Potrebbero piacerti anche

- Worksheet On Accounting For Partnership - Admission of A Partner Board QuestionsDocumento16 pagineWorksheet On Accounting For Partnership - Admission of A Partner Board QuestionsCfa Deepti Bindal100% (1)

- Insurance - Syllabus Atty ReyesDocumento11 pagineInsurance - Syllabus Atty ReyesZachary SiayngcoNessuna valutazione finora

- Final Accounts - AdjustmentsDocumento12 pagineFinal Accounts - AdjustmentsSarthak Gupta100% (1)

- Account Past Questions Compilation (2009june - 2020 Dec.)Documento246 pagineAccount Past Questions Compilation (2009june - 2020 Dec.)Prashant Sagar Gautam100% (2)

- MessageDocumento8 pagineMessagetecsevi45Nessuna valutazione finora

- Income and Expenditure Account AssignmentDocumento38 pagineIncome and Expenditure Account AssignmentMUHAMMAD HASSANNessuna valutazione finora

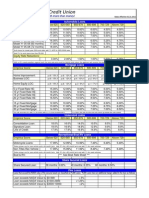

- Loan RatesDocumento1 paginaLoan RatesAndrew ChambersNessuna valutazione finora

- UCP 600 (Bilingual Version)Documento40 pagineUCP 600 (Bilingual Version)HendraImaSasmita85% (27)

- KVS Agra XII ACC QP & MS (Pre-Board) 23-24Documento21 pagineKVS Agra XII ACC QP & MS (Pre-Board) 23-24ragingcaverock696Nessuna valutazione finora

- Quezon City University: Bachelor of Science in AccountancyDocumento13 pagineQuezon City University: Bachelor of Science in AccountancyRiza Mae Alce50% (2)

- Financial StatementsDocumento3 pagineFinancial StatementsSoumendra RoyNessuna valutazione finora

- Credit Appraisal ReportDocumento125 pagineCredit Appraisal ReportSadaf IqbalNessuna valutazione finora

- Module 5 - Statement of Changes in Equity PDFDocumento7 pagineModule 5 - Statement of Changes in Equity PDFSandyNessuna valutazione finora

- CBSE Sample For Class 11 Accountancy (Solved) - Set ADocumento9 pagineCBSE Sample For Class 11 Accountancy (Solved) - Set Adhruba.sarkar3695Nessuna valutazione finora

- Final AccountsDocumento9 pagineFinal AccountsBhuvaneshwari Palani0% (2)

- MT799 PRE ADVISE PROCEDURE BUY-conversion-gate01Documento7 pagineMT799 PRE ADVISE PROCEDURE BUY-conversion-gate01paul_costas100% (2)

- CA Foundation June 23 BRS Problem - CTC ClassesDocumento2 pagineCA Foundation June 23 BRS Problem - CTC ClassesMohit SharmaNessuna valutazione finora

- Chapter 9 - Bank Reconciliation StatementDocumento15 pagineChapter 9 - Bank Reconciliation StatementSaurabh GohanNessuna valutazione finora

- Bank Re-Conciliation QuesDocumento3 pagineBank Re-Conciliation QuesGarima GarimaNessuna valutazione finora

- 5 Cash Book 08-2022 Regular 2023Documento8 pagine5 Cash Book 08-2022 Regular 2023jahnaviNessuna valutazione finora

- CA FND M23 - Cash Book QuestionsDocumento4 pagineCA FND M23 - Cash Book QuestionsRaaja YoganNessuna valutazione finora

- Model Paper, Accountancy, XIDocumento13 pagineModel Paper, Accountancy, XIanyaNessuna valutazione finora

- Accountancy Sample Paper Final ImportantDocumento18 pagineAccountancy Sample Paper Final ImportantChitra Vasu100% (1)

- Fin Account-Sole Trading AnswersDocumento10 pagineFin Account-Sole Trading AnswersAR Ananth Rohith BhatNessuna valutazione finora

- Bank Reconciliation StatementDocumento12 pagineBank Reconciliation StatementMillat AfridiNessuna valutazione finora

- Accountancy QPDocumento11 pagineAccountancy QPTûshar Thakúr0% (1)

- CBSE Quick Revision Notes and Chapter Summary: Class-11 Accountancy Chapter 1 - Introduction To AccountingDocumento6 pagineCBSE Quick Revision Notes and Chapter Summary: Class-11 Accountancy Chapter 1 - Introduction To AccountingSai Surya Stallone50% (2)

- Bos 28432 CP 14Documento53 pagineBos 28432 CP 14Basant Ojha100% (1)

- CBSE Class 11 Accountancy - Cash BookDocumento2 pagineCBSE Class 11 Accountancy - Cash BookMayankJhaNessuna valutazione finora

