Potrebbero piacerti anche

- Reply On PANDocumento6 pagineReply On PANPaul Casaje89% (18)

- Revenue Regulations No 12-99Documento3 pagineRevenue Regulations No 12-99Zoe Dela Cruz0% (1)

- R681s2000 Amending The Rules and Regulations Memorial Parks and CemeteriesDocumento37 pagineR681s2000 Amending The Rules and Regulations Memorial Parks and Cemeteriesacelaerden100% (2)

- PRLD - srs.002-B.00 - Sworn Registration Statement (Single)Documento2 paginePRLD - srs.002-B.00 - Sworn Registration Statement (Single)acelaerden100% (1)

- My Courses: Home BAED-FABM2112-2012S Week 10: Quarterly Exam 1st. Quarter ExamDocumento14 pagineMy Courses: Home BAED-FABM2112-2012S Week 10: Quarterly Exam 1st. Quarter Examjohn75% (8)

- NEW Contract To Sell PAG IBIGDocumento2 pagineNEW Contract To Sell PAG IBIGMj JavellanaNessuna valutazione finora

- RR 2-98 Section 2.57 (B) - CWTDocumento3 pagineRR 2-98 Section 2.57 (B) - CWTZenaida LatorreNessuna valutazione finora

- Final Tax and Creditable Withholding TaxesDocumento3 pagineFinal Tax and Creditable Withholding Taxesarrianemartinez100% (4)

- Broker and Salesperson Specimen Form (DHSUD)Documento1 paginaBroker and Salesperson Specimen Form (DHSUD)acelaerdenNessuna valutazione finora

- LUDIP RA 11396 CMO NO 11s2020Documento11 pagineLUDIP RA 11396 CMO NO 11s2020acelaerden100% (3)

- Write Here Your 6-Digit Examinee Number:: CS FORM E-6 (Revised 2005)Documento1 paginaWrite Here Your 6-Digit Examinee Number:: CS FORM E-6 (Revised 2005)acelaerden100% (1)

- Mutual Funds in IndiaDocumento83 pagineMutual Funds in Indiaswangi100% (2)

- Rossbeck 021611Documento26 pagineRossbeck 021611seehariNessuna valutazione finora

- BIR Tax Briefing - RR 11-2018Documento3 pagineBIR Tax Briefing - RR 11-2018Jeff BulasaNessuna valutazione finora

- Assessment ReturnDocumento10 pagineAssessment ReturnTriila manillaNessuna valutazione finora

- SEMINAR ON NGAsDocumento63 pagineSEMINAR ON NGAsHelen Joy Grijaldo JueleNessuna valutazione finora

- PenaltiesDocumento2 paginePenaltiesfatmaaleahNessuna valutazione finora

- BIR Form No. 2551M Percentage Tax Return Guidelines and InstructionsDocumento2 pagineBIR Form No. 2551M Percentage Tax Return Guidelines and InstructionsseanjharodNessuna valutazione finora

- Withholding Taxes: Carlo P. Divedor 19 October 2017Documento20 pagineWithholding Taxes: Carlo P. Divedor 19 October 2017Melanie Grace Ulgasan LuceroNessuna valutazione finora

- Withholding Taxes 2Documento20 pagineWithholding Taxes 2hildaNessuna valutazione finora

- Ax Reminder: When To Apply 10% or 15% EWT For Professional FeesDocumento2 pagineAx Reminder: When To Apply 10% or 15% EWT For Professional FeesRegs AccexNessuna valutazione finora

- Withholding Tax SystemDocumento8 pagineWithholding Tax Systemjeric aquipelNessuna valutazione finora

- 7.d Citibank NA vs. CA (G.R. No. 107434 October 10, 1997) - H DigestDocumento2 pagine7.d Citibank NA vs. CA (G.R. No. 107434 October 10, 1997) - H DigestHarleneNessuna valutazione finora

- Digest RR 14-2018Documento1 paginaDigest RR 14-2018Carlota Nicolas VillaromanNessuna valutazione finora

- Guidelines and Instructions For BIR Form No. 1701Q Quarterly Income Tax Return For Individuals, Estates and TrustsDocumento1 paginaGuidelines and Instructions For BIR Form No. 1701Q Quarterly Income Tax Return For Individuals, Estates and TrustsAlyssa Hallasgo-Lopez AtabeloNessuna valutazione finora

- RR No. 02-2006Documento10 pagineRR No. 02-2006odessaNessuna valutazione finora

- DRAFT RR-Implementing EOPT - For Public ConsultationDocumento4 pagineDRAFT RR-Implementing EOPT - For Public ConsultationGennelyn OdulioNessuna valutazione finora

