Potrebbero piacerti anche

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- Incorporating The Financial Impact of Environmental Issues in Financing, Investing, And/or Operating DecisionsDocumento6 pagineIncorporating The Financial Impact of Environmental Issues in Financing, Investing, And/or Operating DecisionsAshlee JornadalNessuna valutazione finora

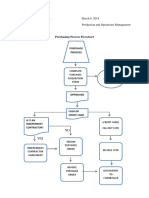

- FlowcharttDocumento4 pagineFlowcharttAshlee JornadalNessuna valutazione finora

- Plant Roots Written ReportDocumento3 paginePlant Roots Written ReportAshlee JornadalNessuna valutazione finora

- Seed Report OutlineDocumento2 pagineSeed Report OutlineAshlee JornadalNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Civ Beyond Earth HotkeysDocumento1 paginaCiv Beyond Earth HotkeysExirtisNessuna valutazione finora

- IcarosDesktop ManualDocumento151 pagineIcarosDesktop ManualAsztal TavoliNessuna valutazione finora

- Colorfastness of Zippers To Light: Standard Test Method ForDocumento2 pagineColorfastness of Zippers To Light: Standard Test Method ForShaker QaidiNessuna valutazione finora

- Ci Thai RiceDocumento4 pagineCi Thai RiceMakkah Madina riceNessuna valutazione finora

- Switching Simulation in GNS3 - GNS3Documento3 pagineSwitching Simulation in GNS3 - GNS3Jerry Fourier KemeNessuna valutazione finora

- DS Agile - Enm - C6pDocumento358 pagineDS Agile - Enm - C6pABDERRAHMANE JAFNessuna valutazione finora

- Back Propagation Neural NetworkDocumento10 pagineBack Propagation Neural NetworkAhmad Bisyrul HafiNessuna valutazione finora

- Project Management TY BSC ITDocumento57 pagineProject Management TY BSC ITdarshan130275% (12)

- Owners Manual Air Bike Unlimited Mag 402013Documento28 pagineOwners Manual Air Bike Unlimited Mag 402013David ChanNessuna valutazione finora

- Predator U7135 ManualDocumento36 paginePredator U7135 Manualr17g100% (1)

- EKC 202ABC ManualDocumento16 pagineEKC 202ABC ManualJose CencičNessuna valutazione finora

- Maritime Academy of Asia and The Pacific-Kamaya Point Department of AcademicsDocumento7 pagineMaritime Academy of Asia and The Pacific-Kamaya Point Department of Academicsaki sintaNessuna valutazione finora

- Binary OptionsDocumento24 pagineBinary Optionssamsa7Nessuna valutazione finora

- Conservation Assignment 02Documento16 pagineConservation Assignment 02RAJU VENKATANessuna valutazione finora

- Experiment - 1: Batch (Differential) Distillation: 1. ObjectiveDocumento30 pagineExperiment - 1: Batch (Differential) Distillation: 1. ObjectiveNaren ParasharNessuna valutazione finora

- Grade 9 Science Biology 1 DLPDocumento13 pagineGrade 9 Science Biology 1 DLPManongdo AllanNessuna valutazione finora

- Expression of Interest (Consultancy) (BDC)Documento4 pagineExpression of Interest (Consultancy) (BDC)Brave zizNessuna valutazione finora

- Maritta Koch-Weser, Scott Guggenheim - Social Development in The World Bank - Essays in Honor of Michael M. Cernea-Springer (2021)Documento374 pagineMaritta Koch-Weser, Scott Guggenheim - Social Development in The World Bank - Essays in Honor of Michael M. Cernea-Springer (2021)IacobNessuna valutazione finora

- Elpodereso Case AnalysisDocumento3 pagineElpodereso Case AnalysisUsama17100% (2)

- Lab Report SBK Sem 3 (Priscilla Tuyang)Documento6 pagineLab Report SBK Sem 3 (Priscilla Tuyang)Priscilla Tuyang100% (1)

- Manual For Tacho Universal Edition 2006: Legal DisclaimerDocumento9 pagineManual For Tacho Universal Edition 2006: Legal DisclaimerboirxNessuna valutazione finora

- Standard Test Methods For Rheological Properties of Non-Newtonian Materials by Rotational (Brookfield Type) ViscometerDocumento8 pagineStandard Test Methods For Rheological Properties of Non-Newtonian Materials by Rotational (Brookfield Type) ViscometerRodrigo LopezNessuna valutazione finora

- Feasibility Study For Cowboy Cricket Farms Final Report: Prepared For Prospera Business Network Bozeman, MTDocumento42 pagineFeasibility Study For Cowboy Cricket Farms Final Report: Prepared For Prospera Business Network Bozeman, MTMyself IreneNessuna valutazione finora

- List of Sovereign States and Dependent Territories by Birth RateDocumento7 pagineList of Sovereign States and Dependent Territories by Birth RateLuminita CocosNessuna valutazione finora

- Kapinga Kamwalye Conservancy ReleaseDocumento5 pagineKapinga Kamwalye Conservancy ReleaseRob ParkerNessuna valutazione finora

- Account Statement 250820 240920 PDFDocumento2 pagineAccount Statement 250820 240920 PDFUnknown100% (1)

- 5066452Documento53 pagine5066452jlcheefei9258Nessuna valutazione finora

- GE 7 ReportDocumento31 pagineGE 7 ReportMark Anthony FergusonNessuna valutazione finora

- Babe Ruth Saves BaseballDocumento49 pagineBabe Ruth Saves BaseballYijun PengNessuna valutazione finora

- Gaming Ports MikrotikDocumento6 pagineGaming Ports MikrotikRay OhmsNessuna valutazione finora