Potrebbero piacerti anche

- Investment Objective Historical Performance: Pami Horizon Fund, IncDocumento1 paginaInvestment Objective Historical Performance: Pami Horizon Fund, IncRamil MontealtoNessuna valutazione finora

- Investment Objective Historical Performance: Philam Fund, IncDocumento1 paginaInvestment Objective Historical Performance: Philam Fund, IncWeas ChuckNessuna valutazione finora

- Ffs Pfi Jun 30 2019Documento1 paginaFfs Pfi Jun 30 2019Ramil MontealtoNessuna valutazione finora

- Fund Allocation Investment Objective: Pami Equity Index Fund, IncDocumento1 paginaFund Allocation Investment Objective: Pami Equity Index Fund, IncRamil MontealtoNessuna valutazione finora

- Investment Objective NAVPS Graph: Philam Bond Fund, IncDocumento1 paginaInvestment Objective NAVPS Graph: Philam Bond Fund, IncRamil MontealtoNessuna valutazione finora

- I Balanced Fund Apr 23Documento3 pagineI Balanced Fund Apr 23mid_cycloneNessuna valutazione finora

- MP - 3 - Peso Growth FundDocumento2 pagineMP - 3 - Peso Growth FundFrank TaquioNessuna valutazione finora

- Asset Allocation Fund (5) : Hybrid Hybrid BalancedDocumento2 pagineAsset Allocation Fund (5) : Hybrid Hybrid BalancedHayston DezmenNessuna valutazione finora

- Annual Investment Report 2016-17Documento15 pagineAnnual Investment Report 2016-17DARSHANNessuna valutazione finora

- Peso Emperor Fund - Fund Fact Sheet - October - 2020Documento2 paginePeso Emperor Fund - Fund Fact Sheet - October - 2020Jayr LegaspiNessuna valutazione finora

- Peso Wealth Optimizer Fund 2036 - Fund Fact Sheet - December - 2020Documento3 paginePeso Wealth Optimizer Fund 2036 - Fund Fact Sheet - December - 2020Jayr LegaspiNessuna valutazione finora

- Peso Emperor Fund - Fund Fact Sheet - December - 2020Documento2 paginePeso Emperor Fund - Fund Fact Sheet - December - 2020Jayr LegaspiNessuna valutazione finora

- AD15 June11Documento2 pagineAD15 June11Alvin LimNessuna valutazione finora

- Fund Fact Sheets NAVPU Captains FundDocumento1 paginaFund Fact Sheets NAVPU Captains FundJohh-RevNessuna valutazione finora

- Conservative at Least Five (5) Years: Account of The ClientDocumento2 pagineConservative at Least Five (5) Years: Account of The ClientkimencinaNessuna valutazione finora

- 9-17-19 TR Presentation (9!16!19 Market Update) - UnlockedDocumento58 pagine9-17-19 TR Presentation (9!16!19 Market Update) - UnlockedZerohedge100% (3)

- ML Participating Fund Letter PDFDocumento4 pagineML Participating Fund Letter PDFFredrick TimotiusNessuna valutazione finora

- Johore Tin (Johotin-Ku) : Average ScoreDocumento11 pagineJohore Tin (Johotin-Ku) : Average ScoreIqbal YusufNessuna valutazione finora

- Hybrid Fund Completes 5 Years NoteDocumento3 pagineHybrid Fund Completes 5 Years NoteMohamed Rajiv AshaNessuna valutazione finora

- ATRAM Phil Equity Smart Index Fund Fact Sheet Jan 2022Documento2 pagineATRAM Phil Equity Smart Index Fund Fact Sheet Jan 2022jvNessuna valutazione finora

- Strategic Bond Fund (59) : Fixed Income Investment GradeDocumento2 pagineStrategic Bond Fund (59) : Fixed Income Investment GradeHayston DezmenNessuna valutazione finora

- Peso Asia Pacific Property Income Fund - Fund Fact Sheet - October - 2020Documento2 paginePeso Asia Pacific Property Income Fund - Fund Fact Sheet - October - 2020Jayr LegaspiNessuna valutazione finora

- Intermediate Term Bond FundDocumento1 paginaIntermediate Term Bond FundYannah HidalgoNessuna valutazione finora

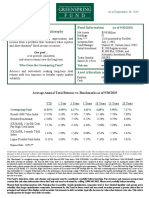

- Greenspring Fund Philosophy Fund Information: (As of 9/30/2019)Documento2 pagineGreenspring Fund Philosophy Fund Information: (As of 9/30/2019)Anonymous TtkcZvPNessuna valutazione finora

