Potrebbero piacerti anche

- Enterprise TechDocumento4 pagineEnterprise TechNatalie Daguiam100% (2)

- AFAR ProblemsDocumento45 pagineAFAR ProblemsElena Llasos84% (31)

- Format Sopl and SofpDocumento3 pagineFormat Sopl and SofpMuhammad Faaiz IzzeawanNessuna valutazione finora

- Sharecropping Simulation ActivityDocumento5 pagineSharecropping Simulation Activityapi-282568260100% (1)

- Earn $1,100 Per Week Through Risk Free Arbitrage BettingDocumento19 pagineEarn $1,100 Per Week Through Risk Free Arbitrage Bettingsnpatel171100% (1)

- Business Combi and Conso HandoutDocumento16 pagineBusiness Combi and Conso HandoutKarlo Jude Acidera100% (2)

- Preparation of Financial Statement For A Sole TraderDocumento8 paginePreparation of Financial Statement For A Sole TraderDebbie DebzNessuna valutazione finora

- Past CPA Board On MASDocumento22 paginePast CPA Board On MASJaime Gomez Sto TomasNessuna valutazione finora

- Buying and SellingDocumento19 pagineBuying and SellingNeri SangalangNessuna valutazione finora

- Revision Questions - CH 17 - QuestionsDocumento3 pagineRevision Questions - CH 17 - QuestionsMinh ThưNessuna valutazione finora

- Installment Sales Methods in Gross Profit (GP) RecognitionDocumento3 pagineInstallment Sales Methods in Gross Profit (GP) RecognitionLeny Lyn AnihayNessuna valutazione finora

- Revenue RecognitionDocumento8 pagineRevenue RecognitionSedrick ChiongNessuna valutazione finora

- Sba ComputationsDocumento1 paginaSba ComputationsAbdul Jamal NassirNessuna valutazione finora

- Inventories - : Methods For Inventory WritedownDocumento5 pagineInventories - : Methods For Inventory WritedownBryan NatadNessuna valutazione finora

- Installment SalesDocumento5 pagineInstallment SalesBryan ReyesNessuna valutazione finora

- Far 6815 - Gross Profit Method Far 6816 - Retail Inventory MethodDocumento2 pagineFar 6815 - Gross Profit Method Far 6816 - Retail Inventory MethodKent Raysil PamaongNessuna valutazione finora

- Transfer and Business Taxation Accounting Methods and PeriodsDocumento5 pagineTransfer and Business Taxation Accounting Methods and PeriodsApril Joy Padua SimonNessuna valutazione finora

- Direct Financing & Sales Type LeaseDocumento1 paginaDirect Financing & Sales Type LeaseKent Raysil PamaongNessuna valutazione finora

- Normal Gross Profit Cost To Sell (Ex: Commission) Reconditioning CostDocumento1 paginaNormal Gross Profit Cost To Sell (Ex: Commission) Reconditioning CostddddddaaaaeeeeNessuna valutazione finora

- FormulasDocumento5 pagineFormulasKezNessuna valutazione finora

- Format SoplDocumento2 pagineFormat Soplhumairayazid12Nessuna valutazione finora

- Consolidated statement of comprehensive incomeDocumento11 pagineConsolidated statement of comprehensive incomeAli OptimisticNessuna valutazione finora

- Consolidation Summary P&LDocumento3 pagineConsolidation Summary P&LRah EelNessuna valutazione finora

- ACTBFAR Pro-Forma Statements - Accounting For Manufacturing-1Documento5 pagineACTBFAR Pro-Forma Statements - Accounting For Manufacturing-1Gabrielle Brianna ChuaNessuna valutazione finora

- 13 Consolidated Financial StatementDocumento5 pagine13 Consolidated Financial StatementabcdefgNessuna valutazione finora

- ACCOUNTINGDocumento2 pagineACCOUNTINGMarie OrbetaNessuna valutazione finora

- AFAR FORMULAS EXPLAINEDDocumento53 pagineAFAR FORMULAS EXPLAINEDEmma Mariz GarciaNessuna valutazione finora

- Consolidated Financial FormulasDocumento3 pagineConsolidated Financial FormulasNiña Rica PunzalanNessuna valutazione finora

- Ind As 2: Inventories: (I) MeaningDocumento6 pagineInd As 2: Inventories: (I) MeaningDinesh KumarNessuna valutazione finora

- Summary of EliminationsDocumento7 pagineSummary of EliminationsSella DestikaNessuna valutazione finora

- Statement of Financial Position: AssetsDocumento3 pagineStatement of Financial Position: AssetsMary Quezia AlferezNessuna valutazione finora

