Potrebbero piacerti anche

- Schaum's Outline of Principles of Accounting I, Fifth EditionDa EverandSchaum's Outline of Principles of Accounting I, Fifth EditionValutazione: 5 su 5 stelle5/5 (3)

- MA1 - De thi giua ky - HK2 - 21-22 - send-đã chuyển đổiDocumento4 pagineMA1 - De thi giua ky - HK2 - 21-22 - send-đã chuyển đổiThu ThanhNessuna valutazione finora

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsDa EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNessuna valutazione finora

- 03 Overhead CostingDocumento9 pagine03 Overhead CostingPappu LalNessuna valutazione finora

- 13 OhDocumento12 pagine13 OhLakshay SharmaNessuna valutazione finora

- Seminar Week 2Documento2 pagineSeminar Week 2JaquinNessuna valutazione finora

- Overhead Analysis Solution 1Documento2 pagineOverhead Analysis Solution 1Humphrey OsaigbeNessuna valutazione finora

- Chapter 4 Overhead ProblemsDocumento5 pagineChapter 4 Overhead Problemsthiluvnddi100% (1)

- Tutorial OverheadDocumento6 pagineTutorial OverheadImran FarhanNessuna valutazione finora

- Chapter 5 ExercisesDocumento12 pagineChapter 5 ExercisesIsaiah BatucanNessuna valutazione finora

- ACMA Unit 6 Problems - Overheads PDFDocumento4 pagineACMA Unit 6 Problems - Overheads PDFPrabhat SinghNessuna valutazione finora

- CH5 CostDocumento33 pagineCH5 CostNickey DickeyNessuna valutazione finora

- TYBCOM - Cost - OverheadsDocumento8 pagineTYBCOM - Cost - Overheadsmkbooks4uNessuna valutazione finora

- Unit 2 - Question BankDocumento34 pagineUnit 2 - Question BankTamaraNessuna valutazione finora

- Publishing Company Question: Service Department Operating Department A B C 1 2 TotalDocumento3 paginePublishing Company Question: Service Department Operating Department A B C 1 2 Totalisrael adesanyaNessuna valutazione finora

- Accounting For FOH Part 11Documento16 pagineAccounting For FOH Part 11Shania LiwanagNessuna valutazione finora

- Chapter 6 OverheadsDocumento3 pagineChapter 6 OverheadsDevender SinghNessuna valutazione finora

- Unit 3 Overheads - Tutorial SheetDocumento4 pagineUnit 3 Overheads - Tutorial SheetJust for Silly UseNessuna valutazione finora

- Tutorial 2 - Ch3Documento2 pagineTutorial 2 - Ch3Codreanu AndaNessuna valutazione finora

- Arcadia and Enterprise Co. Worked ExamplesDocumento22 pagineArcadia and Enterprise Co. Worked ExamplesIvy TulesiNessuna valutazione finora

- Lecture 14 POADocumento7 pagineLecture 14 POALau Chun GuiNessuna valutazione finora

- Hand-Out 4 - ABC and Support Cost AllocationDocumento2 pagineHand-Out 4 - ABC and Support Cost AllocationJerric CristobalNessuna valutazione finora

- Cost Accounting 7 & 8Documento26 pagineCost Accounting 7 & 8Kyrara79% (19)

- Cost & Management Accounting - MGT402 Power Point Slides Lecture 15Documento22 pagineCost & Management Accounting - MGT402 Power Point Slides Lecture 15Mr. JalilNessuna valutazione finora

- Lille Tissage WorksheetDocumento19 pagineLille Tissage WorksheetJaouadiNessuna valutazione finora

- PROBLEM 2-45:: Particulars Case A Case B Case CDocumento6 paginePROBLEM 2-45:: Particulars Case A Case B Case CSrihari KumarNessuna valutazione finora

- Cost Accounting 7 & 8Documento29 pagineCost Accounting 7 & 8Kyrara70% (20)

- Activity 1 PDFDocumento2 pagineActivity 1 PDFnimeshaNessuna valutazione finora

- Chapter 10Documento22 pagineChapter 10Dan ChuaNessuna valutazione finora

- OverheadApportionment 7Documento5 pagineOverheadApportionment 7mitsob27Nessuna valutazione finora

