Potrebbero piacerti anche

- Operational Auditing A Complete Guide - 2021 EditionDa EverandOperational Auditing A Complete Guide - 2021 EditionNessuna valutazione finora

- MAS QuizDocumento6 pagineMAS QuizGracelle Mae OrallerNessuna valutazione finora

- MAS Review CVP and Variable CostingDocumento7 pagineMAS Review CVP and Variable CostingAizzy ManioNessuna valutazione finora

- CRC Ace Mas First PBDocumento10 pagineCRC Ace Mas First PBJohn Philip Castro100% (2)

- 04 - Relevant CostingDocumento5 pagine04 - Relevant CostingVince De Guzman100% (2)

- 25 Profit-Performance Measurements & Intracompany Transfer PricingDocumento13 pagine25 Profit-Performance Measurements & Intracompany Transfer PricingLaurenz Simon ManaliliNessuna valutazione finora

- CH 08Documento52 pagineCH 08kareem_batista20860% (5)

- MAS Theory AnswerDocumento7 pagineMAS Theory Answerhanna jeanNessuna valutazione finora

- Variance AnalysisDocumento21 pagineVariance Analysismark anthony espiritu0% (1)

- Financial Analysis ReviewerDocumento15 pagineFinancial Analysis ReviewerPrincess Corine BurgosNessuna valutazione finora

- MAS Compilation of QuestionsDocumento21 pagineMAS Compilation of QuestionsTom Dominguez100% (1)

- Managerial AccountingMid Term Examination (1) - CONSULTADocumento7 pagineManagerial AccountingMid Term Examination (1) - CONSULTAMay Ramos100% (1)

- JakeDocumento5 pagineJakeEvan JordanNessuna valutazione finora

- TaxDocumento3 pagineTaxArven FrancoNessuna valutazione finora

- AcctgDocumento35 pagineAcctgKariz CodogNessuna valutazione finora

- INSTRUCTIONS: Write Your Final Answer in The Answer Sheet. NO ERASURES ALLOWEDDocumento18 pagineINSTRUCTIONS: Write Your Final Answer in The Answer Sheet. NO ERASURES ALLOWEDSandra Mae CabuenasNessuna valutazione finora

- Financial Management RiskDocumento11 pagineFinancial Management RisknevadNessuna valutazione finora

- Management Advisory Services Cpa ReviewDocumento30 pagineManagement Advisory Services Cpa ReviewRyan PedroNessuna valutazione finora

- Test Bank Chapter 8 ABC For Decision Making PDFDocumento44 pagineTest Bank Chapter 8 ABC For Decision Making PDFMarvin AquinoNessuna valutazione finora

- RMYC Cup 2 - RevDocumento9 pagineRMYC Cup 2 - RevJasper Andrew AdjaraniNessuna valutazione finora

- Cost Chapter 14Documento15 pagineCost Chapter 14Marica ShaneNessuna valutazione finora

- 04 CVP AnswerDocumento36 pagine04 CVP AnswerjoyjoyjoyNessuna valutazione finora

- 18 x12 ABC A Traditional Cost Accounting (MAS) BobadillaDocumento11 pagine18 x12 ABC A Traditional Cost Accounting (MAS) BobadillaAnnaNessuna valutazione finora

- Management Advisory ServicesDocumento10 pagineManagement Advisory ServicesMark ArceoNessuna valutazione finora

- Chapter 20Documento9 pagineChapter 20Juja FlorentinoNessuna valutazione finora

- CPAR AT - Philippine Accountancy Act of 2004Documento4 pagineCPAR AT - Philippine Accountancy Act of 2004John Carlo CruzNessuna valutazione finora

- Cup-Management Advisory ServicesDocumento7 pagineCup-Management Advisory ServicesJerauld BucolNessuna valutazione finora

- CH 02Documento53 pagineCH 02CloudKielGuiangNessuna valutazione finora

- Chapter 7Documento18 pagineChapter 7kathleenNessuna valutazione finora

- Accounting On Business Combination Quiz 2: Multiple ChoiceDocumento13 pagineAccounting On Business Combination Quiz 2: Multiple ChoiceTokkiNessuna valutazione finora

- File 4795281140322753513Documento10 pagineFile 4795281140322753513Akako MatsumotoNessuna valutazione finora

- Capital Budgeting Lecture UpdatedDocumento5 pagineCapital Budgeting Lecture UpdatedMark Gelo WinchesterNessuna valutazione finora

- 09 X07 C Responsibility Accounting and TP Variable Costing & Segmented ReportingDocumento8 pagine09 X07 C Responsibility Accounting and TP Variable Costing & Segmented ReportingAnnaNessuna valutazione finora

- Quiz On Cap BudgDocumento3 pagineQuiz On Cap BudgjjjjjjjjNessuna valutazione finora

- Blessed Me LordDocumento168 pagineBlessed Me LordBoa HancockNessuna valutazione finora

- Notes and Loans ReceivableDocumento10 pagineNotes and Loans ReceivableKent TumulakNessuna valutazione finora

