Potrebbero piacerti anche

- MRFDocumento16 pagineMRFArijit Ghosh100% (1)

- Tyre IndustryAnalysisDocumento15 pagineTyre IndustryAnalysisArijit GhoshNessuna valutazione finora

- Increasing Anti-Globalisation Sentiment in Larger Economies of The WorldDocumento4 pagineIncreasing Anti-Globalisation Sentiment in Larger Economies of The WorldArijit GhoshNessuna valutazione finora

- Sustainable Supply Chain Managemen Indian ContextDocumento7 pagineSustainable Supply Chain Managemen Indian ContextArijit GhoshNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- BitAuto IPO Prospectus 2010Documento291 pagineBitAuto IPO Prospectus 2010ryanmaruiNessuna valutazione finora

- Bill of Sale Agreement For Dear Fnu Asonganyi TazochaDocumento1 paginaBill of Sale Agreement For Dear Fnu Asonganyi Tazochastorage mediaNessuna valutazione finora

- BMW AG. - The Rover CompanyDocumento2 pagineBMW AG. - The Rover CompanySindhu SinghNessuna valutazione finora

- 4WD ZF Carraro PublicationDocumento68 pagine4WD ZF Carraro PublicationRobert Russell100% (7)

- Advanced Manufacturing Processes: (Mechanical Engineering Group)Documento20 pagineAdvanced Manufacturing Processes: (Mechanical Engineering Group)Vikram Kumar100% (1)

- Internship ReportDocumento14 pagineInternship ReportDevKV100% (1)

- Argentum Auto Technical PresentationDocumento85 pagineArgentum Auto Technical PresentationaksyalNessuna valutazione finora

- A Project Study Report On Marketing Strategy of JK Tyre LimitedDocumento11 pagineA Project Study Report On Marketing Strategy of JK Tyre LimitedthexxxanasNessuna valutazione finora

- Crawler Crane 1 PDFDocumento12 pagineCrawler Crane 1 PDFagungNessuna valutazione finora

- Manual de Grua Faun ATF-110G-5Documento31 pagineManual de Grua Faun ATF-110G-5La Roca100% (1)

- Hedweld New Product CatalogueDocumento16 pagineHedweld New Product CataloguevictorNessuna valutazione finora

- Mohamad Omar MohamadDocumento44 pagineMohamad Omar MohamadVictor GarciaNessuna valutazione finora

- 1412TP 204 204Documento8 pagine1412TP 204 204Muhammad UmairNessuna valutazione finora

- Imds Newsletter 61Documento5 pagineImds Newsletter 61taleshNessuna valutazione finora

- Booklet DP3Documento8 pagineBooklet DP3niggeruNessuna valutazione finora

- Property Retail Buy & Sell: Can't Ind What You're Looking For? Check Online at Freepressseries - Co.ukDocumento4 pagineProperty Retail Buy & Sell: Can't Ind What You're Looking For? Check Online at Freepressseries - Co.ukDigital MediaNessuna valutazione finora

- 01-Company Profile - PT Rizki Asa BuanaDocumento20 pagine01-Company Profile - PT Rizki Asa BuanaLiandra Ayu NeysiaNessuna valutazione finora

- Voorhees 0515Documento28 pagineVoorhees 0515elauwitNessuna valutazione finora

- Electric Cars-Vol2Documento32 pagineElectric Cars-Vol2Sơn Phạm ThanhNessuna valutazione finora

- Fastwind Monoshock 200 Picture Book 2010Documento32 pagineFastwind Monoshock 200 Picture Book 2010camilo0918Nessuna valutazione finora

- Tata Motors Does Not Follow A Single Marketing Approach or Formula But It Believes That All Members of The Community Should Be ServedDocumento5 pagineTata Motors Does Not Follow A Single Marketing Approach or Formula But It Believes That All Members of The Community Should Be ServedVasu Dev KanchetiNessuna valutazione finora

- Team Maxxim VW Marketing StrategyDocumento36 pagineTeam Maxxim VW Marketing StrategyShaiksha SyedNessuna valutazione finora

- Ford Motor Company Case StudyDocumento13 pagineFord Motor Company Case Studykhopdi_number1100% (1)

- Alterations To 265 & 267 Wellington Street, Launceston: Jackson Trade CarsDocumento7 pagineAlterations To 265 & 267 Wellington Street, Launceston: Jackson Trade CarsThe ExaminerNessuna valutazione finora

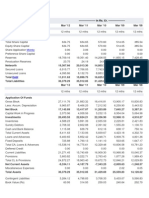

- Balance Sheet of Tata MotorsDocumento25 pagineBalance Sheet of Tata MotorsDevendra Dilip BaikarNessuna valutazione finora

- Relevant Costs For Decision MakingDocumento46 pagineRelevant Costs For Decision MakingFirlanaSubektiNessuna valutazione finora

- Parker Serie P1+PDDocumento84 pagineParker Serie P1+PDRodrigo IglesiasNessuna valutazione finora

- Product Layout of MarutiDocumento16 pagineProduct Layout of MarutiJagmohan Bisht75% (4)