- Philequity Peso Bond Fund: Navps As of Dec 27, 2019Documento1 paginaPhilequity Peso Bond Fund: Navps As of Dec 27, 2019Marlon DNessuna valutazione finora

- 2021 DECEMBER Fund-Fact-SheetDocumento41 pagine2021 DECEMBER Fund-Fact-SheetRyan Jacob SolisNessuna valutazione finora

- Singapore Dynamic Bond Fund: Investment ObjectiveDocumento2 pagineSingapore Dynamic Bond Fund: Investment ObjectiveXavier Alexen AseronNessuna valutazione finora

- BF Fund Fact Sheet Sep 2023Documento2 pagineBF Fund Fact Sheet Sep 2023DAR RYLNessuna valutazione finora

- I Income Fund Apr 23Documento3 pagineI Income Fund Apr 23mid_cycloneNessuna valutazione finora

- Peso Powerhouse Fund - Fund Fact Sheet - December - 2020Documento2 paginePeso Powerhouse Fund - Fund Fact Sheet - December - 2020Jayr LegaspiNessuna valutazione finora

- Investmentz AugustDocumento11 pagineInvestmentz AugustAnimesh PalNessuna valutazione finora

- Old Mutual Global Macro Equity StrategyDocumento2 pagineOld Mutual Global Macro Equity StrategyTeboho QholoshaNessuna valutazione finora

- Market Highlights PDFDocumento8 pagineMarket Highlights PDFPranati BhattacharjeeNessuna valutazione finora

- ALFM Peso Bond FundDocumento2 pagineALFM Peso Bond FundkimencinaNessuna valutazione finora

- 3-17-2020 Jeffrey Gundlach Total Return Presentation-UnlockedDocumento82 pagine3-17-2020 Jeffrey Gundlach Total Return Presentation-UnlockedZerohedge100% (3)

- Eq Uitf Bpi Gefof Nov 2017Documento4 pagineEq Uitf Bpi Gefof Nov 2017Jelor GallegoNessuna valutazione finora

- Fact Sheet Affin Hwang World Series - China Allocation Opportunity FundDocumento1 paginaFact Sheet Affin Hwang World Series - China Allocation Opportunity FundHenry So E DiarkoNessuna valutazione finora

- Government Money Market I Fund (6) : Fixed Income Stable ValueDocumento2 pagineGovernment Money Market I Fund (6) : Fixed Income Stable ValueiuxhpccxNessuna valutazione finora

- Conf Call TranscriptDocumento28 pagineConf Call Transcriptsandy_caponeNessuna valutazione finora

- India's No.1 Portfolio Management Services PortalDocumento1 paginaIndia's No.1 Portfolio Management Services Portalrahul patelNessuna valutazione finora

- Fund Fact Sheets - Prosperity Bond FundDocumento1 paginaFund Fact Sheets - Prosperity Bond FundJeuz Llorenz Colendra-ApitaNessuna valutazione finora

- AlchemyDocumento8 pagineAlchemyAshwin HasyagarNessuna valutazione finora

- PIALEFDocumento1 paginaPIALEFEileen LauNessuna valutazione finora

- Bpi Us Equity Index Feeder Fund Key Information and Investment Disclosure Statement As of July 31, 2018 Fund FactsDocumento3 pagineBpi Us Equity Index Feeder Fund Key Information and Investment Disclosure Statement As of July 31, 2018 Fund FactsMartin MartelNessuna valutazione finora

- 6 - Kiid - Uitf - Eq - Bpi Eq - Jun2015Documento3 pagine6 - Kiid - Uitf - Eq - Bpi Eq - Jun2015Nonami AbicoNessuna valutazione finora

- Capital Appreciation - All Equity PortfolioDocumento2 pagineCapital Appreciation - All Equity PortfolioDwi Rizki Anisa PandiaNessuna valutazione finora

- Growth & Guarantee Is Now Reality: Diamond Saving PlanDocumento2 pagineGrowth & Guarantee Is Now Reality: Diamond Saving PlanMaulik PanchmatiaNessuna valutazione finora

- H Strategic BondDocumento2 pagineH Strategic BondDaniel GauciNessuna valutazione finora

- 2q19 Eaof LetterDocumento13 pagine2q19 Eaof LetterDavid BriggsNessuna valutazione finora

- First Metro Save and Learn Fixed Income FundDocumento1 paginaFirst Metro Save and Learn Fixed Income FundkimencinaNessuna valutazione finora

- Gundlach Pres June 2017Documento57 pagineGundlach Pres June 2017Zerohedge100% (6)