- Consolidated Financial Statement ExerciseDocumento4 pagineConsolidated Financial Statement ExerciseAnonymous OzWtUONessuna valutazione finora

- Chapter 7Documento15 pagineChapter 7msukri_81Nessuna valutazione finora

- State of Owners EquityDocumento1 paginaState of Owners EquitylancealcarazNessuna valutazione finora

- Purchase of Inventories Purchase of Welfare Goods: Inventory Held For Sale Inventory Held For DistributionDocumento3 paginePurchase of Inventories Purchase of Welfare Goods: Inventory Held For Sale Inventory Held For DistributionNicole AutrizNessuna valutazione finora

- ACYAVA 2 Formula SheetDocumento13 pagineACYAVA 2 Formula SheetN SNessuna valutazione finora

- Vertical Income Statement TemplateDocumento2 pagineVertical Income Statement TemplateForam VasaniNessuna valutazione finora

- Secondary Book of Account: Prof. S. Y. ShewaleDocumento10 pagineSecondary Book of Account: Prof. S. Y. Shewalesneharsh2370Nessuna valutazione finora

- Far 06-04 Ias 2 Inventory PDFDocumento9 pagineFar 06-04 Ias 2 Inventory PDFZee MarvsNessuna valutazione finora

- Actg101 Fs Prepa TemplateDocumento16 pagineActg101 Fs Prepa TemplateJaira ClavoNessuna valutazione finora

- Intercompany Fixed AssetsDocumento5 pagineIntercompany Fixed Assetstungoldonette3Nessuna valutazione finora

- Chapter 3 - Statement of Comprehensive IncomeDocumento7 pagineChapter 3 - Statement of Comprehensive IncomeKarylle EntinoNessuna valutazione finora

- FARAP-4403 (Inventories)Documento14 pagineFARAP-4403 (Inventories)Dizon Ropalito P.Nessuna valutazione finora

- Income Statement FormatDocumento3 pagineIncome Statement FormatMohammad Samsul ArefinNessuna valutazione finora

- InstallmentDocumento2 pagineInstallmentguliramsam5Nessuna valutazione finora

- HO Inventory-EstimationDocumento1 paginaHO Inventory-EstimationAl Francis GuillermoNessuna valutazione finora

- Ap 34PW2-2 PDFDocumento1 paginaAp 34PW2-2 PDFRyan PelitoNessuna valutazione finora

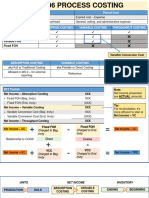

- MS 06-06 Process CostingDocumento6 pagineMS 06-06 Process CostingxernathanNessuna valutazione finora

- CFR ProblemsDocumento28 pagineCFR ProblemsMadhu kumarNessuna valutazione finora

- Summary Notes With AS Charts by CS Rohan Nimbalkar - Account - StepFly YJYB160521Documento82 pagineSummary Notes With AS Charts by CS Rohan Nimbalkar - Account - StepFly YJYB160521Deep MehtaNessuna valutazione finora

- FR Shield - Ind As 2 - InventoriesDocumento4 pagineFR Shield - Ind As 2 - InventoriesTanvi jain100% (1)

- Chap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)Documento18 pagineChap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)7a4374 hisNessuna valutazione finora

- Final Accounts of SoletradersDocumento9 pagineFinal Accounts of SoletradersShanavaz AsokachalilNessuna valutazione finora

- Income Statement and Balance SheetDocumento20 pagineIncome Statement and Balance Sheetpankaj tiwariNessuna valutazione finora

- IAS 36 - ImpairmentDocumento2 pagineIAS 36 - ImpairmentDawar Hussain (WT)Nessuna valutazione finora

- Cost Accounting: Step 1: Determine The Highest and Lowest Activity and The Costs Associated ThereuntoDocumento8 pagineCost Accounting: Step 1: Determine The Highest and Lowest Activity and The Costs Associated ThereuntoRinoah Mae OlorosoNessuna valutazione finora

- Cash Flow Statement AnalysisDocumento3 pagineCash Flow Statement AnalysisSukumarVenkataNessuna valutazione finora

- Investment Decisions NotesDocumento2 pagineInvestment Decisions NotesSaumya AllapartiNessuna valutazione finora

- Audit Inventory ProceduresDocumento57 pagineAudit Inventory Proceduressethdrea officialNessuna valutazione finora

- Merchandising BusinessDocumento9 pagineMerchandising BusinessSean Justin EspinaNessuna valutazione finora