- Tax AdministrationDocumento5 pagineTax AdministrationAbdullahi AbdikadirNessuna valutazione finora

- TAX-CPAR Lecture Filing and Penalties Version 2Documento23 pagineTAX-CPAR Lecture Filing and Penalties Version 2YamateNessuna valutazione finora

- 1701 Guide Nov 2011Documento1 pagina1701 Guide Nov 2011Cy YolipseNessuna valutazione finora

- SET 23 24 Detail Guide EDocumento20 pagineSET 23 24 Detail Guide ENishan MahanamaNessuna valutazione finora

- Returns and Payment of TaxDocumento12 pagineReturns and Payment of TaxHelaena Bueno Delos SantosNessuna valutazione finora

- Obligations: 1. RegistrationDocumento5 pagineObligations: 1. RegistrationPhilip AlamboNessuna valutazione finora

- Item No. 1 - Taxable Period: 1. Purely Compensation Income Earner BIR Annual Income Tax Return (ITR) Form No. 1700Documento48 pagineItem No. 1 - Taxable Period: 1. Purely Compensation Income Earner BIR Annual Income Tax Return (ITR) Form No. 1700Miguel CasimNessuna valutazione finora

- CPAR Filing, Penalties, and Remedies (Batch 89) HandoutDocumento25 pagineCPAR Filing, Penalties, and Remedies (Batch 89) HandoutlllllNessuna valutazione finora

- Electronic Liability Register: TAX Deducted at SourceDocumento10 pagineElectronic Liability Register: TAX Deducted at Sourcejoeljose2019jjNessuna valutazione finora

- RMC No. 135-2019 - Digest PDFDocumento2 pagineRMC No. 135-2019 - Digest PDFAMNessuna valutazione finora

- TDS On Salaries - Income Tax Department, INDIADocumento112 pagineTDS On Salaries - Income Tax Department, INDIAArnav MendirattaNessuna valutazione finora

- RR 3-02Documento6 pagineRR 3-02matinikkiNessuna valutazione finora

- 1601 C CompensationDocumento2 pagine1601 C Compensationjon_cpaNessuna valutazione finora

- Tax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeDocumento7 pagineTax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeJouhara ObeñitaNessuna valutazione finora

- 1601C GuidelinesDocumento1 pagina1601C GuidelinesAnonymous 1tTxK4Nessuna valutazione finora

- W3 Module 3 - Tax Administration Part IIDocumento14 pagineW3 Module 3 - Tax Administration Part IIElmeerajh JudavarNessuna valutazione finora

- Sei - ItrDocumento36 pagineSei - ItrMiguel CasimNessuna valutazione finora

- Chapter 4 - Co-Ownership, Estates and TrustsDocumento8 pagineChapter 4 - Co-Ownership, Estates and TrustsLiRose SmithNessuna valutazione finora

- Taxation 1 Lesson 1. Returns and Payment of TaxDocumento42 pagineTaxation 1 Lesson 1. Returns and Payment of TaxHarui Hani-31Nessuna valutazione finora

- Income Tax 2017 Edazdb1013Documento50 pagineIncome Tax 2017 Edazdb1013Pradeep PatilNessuna valutazione finora

- ACCOUNTING TaxDocumento12 pagineACCOUNTING TaxMark Joseph BajaNessuna valutazione finora

- Tax 1.1Documento13 pagineTax 1.1Mheryza De Castro PabustanNessuna valutazione finora

- 1601e PDFDocumento2 pagine1601e PDFJanKhyrelFloresNessuna valutazione finora

- RR 12-01Documento6 pagineRR 12-01matinikkiNessuna valutazione finora

- Presentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Documento44 paginePresentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Franco DurantNessuna valutazione finora

- Section 2.57.4 of RR No. 2-98Documento2 pagineSection 2.57.4 of RR No. 2-98fatmaaleahNessuna valutazione finora

- Tds Law and Practice: Under Income Tax Act, 1961Documento84 pagineTds Law and Practice: Under Income Tax Act, 1961Vaibhav ChauhanNessuna valutazione finora

- Bir RR 12-99Documento21 pagineBir RR 12-99Isaac Joshua AganonNessuna valutazione finora

- CPAR Lecture Filing and Penalties (Batch 90) HandoutDocumento25 pagineCPAR Lecture Filing and Penalties (Batch 90) HandoutAljur SalamedaNessuna valutazione finora

- Restriction Imposed On Revising Wealth StatementDocumento9 pagineRestriction Imposed On Revising Wealth StatementAbid BashirNessuna valutazione finora

