Potrebbero piacerti anche

- Public International Law Bernas Chapters 1 17Documento35 paginePublic International Law Bernas Chapters 1 17D.F. de LiraNessuna valutazione finora

- LABOR RELATIONS OVERVIEWDocumento53 pagineLABOR RELATIONS OVERVIEWsusanamagtutoNessuna valutazione finora

- (Ash Panopio) PERSONS Digests Under Judge BonifacioDocumento63 pagine(Ash Panopio) PERSONS Digests Under Judge BonifacioAkiko AbadNessuna valutazione finora

- Limson v. CADocumento3 pagineLimson v. CAJMRNessuna valutazione finora

- G.R. No. 179830 December 3, 2009Documento2 pagineG.R. No. 179830 December 3, 2009Akiko AbadNessuna valutazione finora

- Bayan V ZamoraDocumento2 pagineBayan V ZamoraAkiko AbadNessuna valutazione finora

- 09 Villacorta V BernardoDocumento1 pagina09 Villacorta V BernardocrisNessuna valutazione finora

- Samaniego DigestDocumento2 pagineSamaniego DigestAnaAtenistaNessuna valutazione finora

- (Ash Panopio) PERSONS Digests Under Judge BonifacioDocumento63 pagine(Ash Panopio) PERSONS Digests Under Judge BonifacioAkiko AbadNessuna valutazione finora

- 21 Ang Tibay Vs CirDocumento1 pagina21 Ang Tibay Vs CirJose Edu G. BontoNessuna valutazione finora

- MMDA Authority to Open Private RoadDocumento3 pagineMMDA Authority to Open Private RoadAkiko AbadNessuna valutazione finora

- Criminal Procedure Atty. SalvadorDocumento119 pagineCriminal Procedure Atty. SalvadorEman Santos95% (19)

- SALES CASES Batch 2Documento4 pagineSALES CASES Batch 2Akiko AbadNessuna valutazione finora

- Election Cases Moya Vs Del FierroDocumento7 pagineElection Cases Moya Vs Del FierroAkiko AbadNessuna valutazione finora

- Train Law PDFDocumento27 pagineTrain Law PDFLanieLampasaNessuna valutazione finora

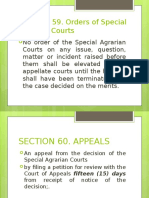

- Agra Sec 59-61Documento2 pagineAgra Sec 59-61Akiko AbadNessuna valutazione finora

- NIRC PROCEEDINGS SUMMARYDocumento10 pagineNIRC PROCEEDINGS SUMMARYAkiko AbadNessuna valutazione finora

- Criminal Procedure FlowchartDocumento6 pagineCriminal Procedure FlowchartAizaFerrerEbina91% (136)

- Additional Cases SalesDocumento3 pagineAdditional Cases SalesAkiko AbadNessuna valutazione finora

- Agra Report Sec 59-61Documento4 pagineAgra Report Sec 59-61Akiko AbadNessuna valutazione finora

- About Mgrs Competence Efficiceny 1Documento11 pagineAbout Mgrs Competence Efficiceny 1Akiko AbadNessuna valutazione finora

- Portugal v. AustraliaDocumento2 paginePortugal v. AustraliaAkiko AbadNessuna valutazione finora

- SALES CASES Batch 2Documento4 pagineSALES CASES Batch 2Akiko AbadNessuna valutazione finora

- Sales Cases Batch 1Documento3 pagineSales Cases Batch 1Akiko AbadNessuna valutazione finora

- Statcon Agpalo Summary PDFDocumento55 pagineStatcon Agpalo Summary PDFGemrose SantosNessuna valutazione finora

- HUMAN RIGHTS LAW CHAPTERSDocumento5 pagineHUMAN RIGHTS LAW CHAPTERSMegan Mateo80% (10)

- Pic Presentation PDFDocumento41 paginePic Presentation PDFAkiko AbadNessuna valutazione finora

- YUGOSLAVIA VS US ICJDocumento2 pagineYUGOSLAVIA VS US ICJAkiko AbadNessuna valutazione finora

- Portugal v. AustraliaDocumento2 paginePortugal v. AustraliaAkiko AbadNessuna valutazione finora

- Train Law PDFDocumento27 pagineTrain Law PDFLanieLampasaNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (120)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Tax Invoice: Tanmay Traders (TTR)Documento2 pagineTax Invoice: Tanmay Traders (TTR)Ajay KumarNessuna valutazione finora

- Criminal Law - Project WorkDocumento4 pagineCriminal Law - Project WorkAlapati Bhavana ChowdaryNessuna valutazione finora