- Responsibility Accounting and Transfer PricingDocumento25 pagineResponsibility Accounting and Transfer Pricingjustine reine cornicoNessuna valutazione finora

- Direct and Absorption Costing 2014Documento15 pagineDirect and Absorption Costing 2014Aj de CastroNessuna valutazione finora

- Business Law: "Serving Towards Your CPADocumento19 pagineBusiness Law: "Serving Towards Your CPADanielle Nicole MarquezNessuna valutazione finora

- Variable Costing - Cost Accounting QuizDocumento2 pagineVariable Costing - Cost Accounting QuizRizza Mae RodriguezNessuna valutazione finora

- Process1 Process2 Process3Documento2 pagineProcess1 Process2 Process3Darwin Competente LagranNessuna valutazione finora

- Test Bank - Mgt. Acctg 2 - CparDocumento16 pagineTest Bank - Mgt. Acctg 2 - CparChris LlevaNessuna valutazione finora

- Saint Theresa College of Tandag, Inc. Tandag City Strategic Cost Management - Summer Class Dit 1Documento4 pagineSaint Theresa College of Tandag, Inc. Tandag City Strategic Cost Management - Summer Class Dit 1Esheikell ChenNessuna valutazione finora

- Cost 2 Finals Quiz 1 2Documento15 pagineCost 2 Finals Quiz 1 2Jp Combis0% (1)

- 2009-09-06 125024 MmmmekaDocumento24 pagine2009-09-06 125024 MmmmekathenikkitrNessuna valutazione finora

- Chapter 3Documento11 pagineChapter 3Christlyn Joy BaralNessuna valutazione finora

- Financial Reporting Standards Council (FRSC)Documento43 pagineFinancial Reporting Standards Council (FRSC)Pam G.Nessuna valutazione finora

- CH 19Documento29 pagineCH 19Emey CalbayNessuna valutazione finora

- TAX. M-1401 Estate Tax: Basic TerminologiesDocumento33 pagineTAX. M-1401 Estate Tax: Basic TerminologiesJimmyChaoNessuna valutazione finora

- Chapter 9 - The Use of Budgets in Planning and Decision MakingDocumento71 pagineChapter 9 - The Use of Budgets in Planning and Decision MakingGray JavierNessuna valutazione finora

- MAC Material 2Documento33 pagineMAC Material 2Blessy Zedlav LacbainNessuna valutazione finora

- All Board Subjects Material 1Documento28 pagineAll Board Subjects Material 1Blessy Zedlav LacbainNessuna valutazione finora

- 2nd Evaluation Exam Key FINALDocumento7 pagine2nd Evaluation Exam Key FINALChristian GeronimoNessuna valutazione finora

- Sale Price of Replaced Equipment P 40,000Documento15 pagineSale Price of Replaced Equipment P 40,000Jay GamboaNessuna valutazione finora

- Sample Questions From Chapter 15Documento5 pagineSample Questions From Chapter 15FH100% (1)

- MS Quiz 3Documento4 pagineMS Quiz 3Harold Dan AcebedoNessuna valutazione finora

- MAS Midterm Quiz 2Documento4 pagineMAS Midterm Quiz 2Joseph John SarmientoNessuna valutazione finora

- NFJPIA - Mockboard 2011 - MAS PDFDocumento7 pagineNFJPIA - Mockboard 2011 - MAS PDFSteven Mark MananguNessuna valutazione finora

- Budget ADocumento15 pagineBudget Ayahoo2008Nessuna valutazione finora

- Accountancy Review Center (ARC) of The Philippines Inc.: Mockboard ExaminationDocumento10 pagineAccountancy Review Center (ARC) of The Philippines Inc.: Mockboard ExaminationJudy TotoNessuna valutazione finora

- Auditing Theory MCQs by Salosagcol With AnswersDocumento31 pagineAuditing Theory MCQs by Salosagcol With AnswersYeovil Pansacala79% (62)

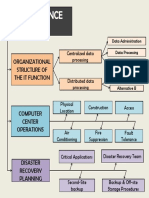

- Organizational Structure of The It Function: Centralized Data ProcessingDocumento1 paginaOrganizational Structure of The It Function: Centralized Data ProcessingRyan Christian M. CoralNessuna valutazione finora

- Theoretical FrameworkDocumento1 paginaTheoretical FrameworkRyan Christian M. CoralNessuna valutazione finora

- Management Advisory Services-Elimination RoundDocumento18 pagineManagement Advisory Services-Elimination RoundRyan Christian M. Coral0% (1)

- AcadsDocumento4 pagineAcadsRyan Christian M. CoralNessuna valutazione finora

- Audit Plan GuideDocumento4 pagineAudit Plan GuideRyan Christian M. CoralNessuna valutazione finora

- FinMan PDFDocumento7 pagineFinMan PDFPrincess Engreso100% (1)

- FAR - Final RoundDocumento16 pagineFAR - Final RoundRyan Christian M. CoralNessuna valutazione finora

- 19 x12 ABC B Activity-Based Cost SystemDocumento15 pagine19 x12 ABC B Activity-Based Cost SystemJericho Pedragosa67% (6)

