Potrebbero piacerti anche

- Acctg 100C 01Documento6 pagineAcctg 100C 01Jose Magallanes100% (1)

- CashDocumento16 pagineCashJemson YandugNessuna valutazione finora

- 2 3 2017 ReceivablesDocumento4 pagine2 3 2017 ReceivablesMr. CopernicusNessuna valutazione finora

- Cash and Cash Equivalents Audit of Papskie CompanyDocumento3 pagineCash and Cash Equivalents Audit of Papskie CompanyNicole ReyesNessuna valutazione finora

- Financial Accounting - ReceivablesDocumento7 pagineFinancial Accounting - ReceivablesKim Cristian MaañoNessuna valutazione finora

- FarDocumento19 pagineFarsarahbeeNessuna valutazione finora

- Bank Deposits and Cash EquivalentsDocumento6 pagineBank Deposits and Cash EquivalentsPamela Mae PlatonNessuna valutazione finora

- InvestorsDocumento8 pagineInvestorsJohahn MacabuhayNessuna valutazione finora

- Analyzing notes receivable, allowance for doubtful accounts, and depreciation expenseDocumento2 pagineAnalyzing notes receivable, allowance for doubtful accounts, and depreciation expenseKean Christopher GandalalNessuna valutazione finora

- P1 Day3 RMDocumento6 pagineP1 Day3 RMabcdefg0% (2)

- Reviewer Controlling Cash Part 1Documento6 pagineReviewer Controlling Cash Part 1Mikey Irwin0% (2)

- Cash AssignmentDocumento2 pagineCash AssignmentRocelyn OrdoñezNessuna valutazione finora

- Chapter 1 Acctg 5Documento11 pagineChapter 1 Acctg 5Angelica MayNessuna valutazione finora

- Receivable Financing Qualifying Exam Review Sample QuestionsDocumento4 pagineReceivable Financing Qualifying Exam Review Sample QuestionsHannah Jane Umbay0% (1)

- Bank Reconciliation Problems SolvedDocumento4 pagineBank Reconciliation Problems Solvedsharielles /Nessuna valutazione finora

- MSU-CBA Accountancy Department bank reconciliation and proof of cash problemsDocumento3 pagineMSU-CBA Accountancy Department bank reconciliation and proof of cash problemsAsterism LoneNessuna valutazione finora

- A. TheoryDocumento10 pagineA. TheoryROMULO CUBID100% (1)

- Instruction. Encircle The Letter That Corresponds To Your Answer. Do Not Use Pencils. Avoid ErasuresDocumento6 pagineInstruction. Encircle The Letter That Corresponds To Your Answer. Do Not Use Pencils. Avoid ErasuresstillwinmsNessuna valutazione finora

- Loans and Receivables Sample Problems 2Documento2 pagineLoans and Receivables Sample Problems 2Bryce Bihag60% (5)

- Cash and Equivalents Audit ProblemsDocumento162 pagineCash and Equivalents Audit ProblemsJannah Fate100% (3)

- Assets: Statement of Financial Position RelationshipsDocumento1 paginaAssets: Statement of Financial Position RelationshipsX-2fer ClausNessuna valutazione finora

- Drill - ReceivablesDocumento7 pagineDrill - ReceivablesMark Domingo MendozaNessuna valutazione finora

- Rolito DionelaDocumento40 pagineRolito DionelaRolito Dionela50% (2)

- Polytechnic University of The Philippines College of Accountancy Junior Philippine Institute of AccountantsDocumento15 paginePolytechnic University of The Philippines College of Accountancy Junior Philippine Institute of AccountantsYassi CurtisNessuna valutazione finora

- Phinma - University of Iloilo Bam 006: Midterm Exam: Amount UncollectibleDocumento4 paginePhinma - University of Iloilo Bam 006: Midterm Exam: Amount Uncollectiblehoneyjoy salapantanNessuna valutazione finora

- CASH AND CASH EQUIVALENTS BALANCESDocumento8 pagineCASH AND CASH EQUIVALENTS BALANCESRonel CaagbayNessuna valutazione finora

- Bank Reconciliation EditedDocumento1 paginaBank Reconciliation EditedNors PataytayNessuna valutazione finora

