeholdersDocumento2 pagineFinancing:: 1. Role of Shareholders As Stakeholdersrammar147Nessuna valutazione finora

- Caiib Fmmodbacs Nov08Documento91 pagineCaiib Fmmodbacs Nov08monirba48Nessuna valutazione finora

- CAIIB-Financial Management-Module B Study of Financial StatementsDocumento91 pagineCAIIB-Financial Management-Module B Study of Financial StatementsDeepak RathoreNessuna valutazione finora

- Finance Management: Swapnil S KarvirDocumento29 pagineFinance Management: Swapnil S KarvirMarvellous NerdNessuna valutazione finora

- EBF 2054 Capital StructureDocumento38 pagineEBF 2054 Capital StructureizzatiNessuna valutazione finora

- Internal - Retained Earnings External - Debt (Short-Term vs. Long-Term), Equity and Hybrids (PreferredDocumento1 paginaInternal - Retained Earnings External - Debt (Short-Term vs. Long-Term), Equity and Hybrids (PreferreddskrishnaNessuna valutazione finora

- VC - Finm7312 Slides # 3Documento24 pagineVC - Finm7312 Slides # 3Phumzile MahlanguNessuna valutazione finora

- Capital Structure and Dividend PolicyDocumento25 pagineCapital Structure and Dividend PolicySarah Mae SudayanNessuna valutazione finora

- Unit 4 - FInancial Management & Corporate Finance - KMBN 204-1 - 230707 - 185305Documento18 pagineUnit 4 - FInancial Management & Corporate Finance - KMBN 204-1 - 230707 - 185305upsc viewNessuna valutazione finora

- Introduction To Project FinanceDocumento38 pagineIntroduction To Project FinanceMuhammad Waheed SattiNessuna valutazione finora

- Dividend PolicyDocumento4 pagineDividend PolicySimon silaNessuna valutazione finora

- Financing Decisions Capital Structure: M. Pavan KumarDocumento26 pagineFinancing Decisions Capital Structure: M. Pavan KumarPavan Kumar MylavaramNessuna valutazione finora

- FM II - Chapter 02, Divided PayoutDocumento35 pagineFM II - Chapter 02, Divided PayoutKalkidan G/wahidNessuna valutazione finora

- Akuntansi Keuangan Lanjutan 1: Program Studi Akuntansi Fakultas Ilmu Sosial Dan Humaniora Universitas Bunda MuliaDocumento44 pagineAkuntansi Keuangan Lanjutan 1: Program Studi Akuntansi Fakultas Ilmu Sosial Dan Humaniora Universitas Bunda MuliaTri MahathirNessuna valutazione finora

- Sources of Company FinanceDocumento15 pagineSources of Company Financenileprab877Nessuna valutazione finora

- Basic Facts About ESOPs2Documento20 pagineBasic Facts About ESOPs2Quant TradingNessuna valutazione finora

- Esops 101 (What/Why/How) : Robert E. BrownDocumento20 pagineEsops 101 (What/Why/How) : Robert E. Brownashwani7789Nessuna valutazione finora

- Distribution To ShareholdersDocumento47 pagineDistribution To Shareholderszyra liam stylesNessuna valutazione finora

- Mfe Finals ReviewerDocumento3 pagineMfe Finals ReviewerMerry Joy SolizaNessuna valutazione finora

- Chapter 1: Forms of Business Ownership 1.1 Sole TraderDocumento15 pagineChapter 1: Forms of Business Ownership 1.1 Sole TraderBrandon LuuNessuna valutazione finora

- Fins5514 L01 2023 PDFDocumento33 pagineFins5514 L01 2023 PDFwilliam YuNessuna valutazione finora

- Corporate Governance LectureDocumento24 pagineCorporate Governance LectureVe DekNessuna valutazione finora

- Capital StructureDocumento69 pagineCapital Structurereal history and series real history and seriesNessuna valutazione finora

- Equity - The Accounting Equation For Every BusinessDocumento5 pagineEquity - The Accounting Equation For Every BusinessSarah Del RosarioNessuna valutazione finora

- Chapter 1 Fin 2200Documento7 pagineChapter 1 Fin 2200cheeseNessuna valutazione finora

- Advanced Accounting Part 2 Business Combinations (Ifrs 3)Documento10 pagineAdvanced Accounting Part 2 Business Combinations (Ifrs 3)ClarkNessuna valutazione finora

- DividendsDocumento8 pagineDividendsNtege SimonNessuna valutazione finora

- Dividend Decisions - Dividend PolicyDocumento24 pagineDividend Decisions - Dividend PolicyTIBUGWISHA IVANNessuna valutazione finora

- Economics - Topic 7Documento13 pagineEconomics - Topic 7AB RomillaNessuna valutazione finora

- Dividend Theory Objectives - To Understand: DividendsDocumento41 pagineDividend Theory Objectives - To Understand: DividendsPrAkhar VermaNessuna valutazione finora

- FM Notes - Unit - 5Documento7 pagineFM Notes - Unit - 5Shiva JohriNessuna valutazione finora

- Distribution To ShareholdersDocumento47 pagineDistribution To ShareholdersVanny NaragasNessuna valutazione finora

- Theories On Dividend Policy2Documento44 pagineTheories On Dividend Policy2Ahmad RazaNessuna valutazione finora

- Payout PolicyDocumento9 paginePayout PolicyFirman Nur ZulfikarNessuna valutazione finora

- M&a BasicsDocumento26 pagineM&a BasicsSpace MuskNessuna valutazione finora

- Allocation of Cash Dividends Between Preference Share and Ordinary ShareDocumento2 pagineAllocation of Cash Dividends Between Preference Share and Ordinary Shareshaina.planco4Nessuna valutazione finora