- Mutiara Enterprise Statement of Profit or Loss For The Year Ended 31 December 2019Documento3 pagineMutiara Enterprise Statement of Profit or Loss For The Year Ended 31 December 2019Zafran100% (1)

- Chap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)Documento17 pagineChap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)7a4374 hisNessuna valutazione finora

- Chapter 10-14: Key Accounting Concepts for Inventories and Cost Flow MethodsDocumento5 pagineChapter 10-14: Key Accounting Concepts for Inventories and Cost Flow MethodsNichola aasNessuna valutazione finora

- Basic Income StatementsDocumento2 pagineBasic Income StatementsTanjim BhuiyanNessuna valutazione finora

- Equity Method Proforma EntriesDocumento13 pagineEquity Method Proforma EntriesMichael ArevaloNessuna valutazione finora

- Physics PDFDocumento1 paginaPhysics PDFShaira BugayongNessuna valutazione finora

- Grade 10 First Am BotDocumento14 pagineGrade 10 First Am BotShaira BugayongNessuna valutazione finora

- After TwoDocumento2 pagineAfter TwoShaira BugayongNessuna valutazione finora

- Taxation Material 2Documento7 pagineTaxation Material 2Shaira BugayongNessuna valutazione finora

- Radio Wave Infrared Wave Visible Light Ultraviolet Rays X-Ray Wave Gamma Wave Wavelength FrequencyDocumento1 paginaRadio Wave Infrared Wave Visible Light Ultraviolet Rays X-Ray Wave Gamma Wave Wavelength FrequencyShaira BugayongNessuna valutazione finora

- Table NormalizationDocumento1 paginaTable NormalizationShaira BugayongNessuna valutazione finora

- 4 TH Grading IPDocumento17 pagine4 TH Grading IPShaira BugayongNessuna valutazione finora

- Grade 10 First Am BotDocumento14 pagineGrade 10 First Am BotShaira BugayongNessuna valutazione finora

- Grade10FirstAmbot 1Documento15 pagineGrade10FirstAmbot 1Shaira BugayongNessuna valutazione finora

- ) Was TreatedDocumento3 pagine) Was TreatedShaira BugayongNessuna valutazione finora

- Taxation Material 3Documento11 pagineTaxation Material 3Shaira BugayongNessuna valutazione finora

- Philippine Taxation Questions GuideDocumento36 paginePhilippine Taxation Questions GuideShaira BugayongNessuna valutazione finora

- Central Mindanao University: Cmu Laboratory High SchoolDocumento1 paginaCentral Mindanao University: Cmu Laboratory High SchoolShaira BugayongNessuna valutazione finora

- Taxation Material 1Documento11 pagineTaxation Material 1Shaira Bugayong100% (1)

- Bioplastic Organic Plastic Test 1 6 23 Test 2 4 8 Test 3 3 18 Average 4.33 N 15.33 NDocumento3 pagineBioplastic Organic Plastic Test 1 6 23 Test 2 4 8 Test 3 3 18 Average 4.33 N 15.33 NShaira BugayongNessuna valutazione finora

- Negotiable Instruments LawDocumento2 pagineNegotiable Instruments LawShang BugayongNessuna valutazione finora

- RRLDocumento9 pagineRRLShaira BugayongNessuna valutazione finora

- Manage Appointments and Patient RecordsDocumento2 pagineManage Appointments and Patient RecordsShaira BugayongNessuna valutazione finora

- Grade 10 First Am BotDocumento14 pagineGrade 10 First Am BotShaira BugayongNessuna valutazione finora

- 4 TH Grading IPDocumento17 pagine4 TH Grading IPShaira BugayongNessuna valutazione finora

- APCAS 10 11 Phil Ctry ReportDocumento24 pagineAPCAS 10 11 Phil Ctry ReportBilly Julius GestiadaNessuna valutazione finora

- Statement of Financial Position ClassificationDocumento1 paginaStatement of Financial Position ClassificationShaira BugayongNessuna valutazione finora

- ) Was TreatedDocumento3 pagine) Was TreatedShaira BugayongNessuna valutazione finora

- Tariff and Customs Code-AnswerDocumento10 pagineTariff and Customs Code-AnswerShaira BugayongNessuna valutazione finora

- 2009-09-19 061224 UpselwDocumento1 pagina2009-09-19 061224 UpselwMArk Dino AlbielaNessuna valutazione finora

- Sec11 23Documento1 paginaSec11 23Shaira BugayongNessuna valutazione finora

- Summary of Important EquationsDocumento7 pagineSummary of Important EquationsShaira Bugayong100% (1)