- Example Overheards Allocation 1Documento4 pagineExample Overheards Allocation 1Phomolo StoffelNessuna valutazione finora

- Overhead Question WalkthroughDocumento38 pagineOverhead Question WalkthroughaliahamirworksNessuna valutazione finora

- 21st - OCTOBER - 2022-TODAY CLASS - DotDocumento23 pagine21st - OCTOBER - 2022-TODAY CLASS - DotPalesaNessuna valutazione finora

- Cost Accounting Level 3/series 4 2008 (3016)Documento20 pagineCost Accounting Level 3/series 4 2008 (3016)Hein Linn Kyaw0% (1)

- Financial Plan: and Economic ChallengesDocumento5 pagineFinancial Plan: and Economic ChallengesEmmanuel AkoloNessuna valutazione finora

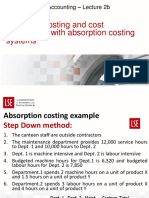

- Job-Order Costing and Cost Assignment With Absorption Costing SystemsDocumento50 pagineJob-Order Costing and Cost Assignment With Absorption Costing SystemsAnh Quan NguyenNessuna valutazione finora

- Soalan2 Quiz Chapter 3Documento8 pagineSoalan2 Quiz Chapter 3biarrahsiaNessuna valutazione finora

- Costco2-Quiz End-TermDocumento4 pagineCostco2-Quiz End-TermmhikeedelantarNessuna valutazione finora

- 3 RTP Nov 21Documento34 pagine3 RTP Nov 21Bharath Krishna MVNessuna valutazione finora

- 66088bos53351inter p3Documento34 pagine66088bos53351inter p3Asfarin ShaikhNessuna valutazione finora

- The Other: Cost AccowntingDocumento7 pagineThe Other: Cost AccowntingLakshmi SNessuna valutazione finora

- Acc271215 OhdDocumento4 pagineAcc271215 Ohdbasilimagambo22Nessuna valutazione finora

- Cost CenterDocumento6 pagineCost CenterBen DoverNessuna valutazione finora

- CA Solution ManualDocumento27 pagineCA Solution ManualClarisse Pelayo100% (1)

- Problem 14Documento2 pagineProblem 14Nepal Bishal ShresthaNessuna valutazione finora

- Cost Management AssignmentDocumento29 pagineCost Management AssignmentInanda MeitasariNessuna valutazione finora

- Financial Plan (Illustration)Documento6 pagineFinancial Plan (Illustration)rana samiNessuna valutazione finora

- @ProCA - Inter Contract Costing Past Exam QuestionsDocumento10 pagine@ProCA - Inter Contract Costing Past Exam QuestionscallbvipinjainNessuna valutazione finora

- Book 1Documento12 pagineBook 1Vincent Luigil AlceraNessuna valutazione finora

- SM CSE ACT 301 Final AssessmentDocumento4 pagineSM CSE ACT 301 Final AssessmentArifur Rahaman 182-15-2111Nessuna valutazione finora

- Traditional Approaches To Full Costing Answers To End of Chapter ExercisesDocumento4 pagineTraditional Approaches To Full Costing Answers To End of Chapter ExercisesJay BrockNessuna valutazione finora

- Mystic SportsDocumento34 pagineMystic SportshelloNessuna valutazione finora

- Chapter 3 Overheads: Joudat Ali Malik ACMA, APFA, MA (Economics), CFC (Canada)Documento8 pagineChapter 3 Overheads: Joudat Ali Malik ACMA, APFA, MA (Economics), CFC (Canada)sarahNessuna valutazione finora

- AS - Cost Accountting 3 - Past PaperDocumento6 pagineAS - Cost Accountting 3 - Past PaperAvikamm AgrawalNessuna valutazione finora

- Sagip Chapter 8Documento7 pagineSagip Chapter 8Christopherchan ChanNessuna valutazione finora

- Absorption (Total) Costing AnswersDocumento7 pagineAbsorption (Total) Costing AnswersNalan TafanaNessuna valutazione finora