- Janet Wooster Owns A Retail Store That Sells New andDocumento2 pagineJanet Wooster Owns A Retail Store That Sells New andAmit PandeyNessuna valutazione finora

- XDocumento2 pagineXjaymark canayaNessuna valutazione finora

- Intermediate AccountingDocumento6 pagineIntermediate AccountingMary Angeline LopezNessuna valutazione finora

- Receivable - Q2Documento3 pagineReceivable - Q2Dymphna Ann CalumpianoNessuna valutazione finora

- ReceivablesDocumento5 pagineReceivablesEren Cruz100% (1)

- Lanimfa T.dela Cruz BSA-3A: Partnership OperationDocumento4 pagineLanimfa T.dela Cruz BSA-3A: Partnership Operationleonard dela cruzNessuna valutazione finora

- 04b Receivables (Part 2)Documento6 pagine04b Receivables (Part 2)JEFFERSON CUTE100% (1)

- Drill#1Documento5 pagineDrill#1Leslie BustanteNessuna valutazione finora

- Investment Income and GainsDocumento9 pagineInvestment Income and GainsRex AdarmeNessuna valutazione finora

- Inventory LatojaDocumento2 pagineInventory Latojalisa juganNessuna valutazione finora

- Dysas - Fin Acc - 3rdDocumento5 pagineDysas - Fin Acc - 3rdJao FloresNessuna valutazione finora

- Far 102 - Cash - Bank Reconciliation PDFDocumento3 pagineFar 102 - Cash - Bank Reconciliation PDFPatty LapuzNessuna valutazione finora

- Problem 1-1 Multiple Choice (ACP)Documento11 pagineProblem 1-1 Multiple Choice (ACP)Irahq Yarte Torrejos0% (1)

- Chapter 5 Audit of PPEDocumento29 pagineChapter 5 Audit of PPELyka Mae Palarca IrangNessuna valutazione finora

- 4 InventoriesDocumento5 pagine4 InventoriesandreamrieNessuna valutazione finora

- Chapter 23 PPEDocumento5 pagineChapter 23 PPERose AysonNessuna valutazione finora

- AT - Activity - No. 8 - Substantive Testing - Axl Rome P. FloresDocumento3 pagineAT - Activity - No. 8 - Substantive Testing - Axl Rome P. FloresDanielle VasquezNessuna valutazione finora

- Notes ReceivableDocumento4 pagineNotes ReceivableJenny MendozaNessuna valutazione finora

- PAS 36 Concept MapDocumento1 paginaPAS 36 Concept MapMicah RamaykaNessuna valutazione finora

- Cash and Cash EquivalentsDocumento33 pagineCash and Cash EquivalentsJohn kyle Abbago100% (2)

- AP - Loans & ReceivablesDocumento11 pagineAP - Loans & ReceivablesDiane PascualNessuna valutazione finora

- AssignmentDocumento6 pagineAssignmentIrishNessuna valutazione finora

- Cash and Cash Equivalents GuideDocumento33 pagineCash and Cash Equivalents GuideKaren Estrañero LuzonNessuna valutazione finora

- Cash and Cash Equivalents AssignmentDocumento15 pagineCash and Cash Equivalents AssignmentJonathan Peter Del Rosario100% (1)

- RecvbleDocumento24 pagineRecvbleJoseph Salido100% (1)

- CHAPTER 8 Intermediate Acctng 1Documento58 pagineCHAPTER 8 Intermediate Acctng 1Tessang OnongenNessuna valutazione finora

- UCP: CVP Analysis and ExercisesDocumento10 pagineUCP: CVP Analysis and ExercisesDin Rose GonzalesNessuna valutazione finora

- Score for this attempt: 40 out of 40Documento34 pagineScore for this attempt: 40 out of 40moncarla lagonNessuna valutazione finora

- Account ReceivableDocumento10 pagineAccount ReceivableHarold B. Lacaba0% (1)

- National College of Business and Arts 1st Preboard Accounting ReviewDocumento7 pagineNational College of Business and Arts 1st Preboard Accounting ReviewTherese AcostaNessuna valutazione finora

