Potrebbero piacerti anche

- CheckingStatement BoA 30 11 2020 30 12 2020Documento3 pagineCheckingStatement BoA 30 11 2020 30 12 2020xxalias100% (3)

- CFPB Consumer Reporting Companies ListDocumento35 pagineCFPB Consumer Reporting Companies Listgabby maca100% (2)

- Starting A Six Figure Credit Repair BusinessDocumento40 pagineStarting A Six Figure Credit Repair BusinessLuz Velez100% (1)

- How To Sue TelemarketersDocumento15 pagineHow To Sue TelemarketersPaul J. TaylorNessuna valutazione finora

- 7 Steps To Disputing Re-Aged DebtDocumento3 pagine7 Steps To Disputing Re-Aged Debt:James-Wesley.Nessuna valutazione finora

- Competition DemystifiedDocumento9 pagineCompetition DemystifiedTim JoyceNessuna valutazione finora

- PayMongo Memorandum of AgreementDocumento14 paginePayMongo Memorandum of AgreementMakuto MitsuharaNessuna valutazione finora

- Debt Management 101 - How To Get Out Of Debt FastDa EverandDebt Management 101 - How To Get Out Of Debt FastValutazione: 4 su 5 stelle4/5 (1)

- How To Get Out Of Debt Forever! Use These Step-by-Step Tactics That Helped The Author Get Out of $6,000 In Personal Debt!Da EverandHow To Get Out Of Debt Forever! Use These Step-by-Step Tactics That Helped The Author Get Out of $6,000 In Personal Debt!Nessuna valutazione finora

- Financial Literacy GuideDocumento14 pagineFinancial Literacy GuideEllahnae VelasquezNessuna valutazione finora

- Master Your Debt: Slash Your Monthly Payments and Become Debt FreeDa EverandMaster Your Debt: Slash Your Monthly Payments and Become Debt FreeValutazione: 5 su 5 stelle5/5 (1)

- How to Increase or Build Your Credit Score in One Month: Add Over 100 Points Without The Need of Credit Repair ServicesDa EverandHow to Increase or Build Your Credit Score in One Month: Add Over 100 Points Without The Need of Credit Repair ServicesValutazione: 3 su 5 stelle3/5 (1)

- Game of LifeDocumento51 pagineGame of LifeFlaviub23Nessuna valutazione finora

- Final Borrower Defense Multistate LetterDocumento5 pagineFinal Borrower Defense Multistate LetterBethanyNessuna valutazione finora

- How To Get Rich Quick RealisticallyDocumento5 pagineHow To Get Rich Quick RealisticallyMagyari GáborNessuna valutazione finora

- Tier OneDocumento2 pagineTier OneOlivia Grace100% (1)

- Help! I Can't Pay My Bills: Surviving a Financial CrisisDa EverandHelp! I Can't Pay My Bills: Surviving a Financial CrisisNessuna valutazione finora

- 3 Secrets of MillionairesDocumento32 pagine3 Secrets of MillionairesSazu SuwNessuna valutazione finora

- EverybodysCreditRepairProgramDocumento108 pagineEverybodysCreditRepairProgramFreedomofMindNessuna valutazione finora

- Breaking Free of Financial BondageDocumento12 pagineBreaking Free of Financial BondageJesus LivesNessuna valutazione finora

- Money Letters 2 my Daughter: The letters that will make you laugh, cry and learn a whole lot about money in between!Da EverandMoney Letters 2 my Daughter: The letters that will make you laugh, cry and learn a whole lot about money in between!Valutazione: 5 su 5 stelle5/5 (1)

- The Skys The Limit Credit Repair GuideDocumento5 pagineThe Skys The Limit Credit Repair GuideCarolNessuna valutazione finora

- Retire Rich With Your Self-Directed IRA: What Your Broker & Banker Don’t Want You to Know About Managing Your Own Retirement InvestmentsDa EverandRetire Rich With Your Self-Directed IRA: What Your Broker & Banker Don’t Want You to Know About Managing Your Own Retirement InvestmentsValutazione: 2 su 5 stelle2/5 (1)

- Business Loans The Easy WayDocumento1 paginaBusiness Loans The Easy WayOjo TimmyNessuna valutazione finora

- Credit Cards Best Rewards No Annual FeeDocumento1 paginaCredit Cards Best Rewards No Annual FeeCarolNessuna valutazione finora

