Potrebbero piacerti anche

- RMC 48-90Documento2 pagineRMC 48-90cmv mendozaNessuna valutazione finora

- University of The Philippines College of LawDocumento2 pagineUniversity of The Philippines College of LawSophiaFrancescaEspinosaNessuna valutazione finora

- Florentina L. Baclayon, vs. Judge Mutia: Relevant FactsDocumento2 pagineFlorentina L. Baclayon, vs. Judge Mutia: Relevant FactsSophiaFrancescaEspinosaNessuna valutazione finora

- University of The Philippines College of Law: SpecificationDocumento3 pagineUniversity of The Philippines College of Law: SpecificationSophiaFrancescaEspinosaNessuna valutazione finora

- Pan v. PenaDocumento2 paginePan v. PenaSophiaFrancescaEspinosaNessuna valutazione finora

- People V TolentinoDocumento2 paginePeople V TolentinoSophiaFrancescaEspinosaNessuna valutazione finora

- University of The Philippines College of LawDocumento2 pagineUniversity of The Philippines College of LawSophiaFrancescaEspinosaNessuna valutazione finora

- University of The Philippines College of Law: Us, V. Catalino ApostolDocumento2 pagineUniversity of The Philippines College of Law: Us, V. Catalino ApostolSophiaFrancescaEspinosa100% (1)

- University of The Philippines College of Law: Lito Corpuz, vs. PeopleDocumento5 pagineUniversity of The Philippines College of Law: Lito Corpuz, vs. PeopleSophiaFrancescaEspinosaNessuna valutazione finora

- University of The Philippines College of Law: RelevantDocumento3 pagineUniversity of The Philippines College of Law: RelevantSophiaFrancescaEspinosaNessuna valutazione finora

- People v. SanidadDocumento3 paginePeople v. SanidadSophiaFrancescaEspinosaNessuna valutazione finora

- University of The Philippines College of Law: Melencio Gigantoni Y Javier, vs. People and IacDocumento2 pagineUniversity of The Philippines College of Law: Melencio Gigantoni Y Javier, vs. People and IacSophiaFrancescaEspinosaNessuna valutazione finora

- BLTB v. BitangaDocumento2 pagineBLTB v. BitangaSophiaFrancescaEspinosaNessuna valutazione finora

- Clemente v. CADocumento2 pagineClemente v. CASophiaFrancescaEspinosaNessuna valutazione finora

- University of The Philippines College of LawDocumento3 pagineUniversity of The Philippines College of LawSophiaFrancescaEspinosaNessuna valutazione finora

- XDocumento2 pagineXSophiaFrancescaEspinosaNessuna valutazione finora

- 14 Lecaroz V SandiganbayanDocumento3 pagine14 Lecaroz V SandiganbayanSophiaFrancescaEspinosaNessuna valutazione finora

- Associated Bank, vs. Ca and Lorenzo Sarmiento JRDocumento4 pagineAssociated Bank, vs. Ca and Lorenzo Sarmiento JRSophiaFrancescaEspinosaNessuna valutazione finora

- SDocumento3 pagineSSophiaFrancescaEspinosaNessuna valutazione finora

- Associated Bank v. CADocumento2 pagineAssociated Bank v. CASha SantosNessuna valutazione finora

- Agilent v. IntegratedDocumento2 pagineAgilent v. IntegratedSophiaFrancescaEspinosaNessuna valutazione finora

- Dee Ping Wee v. Lee Hiong WeeDocumento3 pagineDee Ping Wee v. Lee Hiong WeeSophiaFrancescaEspinosa100% (1)

- Chua v. CADocumento2 pagineChua v. CASophiaFrancescaEspinosaNessuna valutazione finora

- XDocumento7 pagineXSophiaFrancescaEspinosaNessuna valutazione finora

- XDocumento2 pagineXSophiaFrancescaEspinosaNessuna valutazione finora

- XDocumento4 pagineXSophiaFrancescaEspinosaNessuna valutazione finora

- XDocumento2 pagineXSophiaFrancescaEspinosaNessuna valutazione finora

- XDocumento2 pagineXSophiaFrancescaEspinosaNessuna valutazione finora

- XDocumento3 pagineXSophiaFrancescaEspinosaNessuna valutazione finora

- XDocumento2 pagineXSophiaFrancescaEspinosaNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Module 6 Applied EcoDocumento12 pagineModule 6 Applied EcoKrista SuyatNessuna valutazione finora

- NFJPIA Online Preboard Exam Tax UnformattedDocumento22 pagineNFJPIA Online Preboard Exam Tax UnformattedYietNessuna valutazione finora