- Financial Plan OkDocumento7 pagineFinancial Plan OkSYED ARSALANNessuna valutazione finora

- AE 22 - MOH - DepartmentalizationDocumento4 pagineAE 22 - MOH - DepartmentalizationJake BorinagaNessuna valutazione finora

- Mba 2013 QP PDFDocumento108 pagineMba 2013 QP PDFdeepakagarwallaNessuna valutazione finora

- SG Botanic GardensDocumento1 paginaSG Botanic GardensKos PaviliunNessuna valutazione finora

- Parent Fellowship, May 2, 2020Documento1 paginaParent Fellowship, May 2, 2020Kos PaviliunNessuna valutazione finora

- EconomicsDocumento1 paginaEconomicsKos PaviliunNessuna valutazione finora

- SpeakingDocumento1 paginaSpeakingKos PaviliunNessuna valutazione finora

- Answer 11Documento3 pagineAnswer 11Kos PaviliunNessuna valutazione finora

- LivingDocumento1 paginaLivingKos PaviliunNessuna valutazione finora

- Answer 11Documento3 pagineAnswer 11Kos PaviliunNessuna valutazione finora

- Answer 9 Revised 11janDocumento4 pagineAnswer 9 Revised 11janKos PaviliunNessuna valutazione finora

- Variable Costing: A Tool For Management: Garrison, Noreen, Brewer, Cheng & Yuen Mcgraw-Hill Education (Asia)Documento79 pagineVariable Costing: A Tool For Management: Garrison, Noreen, Brewer, Cheng & Yuen Mcgraw-Hill Education (Asia)Kos PaviliunNessuna valutazione finora

- Management and Cost Accounting: Colin DruryDocumento17 pagineManagement and Cost Accounting: Colin DruryKos PaviliunNessuna valutazione finora

- Answer10 Revised 11janDocumento3 pagineAnswer10 Revised 11janKos PaviliunNessuna valutazione finora

- ACCT6173-Managerial Accounting: Week 10 Differential Analysis: The Key To Decision MakingDocumento30 pagineACCT6173-Managerial Accounting: Week 10 Differential Analysis: The Key To Decision MakingKos PaviliunNessuna valutazione finora

- P6 Maths SA1 2017 Catholic High Exam PapersDocumento40 pagineP6 Maths SA1 2017 Catholic High Exam PapersKos PaviliunNessuna valutazione finora

- Materi Transfer PricingDocumento20 pagineMateri Transfer Pricingteamjkt48merchNessuna valutazione finora

- P6 English CA1 2017 ACS Exam Papers PDFDocumento22 pagineP6 English CA1 2017 ACS Exam Papers PDFKos PaviliunNessuna valutazione finora

- P6 Maths CA1 2017 Nanyang Exam PapersDocumento40 pagineP6 Maths CA1 2017 Nanyang Exam PapersKos PaviliunNessuna valutazione finora

- Exam PapersDocumento36 pagineExam PapersKos PaviliunNessuna valutazione finora

- P6 Maths CA1 2017 ST Nicholas Exam PapersDocumento37 pagineP6 Maths CA1 2017 ST Nicholas Exam PapersKos PaviliunNessuna valutazione finora

- Primary Six Math Sample Paper PDFDocumento33 paginePrimary Six Math Sample Paper PDFKos PaviliunNessuna valutazione finora

- P6 Maths CA1 2017 Nanyang Exam PapersDocumento38 pagineP6 Maths CA1 2017 Nanyang Exam PapersKos PaviliunNessuna valutazione finora

- P6 Maths SA2 2017 ST Nicholas Exam PapersDocumento44 pagineP6 Maths SA2 2017 ST Nicholas Exam PapersKos PaviliunNessuna valutazione finora

- Apparel Roi CalculatorDocumento3 pagineApparel Roi CalculatorRezza AdityaNessuna valutazione finora

- Feasibility Analysis and Business Plan IntroDocumento41 pagineFeasibility Analysis and Business Plan IntroRicardo Oneil AfflickNessuna valutazione finora

- PLDT vs. NTCDocumento2 paginePLDT vs. NTCI took her to my penthouse and i freaked itNessuna valutazione finora