- FINANCIAL ACCOUNTING 1 CASH AND CASH EQUIVALENTSDocumento9 pagineFINANCIAL ACCOUNTING 1 CASH AND CASH EQUIVALENTSPau Santos76% (29)

- Theories - Cash & Cash Equivalents: Identify The Choice That Best Completes The Statement or Answers The QuestionDocumento15 pagineTheories - Cash & Cash Equivalents: Identify The Choice That Best Completes The Statement or Answers The QuestionRyan PatitoNessuna valutazione finora

- 03 - Cash & Cash Equivalents - TheoryDocumento2 pagine03 - Cash & Cash Equivalents - TheoryROMAR A. PIGANessuna valutazione finora

- Student Organization ConsultationDocumento11 pagineStudent Organization ConsultationKent CondinoNessuna valutazione finora

- g10 Music 3rd Page 2Documento1 paginag10 Music 3rd Page 2Kent CondinoNessuna valutazione finora

- A Software System Development Life Cycle Model For ImprovedDocumento22 pagineA Software System Development Life Cycle Model For ImprovedPutri KrismayanthiNessuna valutazione finora

- Facts of CheerleadingDocumento1 paginaFacts of CheerleadingKent CondinoNessuna valutazione finora

- Chapter 11: The General Ledger and Financial Reporting CycleDocumento29 pagineChapter 11: The General Ledger and Financial Reporting CycleKent CondinoNessuna valutazione finora

- Gross Estate ProblemsDocumento17 pagineGross Estate ProblemsLloyd Sonica100% (1)

- It Systems of Fixed Assets Processe1Documento5 pagineIt Systems of Fixed Assets Processe1Kent CondinoNessuna valutazione finora

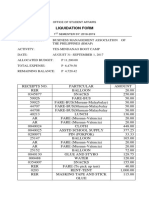

- Liquidation Form: Office of Student AffairsDocumento3 pagineLiquidation Form: Office of Student AffairsKent CondinoNessuna valutazione finora

- Gross Estate ProblemsDocumento17 pagineGross Estate ProblemsLloyd Sonica100% (1)

- Condino, K. - Income Taxation (Tax 41) SynthesisDocumento1 paginaCondino, K. - Income Taxation (Tax 41) SynthesisKent CondinoNessuna valutazione finora

- It Systems of Fixed Assets Processe1Documento5 pagineIt Systems of Fixed Assets Processe1Kent CondinoNessuna valutazione finora

- Reviewers and ScheduleDocumento1 paginaReviewers and ScheduleKent CondinoNessuna valutazione finora

- Chapter 1 and 2Documento16 pagineChapter 1 and 2Kent CondinoNessuna valutazione finora

- References CdewqDocumento1 paginaReferences CdewqKent CondinoNessuna valutazione finora

- Chapter IDocumento4 pagineChapter IKent CondinoNessuna valutazione finora

- Chapter VDocumento4 pagineChapter VKent CondinoNessuna valutazione finora

- Cash and Cash Equivalents Audit Procedures CONDINODocumento11 pagineCash and Cash Equivalents Audit Procedures CONDINOKent CondinoNessuna valutazione finora

- Ethnoveterinary Medicine in SpainDocumento11 pagineEthnoveterinary Medicine in SpainKent CondinoNessuna valutazione finora

- Appraisal of Ethno-Veterinary PracticesDocumento7 pagineAppraisal of Ethno-Veterinary PracticesKent CondinoNessuna valutazione finora

- Vetsci00118 0006Documento1 paginaVetsci00118 0006Kent CondinoNessuna valutazione finora

- Ethnobotanical Study... EthiopiaDocumento10 pagineEthnobotanical Study... EthiopiaKent CondinoNessuna valutazione finora

- Corporate Books and Records Chapter 11Documento17 pagineCorporate Books and Records Chapter 11NingClaudioNessuna valutazione finora

- South Indian BankDocumento11 pagineSouth Indian BankAngel BrokingNessuna valutazione finora

- Types of Cyber CrimeDocumento22 pagineTypes of Cyber CrimeHina Aswani100% (1)

- Shareholders Agreement ChecklistDocumento7 pagineShareholders Agreement Checklistantstar2005100% (1)