- Dollars and Cent$: A Parent's Guide to Raising Financially Literate KidsDa EverandDollars and Cent$: A Parent's Guide to Raising Financially Literate KidsNessuna valutazione finora

- Rescued! 401k Plan Traps Business Owners Must Avoid and FixDa EverandRescued! 401k Plan Traps Business Owners Must Avoid and FixNessuna valutazione finora

- Loopholes of The RichDocumento17 pagineLoopholes of The RichcarolinegodwinNessuna valutazione finora

- 40168collections Lawyer: The Good, The Bad, and The UglyDocumento3 pagine40168collections Lawyer: The Good, The Bad, and The UglyheldazddsnNessuna valutazione finora

- 5 Ways To Make Passive Income Online For FreeDocumento7 pagine5 Ways To Make Passive Income Online For FreeMohamed Monahed100% (1)

- GetRichSlowry - ROTH IRADocumento31 pagineGetRichSlowry - ROTH IRAThomas SpoffordNessuna valutazione finora

- Multiple Streams of IncomeDocumento9 pagineMultiple Streams of IncomeWarren BuffetNessuna valutazione finora

- HowToBuildWealth Chapter1Documento51 pagineHowToBuildWealth Chapter1Mark EsperNessuna valutazione finora

- Basic 13Documento3 pagineBasic 13Nathalie_Crist_8756Nessuna valutazione finora

- How To Make Money in Real EstateDocumento3 pagineHow To Make Money in Real Estatewise_man1975100% (1)

- State-OHIO-FINANCIAL ASSISTANCE - BUSINESS - HEALTH CARE - PET CARE CONSULTING - REAL ESTATE - HOUSING - Copy - ML EDITDocumento4 pagineState-OHIO-FINANCIAL ASSISTANCE - BUSINESS - HEALTH CARE - PET CARE CONSULTING - REAL ESTATE - HOUSING - Copy - ML EDITmcvelli40Nessuna valutazione finora

- Give Yourself CreditDocumento43 pagineGive Yourself CreditFadhel GhribiNessuna valutazione finora

- Debt Cleanse: How To Settle Your Unaffordable Debts For Pennies On The Dollar (And Not Pay Some At All)Da EverandDebt Cleanse: How To Settle Your Unaffordable Debts For Pennies On The Dollar (And Not Pay Some At All)Nessuna valutazione finora

- Money Matters: A Simple Guide To Help You Make Ends MeetDa EverandMoney Matters: A Simple Guide To Help You Make Ends MeetNessuna valutazione finora

- What Is FCRADocumento3 pagineWhat Is FCRAJorge AndrésNessuna valutazione finora

- The Ultimate Guide To Government Bidding OnlineDocumento14 pagineThe Ultimate Guide To Government Bidding OnlineAyon BaxterNessuna valutazione finora

- Build Your Human Equity Line of Credit™: The Secrets to Creating a Lifetime of Assets in Any EconomyDa EverandBuild Your Human Equity Line of Credit™: The Secrets to Creating a Lifetime of Assets in Any EconomyNessuna valutazione finora

- Taxes - The Largest Transfer of Your WealthDocumento20 pagineTaxes - The Largest Transfer of Your WealthMark Houston0% (1)

- The Credit Repair Handbook Everything You Need To Know (DR - Soc)Documento241 pagineThe Credit Repair Handbook Everything You Need To Know (DR - Soc)sssNessuna valutazione finora

- Personal Financial Stewardship: The Step-By-Step Guide to Debt-Free LivingDa EverandPersonal Financial Stewardship: The Step-By-Step Guide to Debt-Free LivingNessuna valutazione finora

- Realistic Guide to Financial Freedom Through: Investing Activity. With step-by-step guide!: How to make millions with a simple investing strategy, part 1, #1Da EverandRealistic Guide to Financial Freedom Through: Investing Activity. With step-by-step guide!: How to make millions with a simple investing strategy, part 1, #1Nessuna valutazione finora

- How To Increase Your Credit in 30 DaysDocumento2 pagineHow To Increase Your Credit in 30 Daystia1908Nessuna valutazione finora

- Credit Restoration Secrets Article 10Documento3 pagineCredit Restoration Secrets Article 10TRISTARUSA100% (1)

- Va HomeDocumento17 pagineVa Homeapi-235677343Nessuna valutazione finora

- Takeoff How To Travel The World For Next To Nothing 10xT 2Documento103 pagineTakeoff How To Travel The World For Next To Nothing 10xT 2Mike ShoeNessuna valutazione finora