- Mitsubishi UFJ Financial Group Inc MUFG (XNYS) : MUFG Also Reports Modest Uptick in Credit Costs in 3Q We Prefer SMFGDocumento14 pagineMitsubishi UFJ Financial Group Inc MUFG (XNYS) : MUFG Also Reports Modest Uptick in Credit Costs in 3Q We Prefer SMFGAnonymous P73cUg73LNessuna valutazione finora

- GreatlinkenhancerfundDocumento2 pagineGreatlinkenhancerfundswifthawkNessuna valutazione finora

- Bdo Peso Money Market Fund: As A Percentage of Average Daily NAV For The Month Valued at PHP 85.457 BillionDocumento7 pagineBdo Peso Money Market Fund: As A Percentage of Average Daily NAV For The Month Valued at PHP 85.457 Billionk100% (1)

- Shinhan Supreme Balance FundDocumento1 paginaShinhan Supreme Balance FundhhhahaNessuna valutazione finora

- Equity Fund: % Top 10 Holding As On 31st March 2019Documento1 paginaEquity Fund: % Top 10 Holding As On 31st March 2019Sajith KumarNessuna valutazione finora

- 2015 Ci Harbour F ClassDocumento3 pagine2015 Ci Harbour F ClassMarcelo MedeirosNessuna valutazione finora

- Discovery Fund April 23Documento1 paginaDiscovery Fund April 23Satyajeet AnandNessuna valutazione finora

- Spandana Sphoorty Financial Limited - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDocumento7 pagineSpandana Sphoorty Financial Limited - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNessuna valutazione finora

- DIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)Da EverandDIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)Nessuna valutazione finora

- Construction: James L. DulaliaDocumento17 pagineConstruction: James L. DulaliaKamille Anne GabaynoNessuna valutazione finora

- 2021 Schedule of Finishes MAPLE ModelDocumento1 pagina2021 Schedule of Finishes MAPLE ModelKamille Anne GabaynoNessuna valutazione finora

- Commercial, STD, FLORO - Water Reading Monitoring REV 05222021Documento39 pagineCommercial, STD, FLORO - Water Reading Monitoring REV 05222021Kamille Anne GabaynoNessuna valutazione finora

- CHB Inventory: 3-Jun-20 WedDocumento4 pagineCHB Inventory: 3-Jun-20 WedKamille Anne GabaynoNessuna valutazione finora

- Sub-Contractor Accomplishment Report: Ronito MacapazDocumento15 pagineSub-Contractor Accomplishment Report: Ronito MacapazKamille Anne GabaynoNessuna valutazione finora

- Construction: James L. DulaliaDocumento17 pagineConstruction: James L. DulaliaKamille Anne GabaynoNessuna valutazione finora

- Summary of Work May 21 To May 27 ValDocumento2 pagineSummary of Work May 21 To May 27 ValKamille Anne GabaynoNessuna valutazione finora

- Thursday, August 06, 2020, 02:29 PM: Page 1 of 135 C:/Users/Rose/Desktop/work/Structure1.anlDocumento135 pagineThursday, August 06, 2020, 02:29 PM: Page 1 of 135 C:/Users/Rose/Desktop/work/Structure1.anlKamille Anne GabaynoNessuna valutazione finora

- Summary of Work May 21 To May 27 BangaDocumento3 pagineSummary of Work May 21 To May 27 BangaKamille Anne GabaynoNessuna valutazione finora

- Prod Rate Man-HourDocumento10 pagineProd Rate Man-HourKamille Anne GabaynoNessuna valutazione finora

- List of Products NeededDocumento28 pagineList of Products NeededKamille Anne GabaynoNessuna valutazione finora

- Status With PictureDocumento26 pagineStatus With PictureKamille Anne GabaynoNessuna valutazione finora

- Roof Gutter TdsDocumento3 pagineRoof Gutter TdsKamille Anne GabaynoNessuna valutazione finora

- Angeluz Memorial ParkDocumento2 pagineAngeluz Memorial ParkKamille Anne GabaynoNessuna valutazione finora

- Weekly Accomplishment Report: Nucum Orcullo Dela CruzDocumento3 pagineWeekly Accomplishment Report: Nucum Orcullo Dela CruzKamille Anne GabaynoNessuna valutazione finora

- Angeluz Memorial ParkDocumento4 pagineAngeluz Memorial ParkKamille Anne GabaynoNessuna valutazione finora

- Butchery Business Plan-1Documento12 pagineButchery Business Plan-1Andrew LukupwaNessuna valutazione finora

- Chapter 3Documento5 pagineChapter 3Elsa Mendoza50% (2)