- The Capital Box, Gurgaon: A Project Report On Comparative Study of Ulips and Mutual FundsDocumento60 pagineThe Capital Box, Gurgaon: A Project Report On Comparative Study of Ulips and Mutual FundsAnup PatraNessuna valutazione finora

- Sample MoaDocumento7 pagineSample MoaKool GuyNessuna valutazione finora

- NAB CEO Press Conference Transcript PDFDocumento4 pagineNAB CEO Press Conference Transcript PDFmrfutschNessuna valutazione finora

- FRM Practice Exam Part 2 NOVDocumento139 pagineFRM Practice Exam Part 2 NOVkennethngai100% (2)

- Noes Flex CubeDocumento8 pagineNoes Flex CubeSeboeng MashilangoakoNessuna valutazione finora

- Hotel Banquet QuotationDocumento4 pagineHotel Banquet QuotationeriismailNessuna valutazione finora

- Fintech 400 PDFDocumento410 pagineFintech 400 PDFHarshil MehtaNessuna valutazione finora

- CAT T1 Recording Financial Transactions Course SlidesDocumento162 pagineCAT T1 Recording Financial Transactions Course Slideshazril46100% (5)

- Instructor'S Manual: International Payment Terms or Documentary CreditDocumento2 pagineInstructor'S Manual: International Payment Terms or Documentary CreditNorhidayah N ElyasNessuna valutazione finora

- 2010 Legal Aspects Banking Regulation Common Law Perspectives From ZambiaDocumento352 pagine2010 Legal Aspects Banking Regulation Common Law Perspectives From ZambiaHenri NamalombaNessuna valutazione finora

- RinggitPlus Jirnexu Case StudyDocumento4 pagineRinggitPlus Jirnexu Case StudyMeng Chuan NgNessuna valutazione finora

- CAPITAL-MARKET-BBA-3RD-SEM - FinalDocumento84 pagineCAPITAL-MARKET-BBA-3RD-SEM - FinalSunny MittalNessuna valutazione finora

- Credit Analysis Techniques: Classification & AssessmentDocumento27 pagineCredit Analysis Techniques: Classification & AssessmentJavaria IqbalNessuna valutazione finora

- I.TAx 302Documento4 pagineI.TAx 302tadepalli patanjaliNessuna valutazione finora

- Teacher's Handout MoneyDocumento5 pagineTeacher's Handout MoneyannNessuna valutazione finora

- Introduction To Payment Processing in SAP 120815Documento14 pagineIntroduction To Payment Processing in SAP 120815Senij Khan50% (2)

- Income Under The Head Capital Gains Section 45 (1) : (Charging Section)Documento9 pagineIncome Under The Head Capital Gains Section 45 (1) : (Charging Section)hemantNessuna valutazione finora

- 01 - Mango Financial Management Essentials (232p)Documento232 pagine01 - Mango Financial Management Essentials (232p)Book File100% (6)

- Banking and Financial InstitutionsDocumento6 pagineBanking and Financial InstitutionsCristell BiñasNessuna valutazione finora

- Financial Inclusion in India - A Review of InitiatDocumento11 pagineFinancial Inclusion in India - A Review of InitiatEshan BedagkarNessuna valutazione finora

- G & M Philippines, Inc., V Romil V. Cuambot G.R. No. 162308 November 22, 2006 FactsDocumento2 pagineG & M Philippines, Inc., V Romil V. Cuambot G.R. No. 162308 November 22, 2006 FactsggNessuna valutazione finora

- CA Inter Advanced Account - Regular Course by CA P S BeniwalDocumento346 pagineCA Inter Advanced Account - Regular Course by CA P S BeniwalHarry PotterNessuna valutazione finora

- IB - Modes of Deposit and Profit Calculation - v5Documento56 pagineIB - Modes of Deposit and Profit Calculation - v5ShakikNessuna valutazione finora

- Source Finance Wahid Sandhar SugarsDocumento47 pagineSource Finance Wahid Sandhar SugarsSeema RahulNessuna valutazione finora

- Funds - Transfer V1 PDFDocumento46 pagineFunds - Transfer V1 PDFTanaka MachanaNessuna valutazione finora

- Chapter 1 Financial AccountingDocumento10 pagineChapter 1 Financial AccountingMarcelo Iuki HirookaNessuna valutazione finora