- Dividend PolicyDocumento14 pagineDividend PolicySaeedNessuna valutazione finora

- Solution Manual For Advanced Accounting 14th Edition Joe Ben Hoyle Thomas Schaefer Timothy DoupnikDocumento39 pagineSolution Manual For Advanced Accounting 14th Edition Joe Ben Hoyle Thomas Schaefer Timothy DoupnikMariaPetersonewjkf100% (79)

- Advanced Accounting 13th Edition Hoyle Solutions ManualDocumento38 pagineAdvanced Accounting 13th Edition Hoyle Solutions Manualpottpotlacew8mf1t100% (15)

- Advanced Accounting 13th Edition Hoyle Solutions Manual Full Chapter PDFDocumento60 pagineAdvanced Accounting 13th Edition Hoyle Solutions Manual Full Chapter PDFanwalteru32x100% (13)

- BUSINESS PROPOSAL-dönüştürüldü-2Documento15 pagineBUSINESS PROPOSAL-dönüştürüldü-2Fatah Imdul UmasugiNessuna valutazione finora

- Bugreport Fog - in SKQ1.211103.001 2023 04 10 19 23 21 Dumpstate - Log 9097Documento32 pagineBugreport Fog - in SKQ1.211103.001 2023 04 10 19 23 21 Dumpstate - Log 9097chandrakanth reddyNessuna valutazione finora

- Final - Far Capital - Infopack Diana V3 PDFDocumento79 pagineFinal - Far Capital - Infopack Diana V3 PDFjoekaledaNessuna valutazione finora

- Package Contents: Ariadni DivaDocumento4 paginePackage Contents: Ariadni DivaShadi AbdelsalamNessuna valutazione finora

- ESAT FormulaDocumento11 pagineESAT FormulaSKYE LightsNessuna valutazione finora

- Project DescriptionDocumento5 pagineProject DescriptionM ShahidNessuna valutazione finora

- MCQ Criminal Law 1Documento18 pagineMCQ Criminal Law 1Clark Vincent Ponla0% (1)

- Contractor Commissioning ProcedureDocumento61 pagineContractor Commissioning ProcedureTaras Pompiliu100% (8)

- Project Execution and Control: Lunar International College July, 2021Documento35 pagineProject Execution and Control: Lunar International College July, 2021getahun tesfayeNessuna valutazione finora

- Policy 0000000001523360 PDFDocumento15 paginePolicy 0000000001523360 PDFunique infraNessuna valutazione finora

- Starbucks Delivering Customer Service Case Solution PDFDocumento2 pagineStarbucks Delivering Customer Service Case Solution PDFRavia SharmaNessuna valutazione finora

- CompressDocumento14 pagineCompressAnonymous gfR3btyU0% (1)

- Numerical Techniques For Global AtmosphericDocumento577 pagineNumerical Techniques For Global AtmosphericTatiana N. LeónNessuna valutazione finora

- Labor Relations LawsDocumento20 pagineLabor Relations LawsREENA ALEKSSANDRA ACOPNessuna valutazione finora

- Scope and Sequence Plan Stage4 Year7 Visual ArtsDocumento5 pagineScope and Sequence Plan Stage4 Year7 Visual Artsapi-254422131Nessuna valutazione finora

- Guia de Desinstalación de ODOO EN UBUNTUDocumento3 pagineGuia de Desinstalación de ODOO EN UBUNTUjesusgom100% (1)

- Donor's Tax Post QuizDocumento12 pagineDonor's Tax Post QuizMichael Aquino0% (1)

- Engineering & Machinery Corp vs. CADocumento8 pagineEngineering & Machinery Corp vs. CALaila Ismael SalisaNessuna valutazione finora

- BBBB - View ReservationDocumento2 pagineBBBB - View ReservationBashir Ahmad BashirNessuna valutazione finora

- XC3000 Series Motion Control System of Laser Cutting Commissioning Manual TextDocumento138 pagineXC3000 Series Motion Control System of Laser Cutting Commissioning Manual Textgerardo.reynosoNessuna valutazione finora

- Global Competitiveness ReportDocumento7 pagineGlobal Competitiveness ReportSHOIRYANessuna valutazione finora

- Refill Brand Guidelines 2Documento23 pagineRefill Brand Guidelines 2Catalin MihailescuNessuna valutazione finora

- Complaint Handling Policy of CBECDocumento52 pagineComplaint Handling Policy of CBECharrypotter1Nessuna valutazione finora

- NF en 1317-5 In2Documento23 pagineNF en 1317-5 In2ArunNessuna valutazione finora

- India's Information Technology Sector: What Contribution To Broader Economic Development?Documento32 pagineIndia's Information Technology Sector: What Contribution To Broader Economic Development?Raj KumarNessuna valutazione finora

- Antenna MCQsDocumento38 pagineAntenna MCQsAishwarya BalamuruganNessuna valutazione finora

- Kathrein 739624Documento2 pagineKathrein 739624anna.bNessuna valutazione finora

- Divisional Sec. Contact Details 2019-03-01-UpdateDocumento14 pagineDivisional Sec. Contact Details 2019-03-01-Updatedotr9317Nessuna valutazione finora

- 40th Caterpillar Performance HandbookDocumento372 pagine40th Caterpillar Performance Handbookcarlos_córdova_8100% (11)

- BS en Iso 11114-4-2005 (2007)Documento30 pagineBS en Iso 11114-4-2005 (2007)DanielVegaNeira100% (1)