- 1 - RFP For AML Screening Tool FinalDocumento71 pagine1 - RFP For AML Screening Tool FinalccmehtaNessuna valutazione finora

- File 6530ce398b6c4 2024 2026 MTEF&FSP Transmittal Draft FinalDocumento85 pagineFile 6530ce398b6c4 2024 2026 MTEF&FSP Transmittal Draft FinalMayowa DurosinmiNessuna valutazione finora

- Taxation of Cooperatives and Other CorporatesDocumento8 pagineTaxation of Cooperatives and Other CorporatesTriila manillaNessuna valutazione finora

- Financial Terminology Definition of The Financial TermDocumento36 pagineFinancial Terminology Definition of The Financial TermRajeev TripathiNessuna valutazione finora

- The PILOT - June 2018Documento20 pagineThe PILOT - June 2018Redwood Shores Community AssociationNessuna valutazione finora

- Intermediate Accounting 2 ReviewDocumento27 pagineIntermediate Accounting 2 ReviewcpacpacpaNessuna valutazione finora

- Canadian Labour Market Second EditionDocumento371 pagineCanadian Labour Market Second Editionojasdatt86% (7)

- Applied Indirect TaxationDocumento23 pagineApplied Indirect TaxationMehak KaushikkNessuna valutazione finora

- Taxation in India Vs AfghanistanDocumento11 pagineTaxation in India Vs AfghanistanKomal AgrawalNessuna valutazione finora

- Please Note: Fields Marked With: (Red Asterisk) Are Mandatory Fields and Need To Be Filled UpDocumento20 paginePlease Note: Fields Marked With: (Red Asterisk) Are Mandatory Fields and Need To Be Filled UpHinglaj SinghNessuna valutazione finora

- Excise Announcements For 2023-24 - Final08032023153431Documento124 pagineExcise Announcements For 2023-24 - Final08032023153431jio comNessuna valutazione finora

- Employee's Withholding Exemption and County Status CertificateDocumento2 pagineEmployee's Withholding Exemption and County Status CertificateAparajeeta GuhaNessuna valutazione finora

- IELTS Band 9 Grammar SecretsDocumento14 pagineIELTS Band 9 Grammar SecretsAshraf Bourei100% (1)

- SlaaDocumento36 pagineSlaaGovind BharathwajNessuna valutazione finora

- 09 BIR Stand On Cooperative CTEDocumento52 pagine09 BIR Stand On Cooperative CTEClaudio Jr OlaritaNessuna valutazione finora

- Abello vs. CIRDocumento2 pagineAbello vs. CIRluis capulongNessuna valutazione finora

- Comm. of Internal Revenue v. CA, G. R. No. 47421, May 14, 1990Documento3 pagineComm. of Internal Revenue v. CA, G. R. No. 47421, May 14, 1990Gracëëy UyNessuna valutazione finora

- ACCO 30033 Quiz 1 and 2 (AY2020-2021 1ST ACCO 30033 BSA 3-1)Documento14 pagineACCO 30033 Quiz 1 and 2 (AY2020-2021 1ST ACCO 30033 BSA 3-1)Kevin T. OnaroNessuna valutazione finora

- 221102a pr150 Davis Shawoo Loss and Damage 2210g PDFDocumento40 pagine221102a pr150 Davis Shawoo Loss and Damage 2210g PDFRahadian AhmadNessuna valutazione finora

- Local Tax - SyllabusDocumento8 pagineLocal Tax - Syllabusmark_aure_1Nessuna valutazione finora

- Interim Financial Reporting StandardsDocumento45 pagineInterim Financial Reporting StandardsTrisha Mae AlburoNessuna valutazione finora

- Tax Revenue Performance in KenyaDocumento47 pagineTax Revenue Performance in KenyaMwangi MburuNessuna valutazione finora

- Case Analysis GuideDocumento9 pagineCase Analysis Guideindiran06Nessuna valutazione finora

- PGDTDocumento68 paginePGDTFahmi AbdullaNessuna valutazione finora

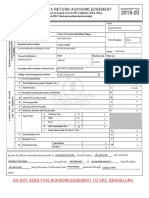

- Indian Income Tax Return Acknowledgement for AY 2019-20Documento1 paginaIndian Income Tax Return Acknowledgement for AY 2019-20Sourav KumarNessuna valutazione finora

- Geography SBA CAPEDocumento17 pagineGeography SBA CAPEChelsea Kielash Persad83% (6)

- Tax Invoice for Fitness EquipmentDocumento1 paginaTax Invoice for Fitness EquipmentVenkat DeepakNessuna valutazione finora

- Tax System - Essay, Elena CucciattiDocumento6 pagineTax System - Essay, Elena CucciattiElena CucciattiNessuna valutazione finora