- 1700 Guide Nov 2011Documento1 pagina1700 Guide Nov 2011Danilo Dela ReaNessuna valutazione finora

- RMC No 16-2013Documento3 pagineRMC No 16-2013Eric DykimchingNessuna valutazione finora

- LifeBlood - Assessment Process Tax 2Documento17 pagineLifeBlood - Assessment Process Tax 2Monjid AbpiNessuna valutazione finora

- TDS On SalariesDocumento112 pagineTDS On Salariesbaalaji05Nessuna valutazione finora

- Mixed Income - ITRDocumento71 pagineMixed Income - ITRMiguel CasimNessuna valutazione finora

- BIR Form 1601 c1Documento2 pagineBIR Form 1601 c1Ver ArocenaNessuna valutazione finora

- Bir Form No. 2304Documento2 pagineBir Form No. 2304mijareschabelita2Nessuna valutazione finora

- Atlas Consolidated Mining vs. CIRDocumento51 pagineAtlas Consolidated Mining vs. CIRCamille Yasmeen SamsonNessuna valutazione finora

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeDa Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeValutazione: 1 su 5 stelle1/5 (1)

- 1040 Exam Prep: Module II - Basic Tax ConceptsDa Everand1040 Exam Prep: Module II - Basic Tax ConceptsValutazione: 1.5 su 5 stelle1.5/5 (2)

- 1040 Exam Prep: Module I: The Form 1040 FormulaDa Everand1040 Exam Prep: Module I: The Form 1040 FormulaValutazione: 1 su 5 stelle1/5 (3)

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsDa Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsNessuna valutazione finora

- MC 93 06Documento19 pagineMC 93 06acelaerdenNessuna valutazione finora

- Department Order No.2021-010Documento4 pagineDepartment Order No.2021-010acelaerdenNessuna valutazione finora

- MC 15 01Documento16 pagineMC 15 01acelaerdenNessuna valutazione finora

- Special Order No. 2022-073Documento23 pagineSpecial Order No. 2022-073acelaerdenNessuna valutazione finora

- Department Order No.2021-011Documento2 pagineDepartment Order No.2021-011acelaerdenNessuna valutazione finora

- Department Order No.2021-013Documento1 paginaDepartment Order No.2021-013acelaerdenNessuna valutazione finora

- Salesperson's Letter of EngagementDocumento1 paginaSalesperson's Letter of Engagementacelaerden67% (3)

- Local Weather Forecast (PM) - Northern Luzon PAGASA Regional Services Division (18 September 21, Saturday)Documento5 pagineLocal Weather Forecast (PM) - Northern Luzon PAGASA Regional Services Division (18 September 21, Saturday)acelaerdenNessuna valutazione finora

- DHSUD Region 3 Salesperson's Registration Form 2021Documento1 paginaDHSUD Region 3 Salesperson's Registration Form 2021acelaerdenNessuna valutazione finora

- DHSUD Region 3 Broker's Registration Form 2021Documento1 paginaDHSUD Region 3 Broker's Registration Form 2021acelaerdenNessuna valutazione finora

- RDRRMC 3 Memo No 47 S 2021 - NDRM 2021 Opening Ceremony 01 July 2021Documento1 paginaRDRRMC 3 Memo No 47 S 2021 - NDRM 2021 Opening Ceremony 01 July 2021acelaerdenNessuna valutazione finora

- Ibpa Mi Bapu Marya Ligaya QNG IbpaDocumento2 pagineIbpa Mi Bapu Marya Ligaya QNG Ibpaacelaerden100% (1)

- MC-18-09 (Guidelines For The Revised IRR of R.A. 7279 As Amended by R.A. 10884Documento36 pagineMC-18-09 (Guidelines For The Revised IRR of R.A. 7279 As Amended by R.A. 10884acelaerden100% (2)

- Hlurb BR 957 s2017Documento3 pagineHlurb BR 957 s2017acelaerdenNessuna valutazione finora

- PRLD - fs.006-b.00 - Sir - Fact Sheet (Condo)Documento2 paginePRLD - fs.006-b.00 - Sir - Fact Sheet (Condo)acelaerdenNessuna valutazione finora

- CSFP Bir 2017 PDFDocumento22 pagineCSFP Bir 2017 PDFacelaerdenNessuna valutazione finora

- Dam Dam SiteDocumento11 pagineDam Dam SiteacelaerdenNessuna valutazione finora

- Hoa A 0003Documento7 pagineHoa A 0003acelaerdenNessuna valutazione finora

- Aliaswoe Fortus Vs HomesteadDocumento6 pagineAliaswoe Fortus Vs HomesteadacelaerdenNessuna valutazione finora

