Potrebbero piacerti anche

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Studies in The Life of ChristDocumento1.424 pagineStudies in The Life of ChristPhillip Gordon Mules100% (2)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- Contract A - Exam NotesDocumento36 pagineContract A - Exam NotesPhillip Gordon MulesNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Value Creation OikuusDocumento68 pagineValue Creation OikuusJefferson CuNessuna valutazione finora

- IBV - 2023 Global Outlook For Banking and Financial Markets PDFDocumento47 pagineIBV - 2023 Global Outlook For Banking and Financial Markets PDFСергей ЗайцевNessuna valutazione finora

- How To Write A Negligence Answer For Torts ExamDocumento4 pagineHow To Write A Negligence Answer For Torts ExamPhillip Gordon MulesNessuna valutazione finora

- Contract Law Cases - With AnswersDocumento5 pagineContract Law Cases - With AnswersPhillip Gordon MulesNessuna valutazione finora

- CORPORATE GOVERNANCE... PowerpointDocumento81 pagineCORPORATE GOVERNANCE... PowerpointEng Tennyson SigaukeNessuna valutazione finora

- HANA Presented SlidesDocumento102 pagineHANA Presented SlidesRao VedulaNessuna valutazione finora

- 8 Main Functions of MarketingDocumento8 pagine8 Main Functions of MarketingKavitaPatilNessuna valutazione finora

- CH 11Documento40 pagineCH 11Corliss Ko100% (1)

- Accrual Accounting Concepts PDFDocumento21 pagineAccrual Accounting Concepts PDFPhillip Gordon MulesNessuna valutazione finora

- Business Information Systems - Quiz 4Documento6 pagineBusiness Information Systems - Quiz 4Phillip Gordon MulesNessuna valutazione finora

- Information Systems in The EnterpriseDocumento4 pagineInformation Systems in The EnterprisePhillip Gordon MulesNessuna valutazione finora

- Marketing AssignmentDocumento16 pagineMarketing AssignmentPhillip Gordon MulesNessuna valutazione finora

- Economics For Managers - NotesDocumento17 pagineEconomics For Managers - NotesPhillip Gordon MulesNessuna valutazione finora

- HRM100 - Trends Report-Assignment 2Documento14 pagineHRM100 - Trends Report-Assignment 2Phillip Gordon MulesNessuna valutazione finora

- Economics For Managers - Notes-2Documento15 pagineEconomics For Managers - Notes-2Phillip Gordon MulesNessuna valutazione finora

- Economics For Managers - Notes-3Documento23 pagineEconomics For Managers - Notes-3Phillip Gordon MulesNessuna valutazione finora

- Practice Multiple Choice Questions - Final Exam HRM100 PDFDocumento10 paginePractice Multiple Choice Questions - Final Exam HRM100 PDFPhillip Gordon MulesNessuna valutazione finora

- Aristotle: Past Exam QuestionsDocumento1 paginaAristotle: Past Exam QuestionsPhillip Gordon MulesNessuna valutazione finora

- R V Droudis (No. 14) (2016) NSWSC 1550Documento23 pagineR V Droudis (No. 14) (2016) NSWSC 1550Phillip Gordon Mules100% (1)

- Aristotle Study QuestionsDocumento5 pagineAristotle Study QuestionsPhillip Gordon MulesNessuna valutazione finora

- ACC209 Managerial Accounting AssignmentDocumento2 pagineACC209 Managerial Accounting AssignmentMartin KKNessuna valutazione finora

- Finance 1 Case Study Sample 2013Documento7 pagineFinance 1 Case Study Sample 2013giorgiaNessuna valutazione finora

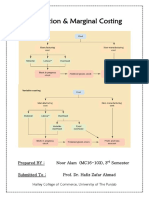

- Absorption & Marginal Costing - Noor Alam (MC16-103)Documento24 pagineAbsorption & Marginal Costing - Noor Alam (MC16-103)Ahmed Ali Khan100% (2)

- Unit 3 The Service ProductDocumento41 pagineUnit 3 The Service ProductKomal SuryavanshiNessuna valutazione finora

- F7-01 International Financial Reporting StandardsDocumento16 pagineF7-01 International Financial Reporting Standardssayedrushdi100% (1)

- Marketing Channels and Supply-Chain ManagementDocumento17 pagineMarketing Channels and Supply-Chain ManagementTala MuradNessuna valutazione finora

- Contents:: Introduction To Invoice VerificationDocumento13 pagineContents:: Introduction To Invoice VerificationpravanthbabuNessuna valutazione finora

- VP Finance Director CFO in Philadelphia PA Resume Thomas Della-FrancoDocumento3 pagineVP Finance Director CFO in Philadelphia PA Resume Thomas Della-FrancoThomasDellaFranco2Nessuna valutazione finora

- Market ResearchDocumento44 pagineMarket ResearchibmrNessuna valutazione finora

- Rehan Ahmad OriginalDocumento3 pagineRehan Ahmad OriginalhsaifNessuna valutazione finora

- Brookfield Asset Management Investor Day 2023Documento128 pagineBrookfield Asset Management Investor Day 2023chi.leNessuna valutazione finora

- Chapter 32 - Efficiency and Market FailureDocumento24 pagineChapter 32 - Efficiency and Market FailurePhuong DaoNessuna valutazione finora

- Chapter 1 Accounting Equation - Double Entry BookkeepingDocumento5 pagineChapter 1 Accounting Equation - Double Entry BookkeepingKate BlossomNessuna valutazione finora

- Family As A Source of Consumer-Based Brand EquityDocumento14 pagineFamily As A Source of Consumer-Based Brand EquityMarta RamalhoNessuna valutazione finora

- Air Bed &: BreakfastDocumento12 pagineAir Bed &: BreakfastPrateek VermaNessuna valutazione finora

- MB 2Documento16 pagineMB 2Shweta ShrivastavaNessuna valutazione finora

- What Went Wrong With Snapdeal and Way Forward Case StudyDocumento16 pagineWhat Went Wrong With Snapdeal and Way Forward Case StudyKrishnesh Lungani100% (1)

- Inventory Formula Excel TemplateDocumento4 pagineInventory Formula Excel TemplateMustafa Ricky Pramana SeNessuna valutazione finora

- Chapter1 - ch-01 - Introduction To Sales ManagementDocumento52 pagineChapter1 - ch-01 - Introduction To Sales ManagementChâu ChâuNessuna valutazione finora

- MIS Assignment 1Documento5 pagineMIS Assignment 1Teke TarekegnNessuna valutazione finora

- DocDocumento45 pagineDocYogesh KatnaNessuna valutazione finora

- Examination Question and Answers, Set A (True or False), Chapter 1 - Introduction To Accounting and BusinessDocumento2 pagineExamination Question and Answers, Set A (True or False), Chapter 1 - Introduction To Accounting and BusinessJohn Carlos DoringoNessuna valutazione finora

- 1.1 What Is Finance?Documento3 pagine1.1 What Is Finance?wasiuddinNessuna valutazione finora

- Summer Internship ReportDocumento69 pagineSummer Internship ReportShobhitShankhalaNessuna valutazione finora