- Indira National School: AcademicDocumento55 pagineIndira National School: AcademicKrish VanvariNessuna valutazione finora

- Holding Company ProblemsDocumento22 pagineHolding Company ProblemsYashodhan MithareNessuna valutazione finora

- Fin Account-Sole Trading AnswersDocumento9 pagineFin Account-Sole Trading AnswersAR Ananth Rohith BhatNessuna valutazione finora

- Chapter 11 - Accounts From Incomplete RecordsDocumento15 pagineChapter 11 - Accounts From Incomplete RecordsShaji SNessuna valutazione finora

- Bcom Semester Iii Accounts Mega Revision Cum Suggestion PDFDocumento6 pagineBcom Semester Iii Accounts Mega Revision Cum Suggestion PDFAvirup ChakrabortyNessuna valutazione finora

- F Accountancy MS XI 2023-24Documento9 pagineF Accountancy MS XI 2023-24bhaiyarakesh100% (1)

- Joint Venture Accounts Hr-5Documento11 pagineJoint Venture Accounts Hr-5meenasarathaNessuna valutazione finora

- Problem in Subsidiary Book Cash BookDocumento2 pagineProblem in Subsidiary Book Cash Bookkamalkav0% (1)

- CertificateDocumento1 paginaCertificateRitaNessuna valutazione finora

- Worksheet BRSDocumento2 pagineWorksheet BRSCA Chhavi Gupta100% (1)

- Brs Practise SheetDocumento1 paginaBrs Practise Sheetapi-252642432Nessuna valutazione finora

- Rectification of Error IMP QUESTIONSDocumento5 pagineRectification of Error IMP QUESTIONSitsaakesh100% (1)

- Worksheet - Rectification of ErrorsDocumento3 pagineWorksheet - Rectification of ErrorsRajni Sinha VermaNessuna valutazione finora

- Ca Foundation All English HandoutsDocumento17 pagineCa Foundation All English HandoutsAditi DhimanNessuna valutazione finora

- 055 AccountancyDocumento15 pagine055 AccountancyHari prakarsh NimiNessuna valutazione finora

- Dissolution QuestionsDocumento5 pagineDissolution Questionsstudyystuff7Nessuna valutazione finora

- Admission of PartnerDocumento3 pagineAdmission of PartnerPraWin KharateNessuna valutazione finora

- CH 3 - BrsDocumento0 pagineCH 3 - BrsHaseeb Ullah KhanNessuna valutazione finora

- Art Integration Project by Shreya Namana Class Xii C Roll No. 45 Topic: GoodwillDocumento8 pagineArt Integration Project by Shreya Namana Class Xii C Roll No. 45 Topic: Goodwillshreya namana100% (2)

- Accounting 12Documento140 pagineAccounting 12sainimanish170gmailc0% (2)

- As 7 Construction ContractDocumento5 pagineAs 7 Construction ContractPankaj MeenaNessuna valutazione finora

- Class 11 Accountancy Project 2 Comprehensive ProblemDocumento9 pagineClass 11 Accountancy Project 2 Comprehensive ProblemANTELOPE CVNessuna valutazione finora

- Xii Mcqs CH - 4 Change in PSRDocumento4 pagineXii Mcqs CH - 4 Change in PSRJoanna GarciaNessuna valutazione finora

- Accountancy Class 11 Most Important Sample Paper 2023-2024Documento12 pagineAccountancy Class 11 Most Important Sample Paper 2023-2024Hardik ChhabraNessuna valutazione finora

- Comprehensive ProjectDocumento11 pagineComprehensive ProjectAKSH NAGARNessuna valutazione finora

- Ratio Analysis Rohit D. AkolkarDocumento21 pagineRatio Analysis Rohit D. AkolkarRajendra Gawate100% (1)

- F 2 Final AssessmentDocumento15 pagineF 2 Final Assessmentayazmustafa0% (1)

- CH 5 MCQ AccDocumento7 pagineCH 5 MCQ AccabiNessuna valutazione finora

- Purchase ConsiderationDocumento5 paginePurchase ConsiderationAR Ananth Rohith BhatNessuna valutazione finora

- Chapter 6 - Dissolution of Partnership Firm - Volume IDocumento41 pagineChapter 6 - Dissolution of Partnership Firm - Volume IVISHNUKUMAR S VNessuna valutazione finora

- AC Sample Paper 3 Unsolved-1Documento10 pagineAC Sample Paper 3 Unsolved-1Appharnha Rs0% (1)

- Past Adjustments QuestionsDocumento6 paginePast Adjustments QuestionsTanisha JainNessuna valutazione finora

- Chapter 6 Sol PDFDocumento81 pagineChapter 6 Sol PDFKrishnaNessuna valutazione finora