- Reason Codes That Creditors Use When Denial of ApplicationsDocumento2 pagineReason Codes That Creditors Use When Denial of ApplicationsMrAlbany Will Davis100% (1)

- Ten Questions To Ask Before You Buy A HouseDocumento16 pagineTen Questions To Ask Before You Buy A HouseShubham KumarNessuna valutazione finora

- Sobal Debt Lawshool PaperDocumento60 pagineSobal Debt Lawshool PaperDavid StarkeyNessuna valutazione finora

- How To Succeed As A Note BrokerDocumento5 pagineHow To Succeed As A Note BrokerRicharnellia-RichieRichBattiest-CollinsNessuna valutazione finora

- Cheat Sheet: Penny StockDocumento2 pagineCheat Sheet: Penny StockDhrupesh955100% (1)

- How To Use Your Credit Rating To Put You On The Path To Debt FreedomDa EverandHow To Use Your Credit Rating To Put You On The Path To Debt FreedomNessuna valutazione finora

- Ne E EV Be W ChaDIT ISE Com PT IDocumento290 pagineNe E EV Be W ChaDIT ISE Com PT IRichaye100% (1)

- Financial Literacy For Women-The Money Matter FAQs-For WomenDocumento13 pagineFinancial Literacy For Women-The Money Matter FAQs-For WomenUtkarshNessuna valutazione finora

- Support MaterialsDocumento3 pagineSupport MaterialsTim JoyceNessuna valutazione finora

- Competing For The FutureDocumento9 pagineCompeting For The FutureTim JoyceNessuna valutazione finora

- Themindofstrategy PDocumento8 pagineThemindofstrategy PTim JoyceNessuna valutazione finora

- Decoding Greatness - OnlineDocumento8 pagineDecoding Greatness - OnlineTim JoyceNessuna valutazione finora

- The War of Art - Steven PressfieldDocumento12 pagineThe War of Art - Steven PressfieldTim Joyce100% (1)

- Beating The Commodity TrapDocumento9 pagineBeating The Commodity TrapTim JoyceNessuna valutazione finora

- The 4 Disciplines of ExecutionDocumento6 pagineThe 4 Disciplines of ExecutionTim JoyceNessuna valutazione finora

- RIG - Thinking in Systems Text SummaryDocumento13 pagineRIG - Thinking in Systems Text SummaryTim JoyceNessuna valutazione finora

- Being The BestDocumento9 pagineBeing The BestTim JoyceNessuna valutazione finora

- Christmas The Australian Way: OnsaleDocumento45 pagineChristmas The Australian Way: OnsaleTim JoyceNessuna valutazione finora

- Iga - Supa - Metro - 111120 - WaDocumento28 pagineIga - Supa - Metro - 111120 - WaTim JoyceNessuna valutazione finora

- Iga - NSW - Supa - V1 - 111120 - NSW LWSDocumento4 pagineIga - NSW - Supa - V1 - 111120 - NSW LWSTim JoyceNessuna valutazione finora

- SA - Foodland Catalogue 11.11.20Documento32 pagineSA - Foodland Catalogue 11.11.20Tim JoyceNessuna valutazione finora

- Ram Execution - Insights + SummaryDocumento5 pagineRam Execution - Insights + SummaryTim JoyceNessuna valutazione finora

- Zig Zag Principle SummaryDocumento6 pagineZig Zag Principle SummaryTim JoyceNessuna valutazione finora

- Shrink To Grow - WP - FINAL V8Documento16 pagineShrink To Grow - WP - FINAL V8Tim JoyceNessuna valutazione finora

- Lash Oresight: How To See The Invisible and Do The ImpossibleDocumento9 pagineLash Oresight: How To See The Invisible and Do The ImpossibleTim JoyceNessuna valutazione finora

- LivBar +marketing PlaybookDocumento38 pagineLivBar +marketing PlaybookTim JoyceNessuna valutazione finora

- Strategy - Slides 2017 Strategy Overview - Board ReportDocumento106 pagineStrategy - Slides 2017 Strategy Overview - Board ReportTim JoyceNessuna valutazione finora

- CAGNY 2019: Dirk Van de PutDocumento64 pagineCAGNY 2019: Dirk Van de PutTim JoyceNessuna valutazione finora

