Potrebbero piacerti anche

- Solutions To Problems: Pe On Estate TaxDocumento11 pagineSolutions To Problems: Pe On Estate TaxErica NicolasuraNessuna valutazione finora

- Tax Return in CanadaDocumento75 pagineTax Return in CanadaAlejandro VelizNessuna valutazione finora

- Compilation of MCQDocumento34 pagineCompilation of MCQDaphnie Bolo100% (1)

- Estate Tax ProblemDocumento2 pagineEstate Tax ProblemClaricel JoyNessuna valutazione finora

- Final and Capital Gains TaxDocumento7 pagineFinal and Capital Gains TaxElla Marie LopezNessuna valutazione finora

- Pe On Estate TaxDocumento25 paginePe On Estate TaxErica NicolasuraNessuna valutazione finora

- Problem 23-1, Page 650 Erica Company: Required: # Debit CreditDocumento14 pagineProblem 23-1, Page 650 Erica Company: Required: # Debit CreditDeanne LumakangNessuna valutazione finora

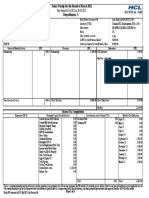

- HCL PayslipDocumento1 paginaHCL PayslipkrishnaNessuna valutazione finora

- Answer Key TaxDocumento12 pagineAnswer Key TaxLocklaim Cardinoza100% (1)

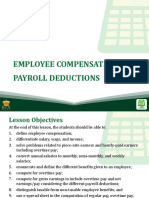

- Employee Compensation + Payroll DeductionsDocumento14 pagineEmployee Compensation + Payroll Deductionsrommel legaspi25% (4)

- Persons - Republic V de GraciaDocumento1 paginaPersons - Republic V de GraciascfsdNessuna valutazione finora

- Chapter 3 Income Taxation Tabag 2019 Sol ManDocumento21 pagineChapter 3 Income Taxation Tabag 2019 Sol ManFMM50% (2)

- 1181 - 1190 Pure and Conditional ObligationsDocumento11 pagine1181 - 1190 Pure and Conditional ObligationsscfsdNessuna valutazione finora

- 8.2 Assignment - Regular Income Tax For IndividualsDocumento8 pagine8.2 Assignment - Regular Income Tax For Individualssam imperialNessuna valutazione finora

- Sample/practice Exam 29 March 2019, Answers Sample/practice Exam 29 March 2019, AnswersDocumento8 pagineSample/practice Exam 29 March 2019, Answers Sample/practice Exam 29 March 2019, AnswersRachel Green0% (1)

- Donors Tax Problem 1 With SolutionDocumento4 pagineDonors Tax Problem 1 With SolutionAngel DaohogNessuna valutazione finora

- (PDF) Re Letter of Tony Q Valenciano (Digest) - CompressDocumento3 pagine(PDF) Re Letter of Tony Q Valenciano (Digest) - CompressscfsdNessuna valutazione finora

- Illustration Deduction and Taxable EstateDocumento8 pagineIllustration Deduction and Taxable EstateLadybellereyann A TeguihanonNessuna valutazione finora

- Router Invoice PDFDocumento1 paginaRouter Invoice PDFNikhil HatiskarNessuna valutazione finora

- CIR V CA, CTA, YMCADocumento2 pagineCIR V CA, CTA, YMCAChil Belgira100% (3)

- Corporation PDFDocumento28 pagineCorporation PDFJorufel PapasinNessuna valutazione finora

- Xviiib2 - Mapa V SandiganbayanDocumento2 pagineXviiib2 - Mapa V SandiganbayanscfsdNessuna valutazione finora

- Xviiib2 - Mapa V SandiganbayanDocumento2 pagineXviiib2 - Mapa V SandiganbayanscfsdNessuna valutazione finora

- Taxation Cup SeriesDocumento5 pagineTaxation Cup SeriesGlaiza Atillo Batuto Orgino100% (1)

- MadlangbayanDocumento2 pagineMadlangbayanscfsdNessuna valutazione finora

- Basic Principles of TaxationDocumento33 pagineBasic Principles of TaxationHenicel Diones San Juan100% (1)

- CRIM - People vs. Morilla GR. No. 189833Documento2 pagineCRIM - People vs. Morilla GR. No. 189833scfsd100% (1)

- Accounting For Corporation Reviewer 1 PDFDocumento27 pagineAccounting For Corporation Reviewer 1 PDFKrisha SaltaNessuna valutazione finora

- Property Exclusive Total DeductionsDocumento6 pagineProperty Exclusive Total DeductionsRiann DevereuxNessuna valutazione finora

- Activity 6Documento4 pagineActivity 6Mystic LoverNessuna valutazione finora

- ActivityDocumento4 pagineActivityDom PaciaNessuna valutazione finora

- Answer To Assignment No. 2Documento1 paginaAnswer To Assignment No. 2Sophia Angelica Marie MarasiganNessuna valutazione finora

- Answer: 2,000,000 Solution:: Sample ProblemDocumento17 pagineAnswer: 2,000,000 Solution:: Sample ProblemJohayra AbbasNessuna valutazione finora