- Worksheet For Issue of Share and DebentureDocumento2 pagineWorksheet For Issue of Share and DebentureLaxmi Kant SahaniNessuna valutazione finora

- Partnership Accounts Fundamentals of Partnershi1Documento16 paginePartnership Accounts Fundamentals of Partnershi1ramandeep kaur100% (1)

- Cash Book - ProblemsDocumento3 pagineCash Book - ProblemsBrowse Purpose100% (2)

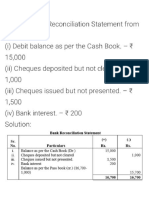

- Prepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookDocumento10 paginePrepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookPragya ShuklaNessuna valutazione finora

- Unit-Iii Bank Reconciliation Statement Debit (+) Credit (-) Credit (-) Debit (+)Documento6 pagineUnit-Iii Bank Reconciliation Statement Debit (+) Credit (-) Credit (-) Debit (+)aiswarya sNessuna valutazione finora

- BRS ProblemsDocumento28 pagineBRS ProblemsKutbuddin JawadwalaNessuna valutazione finora

- Codes Banking MICR Codes RBI 15102010 67440Documento1.455 pagineCodes Banking MICR Codes RBI 15102010 67440abhayarchivNessuna valutazione finora

- Authority of India (IRDA of India) After The Formal Declaration of Insurance Laws (Amendment)Documento3 pagineAuthority of India (IRDA of India) After The Formal Declaration of Insurance Laws (Amendment)hima binduNessuna valutazione finora

- NETS Prepaid Card Vs NETS FlashPay Comparison - v3.4Documento1 paginaNETS Prepaid Card Vs NETS FlashPay Comparison - v3.4TestNessuna valutazione finora

- Tutorial Test 5: 1. Three Types of ActivitiesDocumento4 pagineTutorial Test 5: 1. Three Types of ActivitiesVan Nguyen Thi HoangNessuna valutazione finora

- Assupol Life Cover - WebDocumento5 pagineAssupol Life Cover - WebtebkataneNessuna valutazione finora

- Bcom Paper Code: BCOM 314 Principles of InsuranceDocumento37 pagineBcom Paper Code: BCOM 314 Principles of InsuranceShajana ShahulNessuna valutazione finora

- SWOT ANALYSIS of PICIC BankDocumento4 pagineSWOT ANALYSIS of PICIC BankWasimOrakzai100% (3)

- Questions AnswersDocumento3 pagineQuestions AnswersajitNessuna valutazione finora

- Full Download Fundamentals of Corporate Finance Canadian 6th Edition Brealey Test BankDocumento35 pagineFull Download Fundamentals of Corporate Finance Canadian 6th Edition Brealey Test Banktantalicbos.qmdcdj100% (22)

- A Founder's Guide To M&A Deal Structure & AgreementDocumento4 pagineA Founder's Guide To M&A Deal Structure & AgreementYassine AlachbiliNessuna valutazione finora

- Axis Bank 2016-17Documento316 pagineAxis Bank 2016-17Vidya VijayanNessuna valutazione finora

- CH 4 Smart BookDocumento32 pagineCH 4 Smart BookEmi NguyenNessuna valutazione finora

- Capitalized Cost and GradientDocumento9 pagineCapitalized Cost and GradientNovy ArevaloNessuna valutazione finora

- Investment in Subsidiary Problem A - Equity Model and Cost ModelDocumento7 pagineInvestment in Subsidiary Problem A - Equity Model and Cost ModelJessica IslaNessuna valutazione finora

- Barcoma-Acce 412 (11435) - Reaction PaperDocumento2 pagineBarcoma-Acce 412 (11435) - Reaction PaperDiana Mae BarcomaNessuna valutazione finora

- Rectification of Errors Accounting Workbooks Zaheer SwatiDocumento6 pagineRectification of Errors Accounting Workbooks Zaheer SwatiZaheer SwatiNessuna valutazione finora

- التمويل بعقد المشاركة في المصارف الإسلاميةDocumento20 pagineالتمويل بعقد المشاركة في المصارف الإسلاميةNEXTWAY TECHNOLOGIENessuna valutazione finora

- PL Nov OktDocumento2 paginePL Nov OktKahfiNessuna valutazione finora

- Interim Financial ReportingDocumento20 pagineInterim Financial ReportingToni Rose Hernandez LualhatiNessuna valutazione finora

- CHP 11Documento41 pagineCHP 11SUBA NANTINI A/P M.SUBRAMANIAMNessuna valutazione finora

- Electronic Contribution Collection List SummaryDocumento12 pagineElectronic Contribution Collection List SummaryPbs Aurora PrinceNessuna valutazione finora

- Botswana Financial Sector OverviewDocumento45 pagineBotswana Financial Sector Overviewfk92Nessuna valutazione finora