Potrebbero piacerti anche

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Executive Summary: Krispy Kreme Doughnuts, and A Napping Area. Habbo Hub Shall Fill An Affordability Niche NotDocumento50 pagineExecutive Summary: Krispy Kreme Doughnuts, and A Napping Area. Habbo Hub Shall Fill An Affordability Niche NotAndreiNessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Bibliography Research Questions/ Objectives Themes/ Variables Methods Used Major FindingsDocumento8 pagineBibliography Research Questions/ Objectives Themes/ Variables Methods Used Major FindingsAndreiNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Sign HereDocumento4 pagineSign HereAndreiNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- 5 Labor Code of The Philippines PDDocumento49 pagine5 Labor Code of The Philippines PDAndrei100% (1)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- RRLDocumento86 pagineRRLAndreiNessuna valutazione finora

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Aasc 2019-ProgramDocumento2 pagineAasc 2019-ProgramAndreiNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- How I Built A Profitable Dropshipping Business in 14 Days Without Spending Money On Ads PDFDocumento33 pagineHow I Built A Profitable Dropshipping Business in 14 Days Without Spending Money On Ads PDFforoshacker100% (2)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Entreprenur Ship 115Documento115 pagineEntreprenur Ship 115alvin kunddukulamNessuna valutazione finora

- Conceptualizing Entrepreneurship in Human Resource ManagementDocumento9 pagineConceptualizing Entrepreneurship in Human Resource Managementericchico362Nessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Lesson 3 Core CompetencyDocumento31 pagineLesson 3 Core CompetencyJessie J.Nessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- A Technopreneur by The Name of Thomas Alva EdisonDocumento2 pagineA Technopreneur by The Name of Thomas Alva Edisonitzmanolr8Nessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

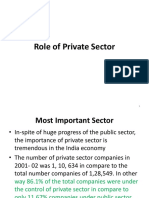

- Unit 1.1.3 Role of Private SectorDocumento26 pagineUnit 1.1.3 Role of Private SectorVinod NathanNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Chapter 1-Introduction To The World of RetailingDocumento29 pagineChapter 1-Introduction To The World of RetailingAshaAnwar83% (6)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- Chapter 6.Pptx NiosDocumento20 pagineChapter 6.Pptx Niosamita venkateshNessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Business Management NotesDocumento11 pagineBusiness Management Notesrizam aliNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Plastic Products Manufacturing Profitable Plastic Industries - 173837 PDFDocumento44 paginePlastic Products Manufacturing Profitable Plastic Industries - 173837 PDFHarshith Gowda100% (2)

- University Matriculation LectureDocumento46 pagineUniversity Matriculation LectureAkinola Oluwatoyin CharlesNessuna valutazione finora

- CSR Activities of EY:: EducationDocumento3 pagineCSR Activities of EY:: EducationSupragya SaurabhNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Why Startups Fail and How Yours Can SucceedDocumento184 pagineWhy Startups Fail and How Yours Can SucceedWerner GarciaNessuna valutazione finora

- MODULE 4 EntrepreneurshipDocumento15 pagineMODULE 4 EntrepreneurshipFunny JuanNessuna valutazione finora

- Enterprise Drivers BESDocumento4 pagineEnterprise Drivers BESPaplopaNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Cunningham 2018Documento38 pagineCunningham 2018david herrera sotoNessuna valutazione finora

- Angaros Advisory v1Documento12 pagineAngaros Advisory v1Madhu AvalurNessuna valutazione finora

- DLL G6 Q4 Week 1 All SubjectsDocumento37 pagineDLL G6 Q4 Week 1 All SubjectsNota BelzNessuna valutazione finora

- Sample SopDocumento4 pagineSample SopsomuyaNessuna valutazione finora

- Process Manual: Saksham Jharkhand Kaushal Vikas Yojana (SJKVY) Pilot PhaseDocumento50 pagineProcess Manual: Saksham Jharkhand Kaushal Vikas Yojana (SJKVY) Pilot PhaseArvind TiwariNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Entrep 4 (Real)Documento4 pagineEntrep 4 (Real)Ma.Dulce ManalastasNessuna valutazione finora

- Output: Defining and Developing The Music Sector in Northern IrelandDocumento92 pagineOutput: Defining and Developing The Music Sector in Northern IrelandGenerator NINessuna valutazione finora

- Co Working SpacesDocumento6 pagineCo Working SpacesArshad UllahNessuna valutazione finora

- Serviced Apartment: Profile No.: 41 NIC Code:55901Documento9 pagineServiced Apartment: Profile No.: 41 NIC Code:55901Shikhar Singhal100% (3)

- Full Download Small Business Management Launching and Growing Entrepreneurial Ventures 17th Edition Longenecker Test BankDocumento36 pagineFull Download Small Business Management Launching and Growing Entrepreneurial Ventures 17th Edition Longenecker Test Bankgrobesonnie100% (29)

- Ilovepdf MergedDocumento48 pagineIlovepdf MergedYogesh BantanurNessuna valutazione finora

- Immersion ReviewerDocumento29 pagineImmersion ReviewerMikyla RamilNessuna valutazione finora

- Socio demographicFactorsandEntrepreneurialInclinationAmongAdolescentsBasisfortheDevelopmentofanEnhancedEntrepreneurialProgramEEPforTeenagersDocumento25 pagineSocio demographicFactorsandEntrepreneurialInclinationAmongAdolescentsBasisfortheDevelopmentofanEnhancedEntrepreneurialProgramEEPforTeenagersMariene Thea DimaunahanNessuna valutazione finora

- Combinepdf 5Documento81 pagineCombinepdf 5Trixie Mae PerezNessuna valutazione finora

- MyZus Case Study From IIT BOMBAY IncubatorDocumento17 pagineMyZus Case Study From IIT BOMBAY IncubatorSandeep SrivastavaNessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)