- Appendix 26 - Instructions - RCDDocumento2 pagineAppendix 26 - Instructions - RCDthessa_starNessuna valutazione finora

- Various Letters Set1Documento64 pagineVarious Letters Set1Marcus Roland50% (2)

- 07 Segment Reporting 1Documento4 pagine07 Segment Reporting 1Irtiza AbbasNessuna valutazione finora

- Key Finding IFRS For Banking in Laos at BoLDocumento56 pagineKey Finding IFRS For Banking in Laos at BoLMiladNessuna valutazione finora

- Homework Assignment 1 KeyDocumento6 pagineHomework Assignment 1 KeymetetezcanNessuna valutazione finora

- AI - Materi 9 Analisis LK InternasDocumento21 pagineAI - Materi 9 Analisis LK Internasbams_febNessuna valutazione finora

- Enabling Clean Energy Access With Smart CookingDocumento4 pagineEnabling Clean Energy Access With Smart CookingLam Thuc NghiNessuna valutazione finora

- Manual Steps SAPNote 1699985Documento3 pagineManual Steps SAPNote 1699985chandrasekha3975Nessuna valutazione finora

- BCG CII India Future of Jobs Mar 2017Documento48 pagineBCG CII India Future of Jobs Mar 2017Learning EngineerNessuna valutazione finora

- Audit of The Capital Acquisition and Repayment CycleDocumento20 pagineAudit of The Capital Acquisition and Repayment Cycleputri retno100% (1)

- Chapter 7 Pricing Strategies: You Don 'T Sell Through Price. You Sell The PriceDocumento30 pagineChapter 7 Pricing Strategies: You Don 'T Sell Through Price. You Sell The Priceabhi7219Nessuna valutazione finora

- Introduction To Investment BankingDocumento45 pagineIntroduction To Investment BankingHuế ThùyNessuna valutazione finora

- FIMA 30013 FS Analysis Premium Notes P1Documento5 pagineFIMA 30013 FS Analysis Premium Notes P1dcdeguzman.pup.pulilanNessuna valutazione finora

- Abm Business Mathematics Reading Materials 2019Documento16 pagineAbm Business Mathematics Reading Materials 2019Nardsdel Rivera100% (1)

- A Research Paper On Investment Awareness Among IndianDocumento18 pagineA Research Paper On Investment Awareness Among IndianElaisa AurinNessuna valutazione finora

- Business AccountingDocumento1.108 pagineBusiness AccountingAhmad Haikal100% (1)

- Farley Alan - 20 Rules For The Master Swing Trader PDFDocumento5 pagineFarley Alan - 20 Rules For The Master Swing Trader PDFLuís MiguelNessuna valutazione finora

- First National City Bank of New York Vs Tan - G.R. No. L-14234. February 28, 1962Documento4 pagineFirst National City Bank of New York Vs Tan - G.R. No. L-14234. February 28, 1962RonStephaneMaylonNessuna valutazione finora

- Financial Inclusion Policy - An Inclusive Financial Sector For AllDocumento118 pagineFinancial Inclusion Policy - An Inclusive Financial Sector For AllwNessuna valutazione finora

- Businessmathoct19 (Autosaved)Documento19 pagineBusinessmathoct19 (Autosaved)Andrea GalangNessuna valutazione finora

- Final DVADocumento84 pagineFinal DVAĐoàn Minh TríNessuna valutazione finora

- Bond Solvency Form 2018-19Documento4 pagineBond Solvency Form 2018-19Mohit PatelNessuna valutazione finora

- LTCCDocumento16 pagineLTCCandzie09876Nessuna valutazione finora

- Bond Markets in The MENA RegionDocumento59 pagineBond Markets in The MENA RegionstephaniNessuna valutazione finora

- Dell Working Capital Solution ExplainedDocumento15 pagineDell Working Capital Solution ExplainedFarabi AhmedNessuna valutazione finora

- 6 Fiscal PolicyDocumento792 pagine6 Fiscal Policywerner71100% (1)

- PRMB PDFDocumento13 paginePRMB PDFkshitijsaxenaNessuna valutazione finora