- Supplier Contact NO. Email Address Address 1. B-Meg: Davao OfficeDocumento2 pagineSupplier Contact NO. Email Address Address 1. B-Meg: Davao OfficeShang BugayongNessuna valutazione finora

- Rice Mill Detailed Project Report - 9t Per Hour - For Finance, Subsidy & Project Related Support Contact - 9861458008Documento49 pagineRice Mill Detailed Project Report - 9t Per Hour - For Finance, Subsidy & Project Related Support Contact - 9861458008Radha Krishna SahooNessuna valutazione finora

- Case - Costing in Pepe Denim PDFDocumento5 pagineCase - Costing in Pepe Denim PDFMadhur AggarwalNessuna valutazione finora

- Becker f6Documento71 pagineBecker f6Safa RoxNessuna valutazione finora

- Capital and Return On CapitalDocumento38 pagineCapital and Return On CapitalThái NguyễnNessuna valutazione finora

- The Impacts of Unemployment in Zimbabwe From The 2009-2019Documento12 pagineThe Impacts of Unemployment in Zimbabwe From The 2009-2019Tracy AlpsNessuna valutazione finora

- Chapter 22 Fiscal Policy and Monetary PolicyDocumento68 pagineChapter 22 Fiscal Policy and Monetary PolicyJason ChungNessuna valutazione finora

- Part 1 - Section D Cost Management 1.1 Cost Drivers and Cost FlowsDocumento114 paginePart 1 - Section D Cost Management 1.1 Cost Drivers and Cost FlowsGaleli PascualNessuna valutazione finora

- ClubbingDocumento18 pagineClubbingSamyak JirawalaNessuna valutazione finora

- Susquehanna Equipment Rentals-New DataDocumento14 pagineSusquehanna Equipment Rentals-New Datalaale dijaanNessuna valutazione finora

- All About Inflation: Club of Economics and Finance IIT (BHU), VaranasiDocumento16 pagineAll About Inflation: Club of Economics and Finance IIT (BHU), VaranasiShashank_PardhikarNessuna valutazione finora

- Trade and Capital Flows - GCC and India - Final - May 02 2012Documento55 pagineTrade and Capital Flows - GCC and India - Final - May 02 2012aakashblueNessuna valutazione finora

- 350exi-Q22659 00Documento24 pagine350exi-Q22659 00Jack YangNessuna valutazione finora

- Atul Auto LTD.: Ratio & Company AnalysisDocumento7 pagineAtul Auto LTD.: Ratio & Company AnalysisMohit KanjwaniNessuna valutazione finora

- Accountancy Sample Paper Class 11 PDFDocumento6 pagineAccountancy Sample Paper Class 11 PDFAnkit JhaNessuna valutazione finora

- Tax Treatment of Dividend Received From CompanyDocumento10 pagineTax Treatment of Dividend Received From CompanymukeshNessuna valutazione finora

- Resume Ch.11 Consolidation TheoriesDocumento3 pagineResume Ch.11 Consolidation TheoriesDwiki TegarNessuna valutazione finora

- Pages From Filed ComplaintDocumento9 paginePages From Filed Complaintmbamman-1Nessuna valutazione finora

- Data Market Inquiry SummaryDocumento24 pagineData Market Inquiry SummaryJanice Healing100% (4)

- Total Care Foundation by LawsDocumento6 pagineTotal Care Foundation by LawstotalcareinternationalNessuna valutazione finora

- SSI Feasibility Study SampleDocumento116 pagineSSI Feasibility Study SampleAJi AdilNessuna valutazione finora

- Adjusting Entries for Sharon Matthews ConsultingDocumento8 pagineAdjusting Entries for Sharon Matthews ConsultingUrBaN-xGaMeRx TriicKShOtZNessuna valutazione finora

- Murphy v. Commissioner of IRS, 469 F.3d 27, 1st Cir. (2006)Documento7 pagineMurphy v. Commissioner of IRS, 469 F.3d 27, 1st Cir. (2006)Scribd Government DocsNessuna valutazione finora

- Optimize General Ledger TitleDocumento1 paginaOptimize General Ledger TitleMinn TunNessuna valutazione finora

- Brief Analysis of The Revised Fifth Schedule To The CompaniesDocumento11 pagineBrief Analysis of The Revised Fifth Schedule To The Companieszulfi100% (1)

- Report Audit PT Greenwood Sejahtera TBK 2020Documento100 pagineReport Audit PT Greenwood Sejahtera TBK 2020NYansyahNessuna valutazione finora