- CHP 7Documento32 pagineCHP 7asiflarik.mb14Nessuna valutazione finora

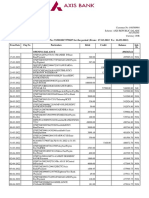

- Statement of Axis Account No:913010017379687 For The Period (From: 17-03-2022 To: 16-09-2022)Documento7 pagineStatement of Axis Account No:913010017379687 For The Period (From: 17-03-2022 To: 16-09-2022)Om Namah ShivayNessuna valutazione finora

- Treasury Management CourseDocumento10 pagineTreasury Management Coursenick21_347Nessuna valutazione finora

- Account Statement From 1 Oct 2019 To 29 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento11 pagineAccount Statement From 1 Oct 2019 To 29 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancemohammed rafiNessuna valutazione finora

- Act 2031Documento32 pagineAct 2031popbiloNessuna valutazione finora

- SMIC - Quarterly Report (Q2 2016)Documento73 pagineSMIC - Quarterly Report (Q2 2016)mikhail_flores_2Nessuna valutazione finora

- Bank of The Philippine Islands Vs The Intermediate Appellate Court and ZshornackDocumento10 pagineBank of The Philippine Islands Vs The Intermediate Appellate Court and ZshornackSheila RosetteNessuna valutazione finora

- Philippine Stock ExchangeDocumento25 paginePhilippine Stock ExchangeJessa Raga-as100% (1)

- EMV v4.2 Book 4Documento155 pagineEMV v4.2 Book 4systemcoding100% (1)

- Kadali Enviro Projects PVT - LTD: Salary CertificateDocumento2 pagineKadali Enviro Projects PVT - LTD: Salary Certificatekumar swamyNessuna valutazione finora

- 66 Restructure DebtsDocumento30 pagine66 Restructure DebtsVikas JainNessuna valutazione finora

- AAU On Tele BirrDocumento72 pagineAAU On Tele BirrNatinael AbebeNessuna valutazione finora

- NBFC Module 2 CompletedDocumento27 pagineNBFC Module 2 CompletedAneesha AkhilNessuna valutazione finora

- Application Form For CSWIP 10 Year Re-Certification (Overseas) With LogbookDocumento4 pagineApplication Form For CSWIP 10 Year Re-Certification (Overseas) With LogbookapkramjiNessuna valutazione finora

- Moneylife 2 October 2014Documento68 pagineMoneylife 2 October 2014krishnakumarsistNessuna valutazione finora

- HHDocumento6 pagineHHJoyce BusaNessuna valutazione finora

- Staff Settlement Form - NewDocumento9 pagineStaff Settlement Form - NewBaban GaigoleNessuna valutazione finora

- File CH Tila Worksheet 07Documento2 pagineFile CH Tila Worksheet 07Helpin HandNessuna valutazione finora

- Electronic Funds Transfer at PointDocumento4 pagineElectronic Funds Transfer at PointNorazila SupianNessuna valutazione finora

- Procurement of Hexagonal Drill Rod 22 M.M. Dia X 1800 M.M. Length As Per NIT Specification.Documento28 pagineProcurement of Hexagonal Drill Rod 22 M.M. Dia X 1800 M.M. Length As Per NIT Specification.sharang shankerNessuna valutazione finora

- Chandru 123Documento28 pagineChandru 123MathanNessuna valutazione finora

- Understanding Interest Options: Int NXT STMT On Armr02Documento4 pagineUnderstanding Interest Options: Int NXT STMT On Armr02Bharat SahniNessuna valutazione finora

- Total: ALE Rp.362,500 Tuna I Rp. 0Documento2 pagineTotal: ALE Rp.362,500 Tuna I Rp. 0Gilang AnggoroNessuna valutazione finora

- Chap 3 SplitDocumento54 pagineChap 3 Split22124020Nessuna valutazione finora

- VLL A17A Dec2011Documento143 pagineVLL A17A Dec2011Victor RamirezNessuna valutazione finora

- A Summer Training Project Report (Reliance Life Insurance)Documento52 pagineA Summer Training Project Report (Reliance Life Insurance)Bhatzada Zahid Jameel100% (3)

- Bank Al HabibDocumento4 pagineBank Al HabibTahir HakroNessuna valutazione finora

- Concept of Outreach in Microfinance Institutions:: Indicator of Success of MfisDocumento6 pagineConcept of Outreach in Microfinance Institutions:: Indicator of Success of MfisRiyadNessuna valutazione finora