- ASP Zakat PPT FinalDocumento13 pagineASP Zakat PPT FinalDionysius Ivan HertantoNessuna valutazione finora

- Lect 12 EOQ SCMDocumento38 pagineLect 12 EOQ SCMApporva MalikNessuna valutazione finora

- Company DetailsDocumento8 pagineCompany DetailsVikash Kumar SinghNessuna valutazione finora

- Unka VAT WithholdingDocumento1 paginaUnka VAT WithholdingGar KooNessuna valutazione finora

- Answers in English For Academic and Professional Purposes: Name: Grade and Section: 1 TeacherDocumento22 pagineAnswers in English For Academic and Professional Purposes: Name: Grade and Section: 1 TeacherSherilyn DiazNessuna valutazione finora

- White Revolution in IndiaDocumento57 pagineWhite Revolution in IndiaPiyush Gaur0% (3)

- Fractional Share FormulaDocumento1 paginaFractional Share FormulainboxnewsNessuna valutazione finora

- Entrepreneurship 11/12 First: Learning Area Grade Level Quarter DateDocumento4 pagineEntrepreneurship 11/12 First: Learning Area Grade Level Quarter DateDivine Mermal0% (1)

- FINAL REPORT 2-1 Final FinalDocumento24 pagineFINAL REPORT 2-1 Final FinalDecoy1 Decoy1Nessuna valutazione finora

- Ashish Chugh Reveals Top Secrets To Finding Multibagger StocksDocumento10 pagineAshish Chugh Reveals Top Secrets To Finding Multibagger StocksSreenivasulu E NNessuna valutazione finora

- An Assignment: Case Study of Dell Inc.-Push or Pull?Documento3 pagineAn Assignment: Case Study of Dell Inc.-Push or Pull?Shahbaz NaserNessuna valutazione finora

- Cost Management Cloud: Receipt AccountingDocumento14 pagineCost Management Cloud: Receipt Accountinghaitham ibrahem mohmedNessuna valutazione finora

- Đề thi tiếng Anh chuyên ngành Tài chính Ngân hàng 1Documento4 pagineĐề thi tiếng Anh chuyên ngành Tài chính Ngân hàng 1Hoang TrieuNessuna valutazione finora

- NBP HR Report-FinalDocumento58 pagineNBP HR Report-FinalMaqbool Jehangir100% (1)

- Induction Acknowledgement-1Documento3 pagineInduction Acknowledgement-1aal.majeed14Nessuna valutazione finora

- Conferring Rights On Citizens-Laws and Their Implementation: Ijpa Jan - March 014Documento11 pagineConferring Rights On Citizens-Laws and Their Implementation: Ijpa Jan - March 014Mayuresh DalviNessuna valutazione finora

- Session 3 Unit 3 Analysis On Inventory ManagementDocumento18 pagineSession 3 Unit 3 Analysis On Inventory ManagementAyesha RachhNessuna valutazione finora

- Appendix 2: Revenue and Expenditures of Chaman BCP From Year 01 To YearDocumento1 paginaAppendix 2: Revenue and Expenditures of Chaman BCP From Year 01 To YearKAshif UMarNessuna valutazione finora

- Ap Macroeconomics Syllabus - MillsDocumento6 pagineAp Macroeconomics Syllabus - Millsapi-311407406Nessuna valutazione finora

- AU Small Finance Bank - Research InsightDocumento6 pagineAU Small Finance Bank - Research InsightDickson KulluNessuna valutazione finora

- Review 105 - Day 17 P1: How Much of The Proceeds From The Issuance of Convertible Bonds Should Be Allocated To Equity?Documento10 pagineReview 105 - Day 17 P1: How Much of The Proceeds From The Issuance of Convertible Bonds Should Be Allocated To Equity?sino akoNessuna valutazione finora

- Case 7Documento2 pagineCase 7Manas Kotru100% (1)

- Chapter 4Documento2 pagineChapter 4Dai Huu0% (1)

- Revenue Memorandum Circular No. 07-96Documento2 pagineRevenue Memorandum Circular No. 07-96rnrbac67% (3)

- Week 14: Game Theory and Pricing Strategies Game TheoryDocumento3 pagineWeek 14: Game Theory and Pricing Strategies Game Theorysherryl caoNessuna valutazione finora

- Global SOUTH & Global NORTHDocumento13 pagineGlobal SOUTH & Global NORTHswamini.k65Nessuna valutazione finora

- Foundation of Economics NotesDocumento16 pagineFoundation of Economics Notesrosa100% (1)

- Wave SetupsDocumento15 pagineWave SetupsRhino382100% (9)