- Contents of A Good Research Proposal v1.0Documento2 pagineContents of A Good Research Proposal v1.0Bright Williams BoakyeNessuna valutazione finora

- Management Advisory Services - Final RoundDocumento14 pagineManagement Advisory Services - Final RoundRyan Christian M. CoralNessuna valutazione finora

- 12 x10 Financial Statement AnalysisDocumento22 pagine12 x10 Financial Statement AnalysisRaffi Tamayo92% (25)

- Allowable DeductionsDocumento4 pagineAllowable DeductionsdailydoseoflawNessuna valutazione finora

- Project Plant Pals Operations & Training Plan: February 15thDocumento3 pagineProject Plant Pals Operations & Training Plan: February 15thP E100% (1)

- Global Cycle Notes - Fixed Income. Credit Suisse. June 02, 2014Documento24 pagineGlobal Cycle Notes - Fixed Income. Credit Suisse. June 02, 2014VizziniNessuna valutazione finora

- Chapter 7 - Management Accounting F2Documento3 pagineChapter 7 - Management Accounting F2Bội Anh Nguyễn Bội AnhNessuna valutazione finora

- Aggregate PlanningDocumento57 pagineAggregate PlanningSanjeev RanjanNessuna valutazione finora

- ProModel SimulationDocumento25 pagineProModel SimulationScribdTranslationsNessuna valutazione finora

- Inventory Management at TATA STEELDocumento90 pagineInventory Management at TATA STEELBalakrishna Chakali40% (5)

- Chapter 11 TestbankDocumento25 pagineChapter 11 TestbankBùi Thị Vân Anh 06Nessuna valutazione finora

- Markov Decision ProcessesDocumento104 pagineMarkov Decision ProcessesWillians Ribeiro Mendes100% (1)

- Management AccountingDocumento155 pagineManagement AccountingBbaggi Bk100% (2)

- Pharmaceutical Manufacturers Embracing Lean Six SigmaDocumento6 paginePharmaceutical Manufacturers Embracing Lean Six SigmahaiderfatmiNessuna valutazione finora

- Working Capital ManagementDocumento72 pagineWorking Capital ManagementShilpi AggarwalNessuna valutazione finora

- Amazon Supply ChainDocumento8 pagineAmazon Supply ChainOSHEEN MISHRANessuna valutazione finora

- Cabria Cpa Review Center: Tel. Nos. (043) 980-6659Documento10 pagineCabria Cpa Review Center: Tel. Nos. (043) 980-6659MaeNessuna valutazione finora

- Journal of Humanitarian Logistics and Supply Chain ManagementDocumento32 pagineJournal of Humanitarian Logistics and Supply Chain ManagementSyaiful Muhammad FurqonNessuna valutazione finora

- NIC 2 (2021) - 2023 V CICLO en-USDocumento6 pagineNIC 2 (2021) - 2023 V CICLO en-USMj264Nessuna valutazione finora

- Working Capital Management in BhelDocumento86 pagineWorking Capital Management in BhelDipesh Gandhi100% (1)

- MS ZucamorDocumento6 pagineMS ZucamorMohammed Ali JavaidNessuna valutazione finora

- ACME CaseDocumento3 pagineACME CaseNamitOhriNessuna valutazione finora

- Inventory Management Applications For Healthcare Supply ChainsDocumento7 pagineInventory Management Applications For Healthcare Supply ChainsAjay tyagi IndianNessuna valutazione finora

- E-Commerce 2017 Business. Technology. Society.: 13 EditionDocumento45 pagineE-Commerce 2017 Business. Technology. Society.: 13 EditionFahim RezaNessuna valutazione finora

- n.202 General Accounting ExercisesDocumento7 paginen.202 General Accounting ExercisesMohanad EmadNessuna valutazione finora

- Sales Order Processing For Sales Kits (31Q - US) : Test Script SAP S/4HANA - 28-08-18Documento25 pagineSales Order Processing For Sales Kits (31Q - US) : Test Script SAP S/4HANA - 28-08-18MihaiNessuna valutazione finora

- Business Form Report ChecklistDocumento2 pagineBusiness Form Report ChecklistcaplusincNessuna valutazione finora

- Atkinson Management Accounting 6e Chapter 7 SolutionsDocumento39 pagineAtkinson Management Accounting 6e Chapter 7 SolutionsWilliam Antonio70% (10)

- Toyota Process Flow Analysis: ToyotaprocessflowanalysisDocumento5 pagineToyota Process Flow Analysis: ToyotaprocessflowanalysisRoel DavidNessuna valutazione finora

- Operations StrategyDocumento8 pagineOperations StrategyKhawaja Qureshi75% (4)

- RBAC Round 2 Case StudyDocumento18 pagineRBAC Round 2 Case StudyK60 Vũ Ngọc YếnNessuna valutazione finora

- Revamping The Supply ChainDocumento7 pagineRevamping The Supply ChainAndrea Dela CruzNessuna valutazione finora

- Advanced Audit and Assurance: Substantive TestsDocumento78 pagineAdvanced Audit and Assurance: Substantive TestsemeraldNessuna valutazione finora