- Answers To Assignment 1 and Problem Exercises Taxation2Documento4 pagineAnswers To Assignment 1 and Problem Exercises Taxation2Dexanne BulanNessuna valutazione finora

- EXERCISE 4-2. PROBLEMS (De Vera, Jazreel S. BS Accountancy V-B)Documento2 pagineEXERCISE 4-2. PROBLEMS (De Vera, Jazreel S. BS Accountancy V-B)Jazreel de VeraNessuna valutazione finora

- NUDJPIA FAR AND AFAR SOLUTIONS - Partnership LiquidationDocumento3 pagineNUDJPIA FAR AND AFAR SOLUTIONS - Partnership LiquidationKyla Artuz Dela CruzNessuna valutazione finora

- Assets 2 PDFDocumento4 pagineAssets 2 PDFMarigold CalendulaNessuna valutazione finora

- Valencia Chap 5 Estate TaxDocumento11 pagineValencia Chap 5 Estate TaxCha DumpyNessuna valutazione finora

- 04 - Task - Performance - 1 (10) BUSTAXDocumento5 pagine04 - Task - Performance - 1 (10) BUSTAXAries Christian S PadillaNessuna valutazione finora

- Bryan Moises PDFDocumento5 pagineBryan Moises PDFMary DenizeNessuna valutazione finora

- Minimum Paidup CapitalDocumento4 pagineMinimum Paidup CapitalBenj OrtizNessuna valutazione finora

- 07 Review 1Documento1 pagina07 Review 1Maricar EgnpNessuna valutazione finora

- Coop Trade Fair Overall Budget3Documento2 pagineCoop Trade Fair Overall Budget3chrisliquiganNessuna valutazione finora

- EncodedDocumento8 pagineEncodedMary Benedict AbraganNessuna valutazione finora

- De Vera Angela Kyle G. Business Taxation Prelim Task 2.1 BSADocumento11 pagineDe Vera Angela Kyle G. Business Taxation Prelim Task 2.1 BSAJohn Francis RosasNessuna valutazione finora

- Question No. 2: Module 6: Discussion 1Documento4 pagineQuestion No. 2: Module 6: Discussion 1Camille BonaguaNessuna valutazione finora

- This Study Resource Was: Problem 1Documento7 pagineThis Study Resource Was: Problem 1?????Nessuna valutazione finora

- Composition of The Gross Estate of A DecedentDocumento16 pagineComposition of The Gross Estate of A DecedentBill BreisNessuna valutazione finora

- Donor's TaxDocumento1 paginaDonor's TaxJan ernie MorillaNessuna valutazione finora

- Midterm Exam IntaxDocumento20 pagineMidterm Exam IntaxJane TuazonNessuna valutazione finora

- Assignment#1Documento9 pagineAssignment#1hae1234Nessuna valutazione finora

- Chapter 20Documento12 pagineChapter 20FireBNessuna valutazione finora

- Solution - Hand Out - Problems 16 and 17Documento14 pagineSolution - Hand Out - Problems 16 and 17Anne Clarisse ConsuntoNessuna valutazione finora

- 2dd3c613 1670283438180Documento8 pagine2dd3c613 1670283438180Kyla Gacula NatividadNessuna valutazione finora

- IRA No. 2 Answer KeyDocumento2 pagineIRA No. 2 Answer KeyProlen AcantoNessuna valutazione finora

- Chapter2aa1sol 2012 PDFDocumento18 pagineChapter2aa1sol 2012 PDFMatt David Kenneth ReyesNessuna valutazione finora

- Explore ACTIVITY 1. Fill Me In: Current AssetsDocumento4 pagineExplore ACTIVITY 1. Fill Me In: Current AssetsCOD CODNessuna valutazione finora

- Installment SalesDocumento6 pagineInstallment SalesJeramae M. artNessuna valutazione finora

- Tandem Activity GE Allowable DeductionsDocumento6 pagineTandem Activity GE Allowable DeductionsErin CruzNessuna valutazione finora

- Gross Estate Activity PDFDocumento5 pagineGross Estate Activity PDFJaypee Verzo SaltaNessuna valutazione finora

- Aec10 - Business Taxation Solution Tabag CH4Documento8 pagineAec10 - Business Taxation Solution Tabag CH4EdeksupligNessuna valutazione finora

- ACCO20093Documento7 pagineACCO20093jfcNessuna valutazione finora

- Taxation Suggested SolutionsDocumento3 pagineTaxation Suggested SolutionsSteven Mark MananguNessuna valutazione finora

- 11170189-Tugas AKL 2 11170189 - Eki AmosDocumento17 pagine11170189-Tugas AKL 2 11170189 - Eki AmosAmouse ManaluNessuna valutazione finora

- Accounting Midterm AssignmentDocumento1 paginaAccounting Midterm AssignmentTRIXIEJOY INIONNessuna valutazione finora

- Illustrations PDFDocumento3 pagineIllustrations PDFCharrey Leigh FormaranNessuna valutazione finora