- Financial Accounting and Reporting NotesDocumento6 pagineFinancial Accounting and Reporting NotesDarlene SarcinoNessuna valutazione finora

- 8 Responsibility Accounting Transfer Price and Balance ScorecardDocumento9 pagine8 Responsibility Accounting Transfer Price and Balance ScorecardAlliah Mae ArbastoNessuna valutazione finora

- Grade 09 Paper 2 Mid-Term ExaminationDocumento7 pagineGrade 09 Paper 2 Mid-Term ExaminationSarrah ShabbirNessuna valutazione finora

- Group 3 - Bandhan BankDocumento16 pagineGroup 3 - Bandhan BankAnisha KhandelwalNessuna valutazione finora

- Grade 10 Provincial Exam Accounting (English) Answer Book - 050312Documento10 pagineGrade 10 Provincial Exam Accounting (English) Answer Book - 050312hobyanevisionNessuna valutazione finora

- Bajaj Finance Ltd. (India) : SourceDocumento2 pagineBajaj Finance Ltd. (India) : SourceDivyagarapatiNessuna valutazione finora

- 05 Subhash May-17 PDFDocumento1 pagina05 Subhash May-17 PDFCma Subhash AtipamulaNessuna valutazione finora

- Macroeconomics & National IncomeDocumento20 pagineMacroeconomics & National Incomesd0324Nessuna valutazione finora

- Auditors ReportDocumento2 pagineAuditors ReportUpendra KesarwaniNessuna valutazione finora

- Cma ArttDocumento427 pagineCma ArttMUHAMMAD ALINessuna valutazione finora

- Account Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento6 pagineAccount Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceKumar SunilNessuna valutazione finora

- AbstractDocumento2 pagineAbstractSakub Amin Sick'L'Nessuna valutazione finora

- Castle ComplaintDocumento40 pagineCastle ComplaintThe Denver PostNessuna valutazione finora

- Shantanu Raj: Seeking Middle Level Assignments in ANY Sector With An Organization of High ReputeDocumento2 pagineShantanu Raj: Seeking Middle Level Assignments in ANY Sector With An Organization of High ReputeSushama VermaNessuna valutazione finora

- Getting Started With GST Unit 2 8 Mark QuestionsDocumento2 pagineGetting Started With GST Unit 2 8 Mark Questionsmanoharchary157Nessuna valutazione finora

- Public-Private Partnership: South Lake Union Streetcar, Seattle, WADocumento13 paginePublic-Private Partnership: South Lake Union Streetcar, Seattle, WAMatthew SteenhoekNessuna valutazione finora

- Ecf 320 - Money, Banking and Financial MarketsDocumento22 pagineEcf 320 - Money, Banking and Financial MarketsFredrich KztizNessuna valutazione finora

- The Impact of Sustainability (Environmental, Social, and Governance) Disclosure and Board Diversity On Firm Value - The Moderating Role of Industry SensitivityDocumento16 pagineThe Impact of Sustainability (Environmental, Social, and Governance) Disclosure and Board Diversity On Firm Value - The Moderating Role of Industry SensitivityHENI YUSNITANessuna valutazione finora

- Your Quarterly Statement: Statement Date: From Date: To DateDocumento3 pagineYour Quarterly Statement: Statement Date: From Date: To DateMalik JawadNessuna valutazione finora

- 14 Quiz and Discussion Version2011 01Documento18 pagine14 Quiz and Discussion Version2011 01andrijamikulicNessuna valutazione finora

- Chapter 1 Introduction To Corporate Finance 2Documento4 pagineChapter 1 Introduction To Corporate Finance 2Mrittika SahaNessuna valutazione finora

- Community TaxDocumento3 pagineCommunity TaxSuzette VillalinoNessuna valutazione finora

- #Pvofguaranteedpaymentof10,000In5Years: PV PVDocumento7 pagine#Pvofguaranteedpaymentof10,000In5Years: PV PVL.E.O.ZNessuna valutazione finora

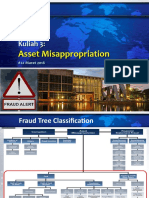

- Asset MisappropriationDocumento15 pagineAsset MisappropriationKelas 7-02 D-IV AKTNessuna valutazione finora

- APR-2015 Bvf6aDocumento4 pagineAPR-2015 Bvf6aSuresh KumarNessuna valutazione finora

- Internship Report Veena - Copy of VeenaDocumento32 pagineInternship Report Veena - Copy of VeenaBhuvan MhNessuna valutazione finora