- United States v. Vernon O. Holland and James Davis Drane Mauldin, JR., 956 F.2d 990, 10th Cir. (1992)Documento6 pagineUnited States v. Vernon O. Holland and James Davis Drane Mauldin, JR., 956 F.2d 990, 10th Cir. (1992)Scribd Government DocsNessuna valutazione finora

- CCD Subscription Agreement - QapitaDocumento12 pagineCCD Subscription Agreement - Qapitalegal shuruNessuna valutazione finora

- Class SuspensionDocumento1 paginaClass SuspensionMarife MagsinoNessuna valutazione finora

- The Remission of Sins by DR Edward BedoreDocumento10 pagineThe Remission of Sins by DR Edward BedoreMark Emmanuel EvascoNessuna valutazione finora

- Eraker v. Redfin and MadronaDocumento16 pagineEraker v. Redfin and MadronaGeekWire100% (1)

- De Minimis and Fringe BenefitsDocumento14 pagineDe Minimis and Fringe BenefitsCza PeñaNessuna valutazione finora

- UtilitarianismDocumento5 pagineUtilitarianismChris Cgc PettingaNessuna valutazione finora

- American Vs Director of PatentsDocumento1 paginaAmerican Vs Director of PatentsKidrelyne vic BonsatoNessuna valutazione finora

- Angara vs. ComelecDocumento3 pagineAngara vs. ComelecJonathan LarozaNessuna valutazione finora

- Cordillera Autonomy CaseDocumento10 pagineCordillera Autonomy CaseArthur YamatNessuna valutazione finora

- IMELDA CS Form No. 212 Revised Personal Data Sheet 3Documento5 pagineIMELDA CS Form No. 212 Revised Personal Data Sheet 3Heinna Alyssa GarciaNessuna valutazione finora

- 3-5 October, 2020 Icep Css - Pms DawnDocumento55 pagine3-5 October, 2020 Icep Css - Pms DawnAijaz Ali ChandioNessuna valutazione finora

- Project Costing & BillingDocumento11 pagineProject Costing & BillingHari Prasad AngalakuditiNessuna valutazione finora

- WCE Application FormDocumento1 paginaWCE Application FormMarianneNessuna valutazione finora

- 01.yau Chu Vs CA G.R. No. L-78519Documento2 pagine01.yau Chu Vs CA G.R. No. L-78519Anasor GoNessuna valutazione finora

- A&c Minimart v. VillarealDocumento2 pagineA&c Minimart v. VillarealSarah Jane UntongNessuna valutazione finora

- Electromagnetic Compatibility: Unit-2: CablingDocumento27 pagineElectromagnetic Compatibility: Unit-2: CablingShiva Prasad MNessuna valutazione finora

- Indeterminate Sentence LawDocumento4 pagineIndeterminate Sentence LawVee DammeNessuna valutazione finora

- L5 - Nature of Clinical Lab - PMLS1Documento98 pagineL5 - Nature of Clinical Lab - PMLS1John Daniel AriasNessuna valutazione finora

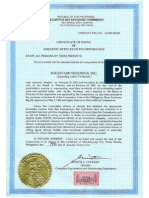

- BHI SEC Cert & Amended Articles of Incorporation PDFDocumento9 pagineBHI SEC Cert & Amended Articles of Incorporation PDFkimberly_uymatiaoNessuna valutazione finora

- Love Theme: Fromnuovocinema ParadisoDocumento3 pagineLove Theme: Fromnuovocinema Paradisogiupy93Nessuna valutazione finora

- Parallel Lines and Transversals PDFDocumento2 pagineParallel Lines and Transversals PDFRonnieMaeMaullionNessuna valutazione finora

- Cunningham Priors On April Motion To EnhanceDocumento1 paginaCunningham Priors On April Motion To EnhanceJohn S KeppyNessuna valutazione finora

- Merits and De-merits of Duty of Care and Boni Mores in Nervous Shock ClaimsDocumento4 pagineMerits and De-merits of Duty of Care and Boni Mores in Nervous Shock ClaimsPragash MaheswaranNessuna valutazione finora

- Article 1341-1355 ObliconDocumento2 pagineArticle 1341-1355 Obliconporeoticsarmy0% (1)

- District Court: Pengadilan (Negeri/agama)Documento2 pagineDistrict Court: Pengadilan (Negeri/agama)Syam Sud DinNessuna valutazione finora

- Introduction to Credit FundamentalsDocumento4 pagineIntroduction to Credit FundamentalsLemon OwNessuna valutazione finora

- Additional FINAL ReviewDocumento41 pagineAdditional FINAL ReviewMandeep SinghNessuna valutazione finora