- Exercise - Vanishing DeductionsDocumento1 paginaExercise - Vanishing DeductionsAndree PereaNessuna valutazione finora

- NUDJPIA FAR AND AFAR SOLUTIONS - Partnership FormationDocumento3 pagineNUDJPIA FAR AND AFAR SOLUTIONS - Partnership FormationKyla Artuz Dela CruzNessuna valutazione finora

- Chapter 5Documento6 pagineChapter 5Briggs Navarro BaguioNessuna valutazione finora

- M6 - Estate Tax Payable Students'Documento17 pagineM6 - Estate Tax Payable Students'micaella pasionNessuna valutazione finora

- CHP 3 Assignment 1 (Sarte)Documento14 pagineCHP 3 Assignment 1 (Sarte)2080288Nessuna valutazione finora

- Rental Housing: Lessons from International Experience and Policies for Emerging MarketsDa EverandRental Housing: Lessons from International Experience and Policies for Emerging MarketsValutazione: 5 su 5 stelle5/5 (1)

- ConstitutionalLaw1 CaseSummaries IBP Ocampo VinuyaDocumento20 pagineConstitutionalLaw1 CaseSummaries IBP Ocampo VinuyascfsdNessuna valutazione finora

- G.R. No. L-37251 August 31, 1981 CITY OF MANILA and CITY TREASURER, Petitioners-Appellants, Manila and ESSO PHILIPPINES, INC.,Respondents-Appellees. Aquino, J.Documento4 pagineG.R. No. L-37251 August 31, 1981 CITY OF MANILA and CITY TREASURER, Petitioners-Appellants, Manila and ESSO PHILIPPINES, INC.,Respondents-Appellees. Aquino, J.scfsdNessuna valutazione finora

- Palomera, Joshua Carl L. United Haulers Association, Inc., Et Al. vs. Oneida-Herkimer Solid Waste Management Authority, Et Al., 550 U.S. 330Documento3 paginePalomera, Joshua Carl L. United Haulers Association, Inc., Et Al. vs. Oneida-Herkimer Solid Waste Management Authority, Et Al., 550 U.S. 330scfsdNessuna valutazione finora

- Owner StatementDocumento8 pagineOwner StatementJack LeeNessuna valutazione finora

- Bill 05 04 2021Documento2 pagineBill 05 04 2021Marcelo RivellinoNessuna valutazione finora

- Cliffton Valley Price ListDocumento2 pagineCliffton Valley Price Listsishir mandalNessuna valutazione finora

- Dr-Acc. Depreciation RM 25 Mill CR - Building RM25 MillDocumento7 pagineDr-Acc. Depreciation RM 25 Mill CR - Building RM25 MillsyuhadahNessuna valutazione finora

- Taxation Question BankDocumento3 pagineTaxation Question BankRishikesh BhujbalNessuna valutazione finora

- Tax1a Preliminary ExamDocumento7 pagineTax1a Preliminary ExamCharmaine PamintuanNessuna valutazione finora

- GST Management System: A Project Report ONDocumento5 pagineGST Management System: A Project Report ONRohit GadekarNessuna valutazione finora

- Net of Withholding Kailangan Niyo I Gross Up, KayaDocumento7 pagineNet of Withholding Kailangan Niyo I Gross Up, KayaJPNessuna valutazione finora

- Reply For 16Documento1 paginaReply For 16Abhay NandaNessuna valutazione finora

- Sap hr1Documento4 pagineSap hr1zafer nadeemNessuna valutazione finora

- Lumbera LectureDocumento3 pagineLumbera LectureRyeNessuna valutazione finora

- Tax Lecture Gross IncomeDocumento6 pagineTax Lecture Gross IncomeAngelojason De LunaNessuna valutazione finora

- AMEND SEC 27 (C), RA No. 10026Documento4 pagineAMEND SEC 27 (C), RA No. 10026Bing MendozaNessuna valutazione finora

- Gas Taxes in FloridaDocumento9 pagineGas Taxes in FloridaGary DetmanNessuna valutazione finora

- Purchase GST Nagarajan GodownDocumento4 paginePurchase GST Nagarajan GodownsamaadhuNessuna valutazione finora

- 10357670-001 G0061847656Documento5 pagine10357670-001 G0061847656Syed Muhammad Imam100% (1)

- Electricity BillDocumento1 paginaElectricity BillPaul LivesNessuna valutazione finora

- Employee DataDocumento1 paginaEmployee DataDinesh RNessuna valutazione finora

- Crossword MoneyDocumento3 pagineCrossword MoneyÁgnes JassóNessuna valutazione finora

- Ajio FN0334206010 1655992237774Documento1 paginaAjio FN0334206010 1655992237774Deepak RaguNessuna valutazione finora

- Basic Requirements For New Applicants and For Bmbes Applying For Renewal of RegistrationDocumento1 paginaBasic Requirements For New Applicants and For Bmbes Applying For Renewal of RegistrationReyLouiseNessuna valutazione finora

- Asian Paints DCF ValuationDocumento64 pagineAsian Paints DCF Valuationsanket patilNessuna valutazione finora